Last week’s capex report was both keenly anticipated and the source of much confusion. It was keenly anticipated, as it’s broadly understood that Australia’s investment bulge will pass (at some point). It was the source of much confusion, as there were a very broad variety of views on what the data meant — some claiming it presaged strong growth, and others claiming that it signalled a looming capex collapse.

The source of divergence really boils down to how one converts the capex intentions data into a capex forecast. The RBA recommends a regression approach, so that’s what I have used. There is, however, a small difference between our methods — I don’t have sectoral business conditions data, so I have not made that adjustment. Given that conditions are depressed just now, this is likely to bias my results up a little.

If we take the capex intentions data seriously, the Q1 capex report suggests a 10% increase in the nominal value of private sector capital investment in FY13-14. That’s not what I expected to find …

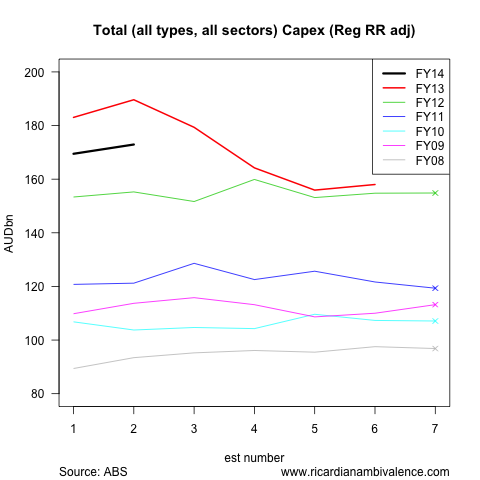

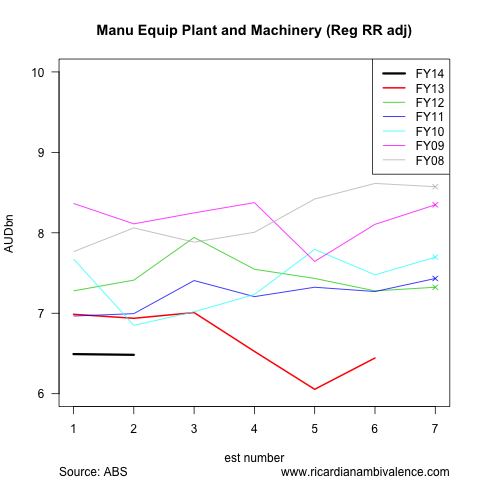

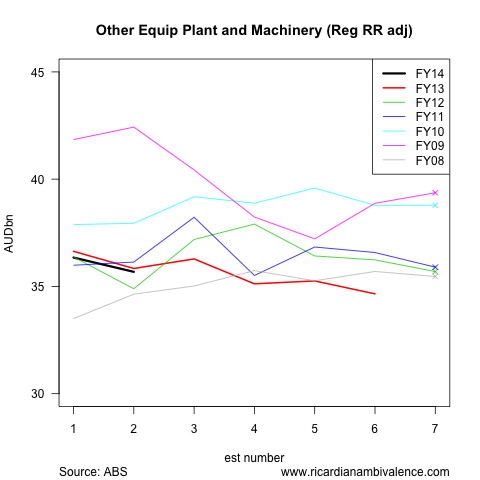

The above chart shows the evolution of the capex outlook by financial year across the seven estimates — with a cross at the endpoint, where the data represents the actual amount of money spent, rather than a forecast.

There are two reasons why the line moves from estimate to estimate: first, firms may revise projections for capital expenditure; second, even if the projections are unchanged the forecast will change as realisation ratios vary from period to period (initial estimates tend to be too small, and later estimates tend to be fairly accurate).

The ongoing growth of capex due to forecast growth in building and structures investment. Building and structures investment is typically underestimated in the early surveys — so the adjustment inflates the projection. The sixth estimate is generally fairly accurate, and the second estimate for FY14 is higher than the sixth estimate for FY13, so after adjustment we get ~15% growth.

The weakness we have all heard about is clearer in equipment, plant and machinery (EPM) investment. Again, firms tend to under-estimate EPM investment this far out, so the fact that the second estimate for FY14 is 22% below the sixth estimate for FY13 is basically undone by the adjustment process — after adjustment, we end up with a 1.3% decline in EPM investment.

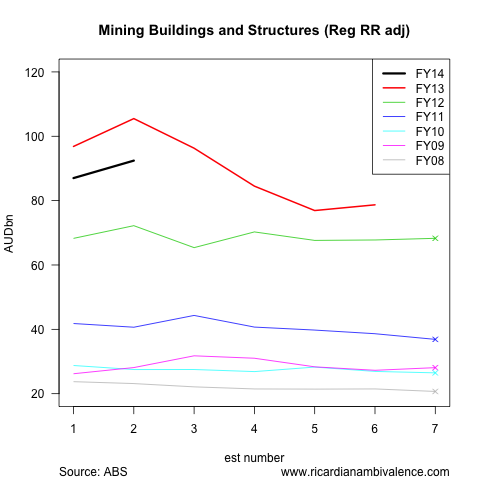

The mining sector is fully responsible for the ongoing growth of building and structures capex. After adjustment, the second estimate for FY14 suggests 17% growth.

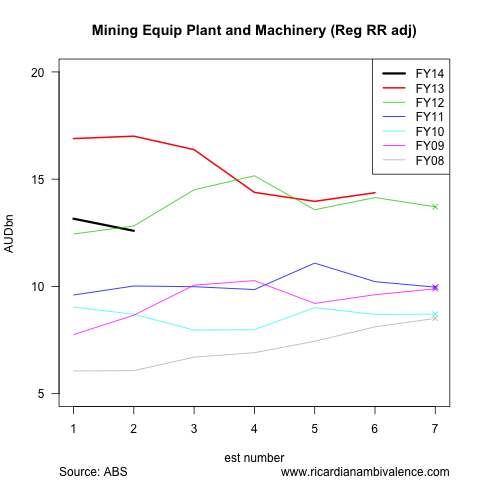

The weakness is clearer in EPM capex (fitting the narrative of business optimisation that’s coming from the management teams of BHP and Rio). After adjustment, mining EPM capex looks set to decline by ~12% in FY14.

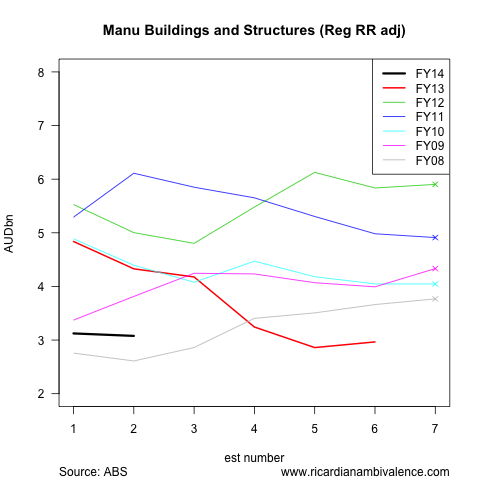

Consistent with the awful manufacturing PMIs, the manufacturing sector does not plan to invest much in FY14 (investment is down ~50% from the peak in FY12). After adjustment, the second estimate for FY14 suggests growth of building and structures investment of ~4% in FY14. This ought to pick up somewhat if the AUD goes down a little further.

After adjustment, the intentions data suggests that Manufacturing investment in EPM will basically hold steady at a low level in FY14. This is down ~30% from the peak of ~9.4bn in FY06.

Happily for the RBA (which is looking for other sources of demand to pick up as mining investment drops off), the ‘other’ sector held onto most of the promising start to FY14. After adjustment to the intentions data, growth of ‘other’ buildings and structures investment looks likely to be ~8.5% in FY14. This is ~7% down from the peak of ~24bn in FY11.

There is a similarly positive tone to the ‘other’ sector EPM investment intentions. After adjustment, growth of ~3% in FY14 looks likely. This is down ~10% from the peak of ~39bn in FY11.

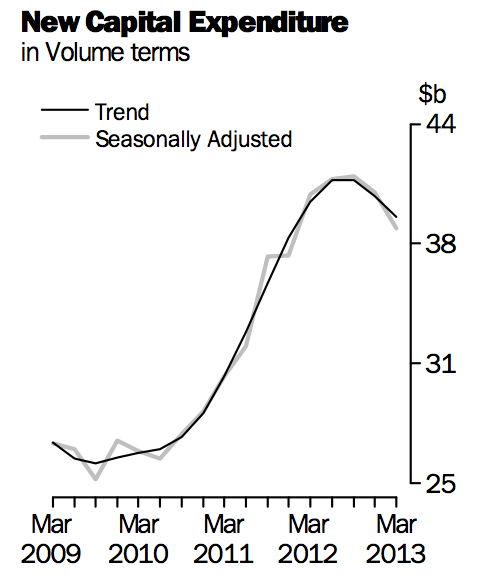

I find all this a little hard to stomach — no one can forecast this stuff, and though realisation ratio adjustment to intentions is useful, it’s not everything. My sense is that the above graph tells the story a little better: investment has peaked, and is trending down.

I find all this a little hard to stomach — no one can forecast this stuff, and though realisation ratio adjustment to intentions is useful, it’s not everything. My sense is that the above graph tells the story a little better: investment has peaked, and is trending down.

Still, this is a useful exercise as it’s a fair approximation of what the RBA is likely to do with the capex data. When they meet this week, they are unlikely to feel pressed to cut rates, as the intentions numbers says we are unlikely to have fallen over the capex cliff.

In the absence of firm data, i guess this is a reasonable conclusion. The downtrend in real activity pretty clearly sets out the risks around these capex projections: which is the reason I expect the RBA to continue cutting rates in due course.

I continue to favour cuts following the quarterly CPI releases (-25bps in August and November) — though they could some sooner if the unemployment rate starts to move up quickly.

Why comparing 2nd vs 6th instead of 2nd vs 2nd? if we assume a similar development as last year, the 2nd is too optimistic, no? If we compare 2nd vs 2nd we conclude we start next year with lower investment intentions compared to this year. I think next year realization rate will be similar to this year. The actual spending clearly shows the peak, I find it hard to believe that this will evolve into higher spending next year.

clearly there are a variety of approaches. we do not know what the 2nd RR is for 12-13, so we would have to inflate by the 11-12 RRs.

We know that the actual total 12-13 is going to be very close 160 billion (40 billion per quarter, and very close to 6th estimate of 12-13). That’s a bit down from 1st estimate 12-13 and lower than all estimates for 12-13.

I would forecast a similar outcome for 13-14 : we are at the peak, differently from all previous years when the mining boom was ongoing / starting to form. These are mostly existing / known mining projects, not new mega projects as they were in previous years.

By similar outcome for 13-14 I mean a similar RR, with total for the year being actually slightly lower: 160b for 12-13 vs 150b for 13-14. I do not know if that’s referred to as a “cliff” or a “plateau”, but I am definitely not seeing into this report a 13-14 investment that is larger than 12-13.

nor do i — that was basically the point of the post.

I guess we can use whatever RR we like, for instance the CBA conclusion after the report is that “Capex spending plans for 2013/14 are holding up. Nominal capex looks like it will grow by 10% in 2013/14”

Click to access 300513-Capex.pdf

another excellent article.

you obviously have too little to do on the week-end.

We can all be thankful for that!!

SSEC, you are big on NGDP targets.

Read Simon Wren-Lewis’s opnion now. Very interesting.

It is in my Around the Traps. Look under the Wonk heading!

Tell us what you think. Maybe we can have a deabte here about it!

everyone loves ngdp — except me!

australian trade prices are not controllable, nor is our fx, so why would we target ngdp? makes no sense to me

SSEC, you are big on NGDP targets….

no, I am not, maybe confusing me with Rajat ?

so sorry then I have mixed people up.

It happens when you are over 50!

:)