We’re now on the run into the September FOMC meeting. The key report will be this Friday’s non-farm payrolls report — as the labour market is the best leading indicator of inflation — however there’s already been a few awkward releases for the hawks.

Friday delivered yet another — the July PCE report showed ongoing too low inflation.

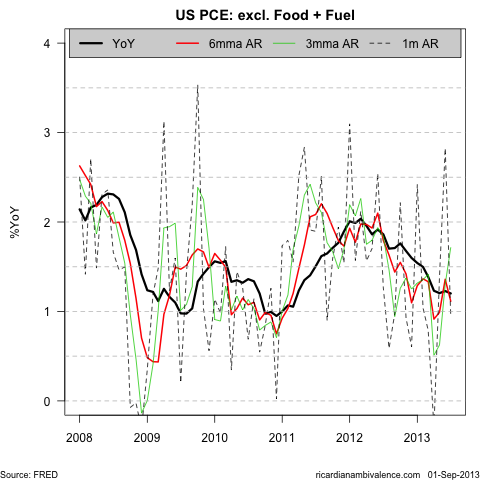

Core PCE inflation rose at an annualised pace of less than 1%y/y in July, and over the year is up only 1.2%. The 6mma AR pace is the best gauge, and this fell 25bps to 1.1%y/y.

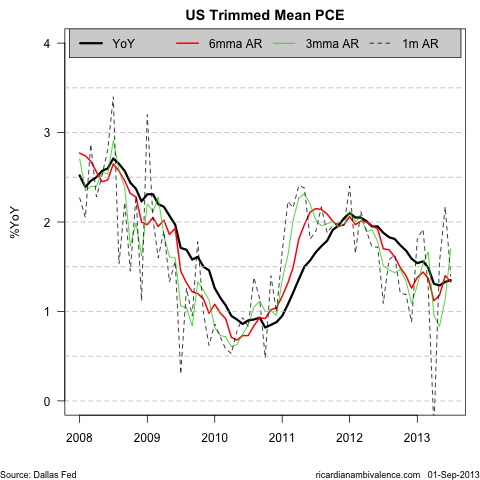

Of course, food and fuel make up an important part of the cost of living, so trimmed mean PCE inflation is probably a better measure. This was also very low, with the 1m AR pace and through the year pace both ~1.4%. The 6mma AR is ~1.3%, and though there are some signs of a pickup from the Q2 low, it’s not yet certain.

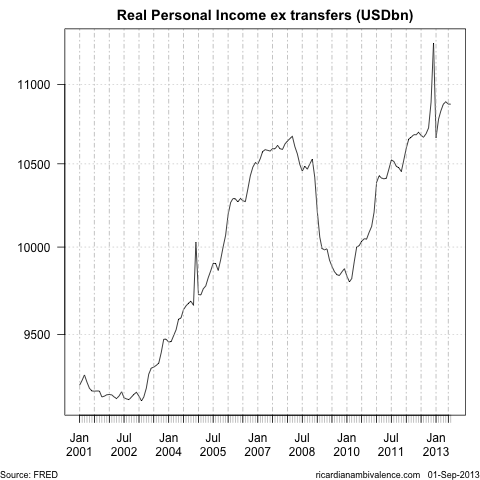

Inflation is too much money chasing too few goods, and the (real) Income excluding transfers data suggests that we are a long way away from a problem. Personal Income excluding transfers is little above the prior cycle peak, and is not rising particularly quickly.

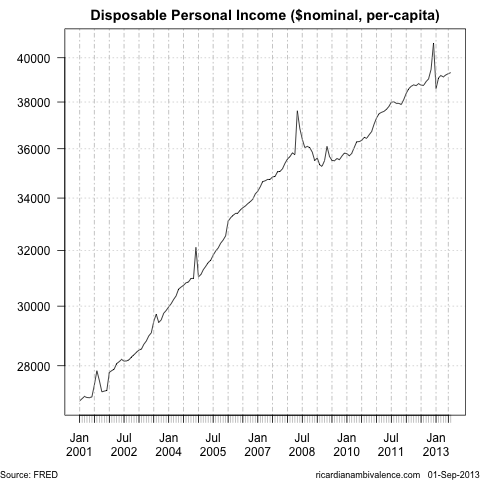

Thanks to inflation, nominal income per capita is more convincingly above the prior peak, but even here the slowdown in the pace of trend growth is very clear.

So the US situation is one of weak inflation and slow income formation — wich means inflation risks are likely to remain low. I doubt this is an environment in which monetary policy is going to be tightened very much.

about time. You were starving us!!

Yeah, sorry about that. Things ought to be more consistent now.

This confirms we’re not even at the point where we need to ask whether tapering represents a ‘tightening’ of mon pol or a ‘reduction in stimulus’ or whether they are even mutually exclusive. Clearly the US economy needs more stimulus, even if the Fed didn’t have a dual mandate. At the Sumner talk last week, an RBA employee who was working at the Fed at the time said that the Fed staff were consistently more dovish than the Board in late 2008. He also said the staff didn’t think that much of many Governors’ understanding of monetary economics.

you are forgiven!!

Rajat, it could be worse it could be the ECB!