This is the five year anniversary of the collapse of Lehman Brothers, and the steady stream of retrospectives has given me cause to think back on my own journey.

There is little doubt that my views have changed substantially over the subsequent five years — mostly with regard to the potency of policy, and therefore the appropriate place of policy markers.

I started the period with fairly dry views: I was on the dry side of the mainstream for academic economists (the academic I most admired was Tom Sargent), and well outside the (Keynesian) mainstream for a financial market economist.

For example, I doubted that either fiscal or monetary policy had important impacts on real variables over meaningful periods (say longer than five years), and was fairly sure that the impact of fiscal and monetary policy was small even over shorter periods … I no longer hold these views.

The financial crisis delivered a fairly serious stress-test of economic dogma. It threw up not only extreme cases, but also contrasting ones (the contrasting approach to fiscal policy taken by the US and UK governments, for example). Folks will be writing PhD’s on this period for a generation, but allow me some premature conclusions of my own.

Fiscal Policy: fiscal policy certainly works in the short run. It may work for bad reasons, but it does work. I now have no qualms with the assertion that the Government can temporarily increase the demand for goods and services by buying more stuff.

As wasteful as it might well have been in Australia (and in many other places), there simply wasn’t much evidence for the proposition that the private sector, anticipating higher future taxes, would pull back in equal measure. At least in the case where the private sector is already retrenching (as it was in the wake of the financial shocks that started the crisis of 2008) there is fairly compelling evidence that fiscal policy works.

Given this, there’s a reasonable case for a trade-off between wasting human capital (by allowing a demand shortfall to persist) and wasting taxpayer money via hasty spending (a.k.a. ‘fiscal stimulus’).

In the presence of large shocks, I now support increased government spending. Of course, in the long run, it’s only likely to increase welfare if the marginal product of Government spending is not only positive, but also sufficiently high — but i am now comfortable that there is trade-off to be made here, and that some wasteful spending might be okay so long as it keeps folks in work.

A part of the problem with this as a policy strategy is corruption, and another part of the problem is waste. A way to manage both is to plan ahead. I think it’s important that governments do so, by maintaining infrastructure priority lists and detailed up-to-date schema for executing (if necessary).

Monetary Policy: the old dogma is that the central bank sets the price level, and that is all. Over the years, all the arguments were about the period in which money might have a temporary impact on real variables.

Is there such a period? How long is the short run? Even if there is a short run trade-off, is it worth exploiting?

I still hold the view that the only thing a central bank can do in the long run is set the price level, but I am no longer sure that this is the only thing they ought to focus on over shorter periods. Central banks seem to be able to move both real and nominal variables over meaningful periods – and it seems likely that they are able to increase welfare by nudging the economy in beneficial directions. And yes, it even seems that they have the wisdom to use these powers at the ‘right’ time (so the trade off is worth exploiting).

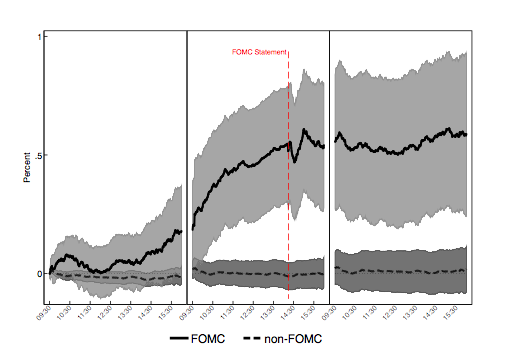

The evidence has been around for some time, particularly in equities (see the above chart which splits equity returns into the three days around the FOMC meetings, and the rest — all the returns come around Fed days) — but being a rates guy, i had not noticed.

It seems that some central banks (well, at least one of them) can have a very large impact on real variables for a meaningful period of time.

The evidence that challenged me most on this was late in the crisis – it was the sharp increase in long-term US real yields as the fed started talking about tapering their bond purchases. This is very weird if you have even a mild ‘neutrality’ view of money.

Up until that time, the main thing that had happened was that real yields fell as the FOMC eased monetary policy. That didn’t tell theorists anything much, as the FOMC and market may have been both responding to the evidence that the economy was weak.

The move away from QE3, and the consequent increase in real yields (but less so the collapse in break-even rates of inflation) challenged me, as it occurred despite fairly lack-lustre data. Thus, i do not buy the story that real yields have risen and that the Fed has got less dovish because the data has picked up.

In this case, i think the data has remained weak and that very long dated real yields have risen due to the Fed’s change of stance. Particularly at the long end, this should not occur. Central banks ought not be able to change 30yr real rates (even if you think the short run is a long time!).

Trend Micro is blocking your site as a “verified threat”.

Protecting the RBC theorists of the future!

Really good article from the perspective of when one changes their mind. I believe you are in the Keynes camp of when the facts change I change my mind. what do you do ?

Even(?) Friedman believed that monetary policy could have real effects (the Great Depression!), so you must have been really hardcore! Almost every model I studied back in the early 90s had RE, so I can see how it might have happened…

I have to disagree on fiscal policy. Not on Ricardian Equivalence grounds but on monetary offset grounds. With a central bank targeting a nominal variable – whether inflation or NGDP or the currency – monetary policy should offset discretionary fiscal policy. Hence Sumner’s maxim, which Stephen Kirchner has taken up, that “estimates of fiscal multipliers become little more than forecasts of central bank incompetence.” Would QE3 have happened if not for Q1’s fiscal tightening? Would Oz rates have fallen below 3% if there was no stimulus? I would say ‘no’ to the first and ‘yes’ to the second. The other thing about fiscal policy is the inevitable delays. As I was just explaining to a non-economist friend, only $1bn out of $14bn of BER planned spending had been spent by the end of September 2009. Yet the RBA started raising rates in early October 2009, suggesting nominal demand was already expected to grow too fast by then. So nearly all of the BER spending was counter-productive from a Keynesian demand-management perspective, ignoring the whole allocative inefficiency issue. Maybe the first round of cash handouts was worthwhile, but that’s all I would have done.

Friedman staked his career on the real impact on money – but that view has lost a fair amount of favour. I still like the principle that one should start with the model in which most of these things (debt, money) are neutral and then work to understand why they matter – but i guess i am quicker to accept that they might work now.

The uncomfortable fact is that many of these things work for ‘bad’ reasons – but perhaps the trade-offs are worth it.

the main problem is that RE has very little evidence supporting it. Afterall Adam Posen found no evidence of it in Japan so if it ain’t going to happen there then when will it happen.

The most wasteful thin to do is nothing and let unemployment rise 9 in most cases at least double).

Little actual evidence of waste here.

That was a sensational post. I really like reading people document a change of mind and why. Helps keep me sensible and less cocky as well.

There’s a great discussion between Robert Skildelsky, Epstein and Munger which touches on what economics actually knows…I like how a strong Keynesian (Skildelsky) and Libertarian (mainly Munger) interacted on this.

http://www.econtalk.org/archives/2013/09/capitalism_gove.html

At the moment for me, macro is really story telling. Too little data and too many complicated models -> over fit -> tell whatever story you would like. Micro is a different story.

Thanks mate, i will check it out. I have heard it said that macro has too many stories and not enough data – i think that’s about right.

Oh I also liked how Skildelksy kept returning to the topic of how fiscal transfers smooth over social frictions. I think that is a key feature and raison-d’etre of nation states (see Bobbit’s Shield of Achilles) and cannot be wished away, eg by Libertarians. Unfortunately for Skildelsky, the welfare state is no longer viable. States will need to change to ensure their survival. We are already see snippets of this (e.g. focus on opportunity rather than safety net). Skildelsky’s concerns about public order are also less warranted as the population ages. Cowen’s argument is that older people vote law and order even to their own detriment and they aren’t likely to be manning the barricades so to speak.