I have been of the view that the Fed would announce a tapering of their Treasury purchases at the upcoming (September 18) policy window. I still hold that view — but with much less conviction. The fact is that the labour market appears to have softened in a meaningful way over the past few months.

While it’s true that the increase in non-farm payrolls was decent (+169k v. mkt whispers of 200k), it’s also true that the size and direction of revisions (-16k to 172k for June, and -58k to 104k for July) suggest that the labour market may be a little more flaky than the headline jobs number suggests.

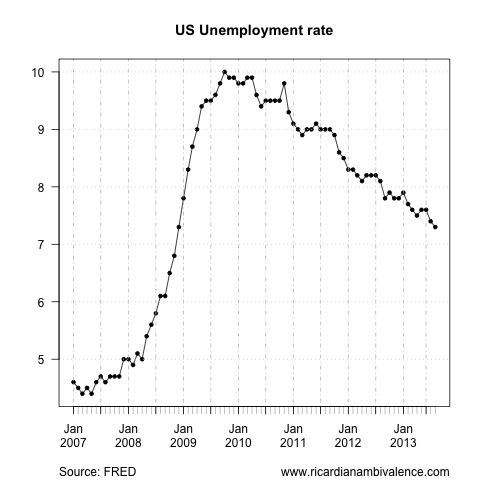

The much commented upon decrease in the unemployment rate was for bad reasons …

Folks have given up looking for work …

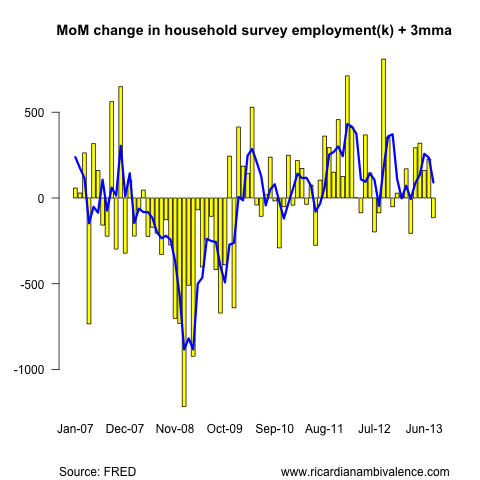

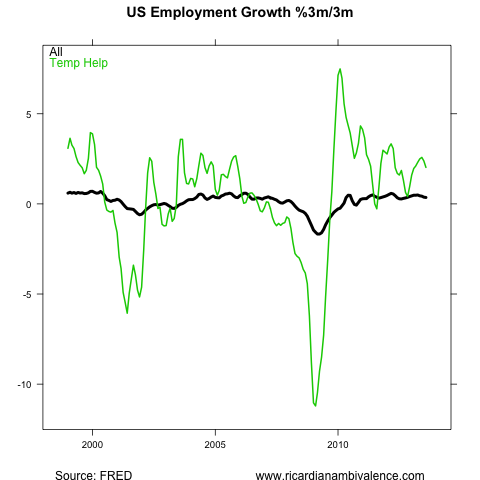

And fewer jobs. The household survey (from which the unemployment rate is drawn) actually showed a 115k drop in employment. The household survey is noisy, so that will happen from time to time, but there’s now a clear downtrend from ~200k/month to ~150k/m.

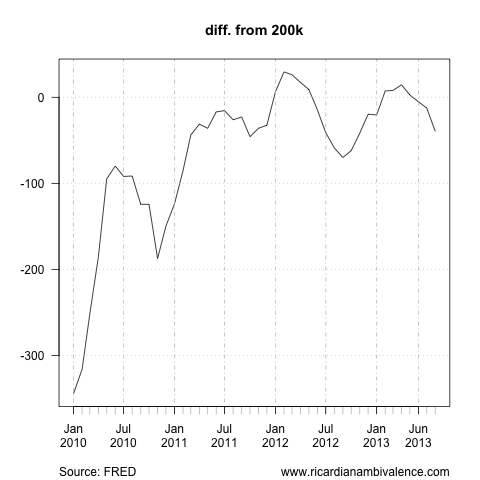

This downtrend is notable in the non-farm payrolls survey as well, with the gap to jobs growth of 200k/m (what i’d taken as a necessary condition for ending QE3) now widening.

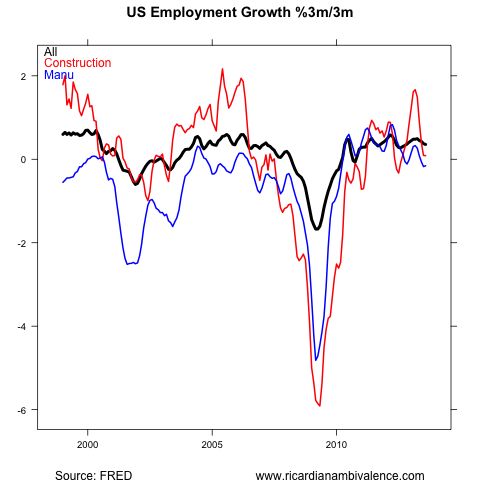

Notwithstanding the healthy increase in retail employment, the cyclical sectors are looking weak. Employment growth in construction employment has stalled, and even with a decent gain in August (+14k) the prior weakness (JUne -7k, July -16k) is weighing the sector down.

Temporary employment continues to grow, but there’s a hint of roll over there as well – which probably reflects the leading edge of the restraining impact of higher rates.

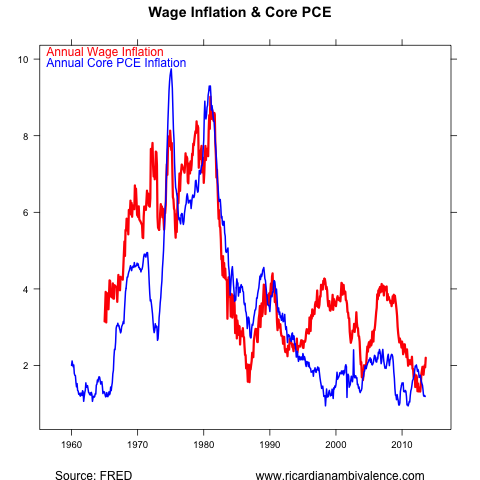

There is only one part of the report which i can see which suggests a case for tightening monetary policy — that is the increase in wages. Wages, however, are a lagging indicator of the labour market’s state — so the strength we’re seeing now is more a reflection of how things were a few quarters back.

Still, if the Fed was worried about very low PCE inflation, it would take a lot of comfort from the fact that wage inflation is finally picking up once again.

So can the Fed taper with this data? Yes, they probably can — but i would think that it’ll be small (maximum 10bn/m), and that it’ll be accompanied by changes to their forward guidance that show they don’t expect to raise the funds rate very quickly. I expect them to add something about defending their inflation target from the low side (a change that started last meeting, to get Bullard on side).

Note that this will be the first meeting where we see the FOMC’s forecasts for 2016 — including the funds rate dots. I am guessing that the median vote will have a forecast funds rate around 2% for the end of 2016, which is similar to what the Eurodollars currently imply.

I can’t see how they can. The economy doesn’t look on a sustainable run to me!

Big moment for the Bernanke legacy. Do you think the recent (US) jobs weakness is behind the recent rise in the AUD?

Partly – the pro USD trade was getting very crowded. I also think the bearish china trade was overcooked.

However both the manufacturing and service indexes – which are forward looking – were VERY strong. Maybe they could skip Sep and wait for Dec, but I do not think this changes things much, as the Fed has already decided it’s only a matter of time and I think they want to start this before the new chairman is nominated.

ISMs are not forward looking – they have little predictive value, even new orders – but they are timely. I prefer nfp to the isms, but you make a fair case – one release isn’t everything.

yes, the employment component of the ISM pretty good, let’s see if that converts to good nfp before winter.

This is why low rates are very dangerous if not regulated properly. Data released late last month by APRA (for Australia):

* 38.7% of new home loans issued by banks over the June quarter were interest-only; (!!!!! = Investors)

* 13.5% of new home loans had a loan-to-value ratio (LVR) of greater than or equal to 90%;

* 19.2% of new home loans had a LVR of between 80% and 90%;

(meaning that 32.7% of total new home loans issued over the June quarter were above 80% LVR)

I personally find these numbers very risky, especially interest only taken out with rates are at record low. I can’t see rate rises coming EVER on these numbers.

Investors prefer high LVR and interest only for tax reasons – i think this is not all that alarming.

I have friends who are investing that way (line of credit – interest only and 80%+ LVR) and myself have been offered a line of credit by my bank many times (and I am thinking about it!). It works as far as if you can ALWAYS afford the repayments. Once things go into liquidation you do not get out of it, you are toast. The current thinking is that with low rates you use the rent to do the repayments so you can be positively geared paying interest only and then profit from capital appreciation too. The problem is what happens when the RBA needs rates to go up. We go back to lower and lower peaking rates discussion we had before.

Which is why it is such a genius trade!

What’s wrong with investors buying property? They aren’t stupid – they must realise (like I believe) that property prices must go up for the economy to rebalance. The period of repressing consumption and other investment to make room for mining investment is over and these conventional drivers must and will eventually pick up again. Another thing is that most investors borrow against an existing property, so they tend to maintain overall LVRs > 80%. I also don’t think anything is wrong in borrowing >80% to buy a property. I certainly did (mainly to pay extortionate stamp duty!) and most people need to first time around.

Oops, I meant investors generally maintain LVRs < 80%.

Nothing is wrong with investors buying property. But banks should really make sure these are not subprime mortgages they are giving out and that they can withstand rates going up to 8%, properties prices falling 20% and unemployment going to 10%. Otherwise once again we’ll see private gains supported by public losses when/if things go bad. Both the Swiss and the NZ central banks agree. I think you are mistaken if you think the RBA will allow much house price appreciation from here. They want more residential construction not a new credit boom.

Well, they only have one instrument and they don’t get a choice.

I don’t think we’ll see 8% mortgage rates for the foreseeable future. And more importantly, unemployment going to 10% would be a massive failure of monetary policy that would most likely see the end of central bank independence, in my view, if it was accompanied by a non-zero cash rate. Maybe next slowdown, if the RBA lets this one linger and deepen.

unemployment did jump to 10% in the US, and in many EU country is still there, despite central bank actions (or because of them), because of bad real estate investments, it’s not something inconceivable.

Hi Ricardo, thought you might like this dashboard I created http://spark.rstudio.com/tim/AusEmploymentFlows/ (I got the idea from your transition charts a few months ago)

Wow, that’s really awesome. How did you get r to read the super table?

Unfortunately I can’t get R to read the supertable directly, I have to take it into excel.

I have started using the Quandl package in R (see quandl.com) as they scrape all of the ABS .csv data and I can set my charts up to update themselves without ever having to touch a .csv again.

Obviously you can’t (taper on that)…

The interesting question for us to consider is whether this is expansionary or contractionary. The rise in the AUD is contractionary on its own. Koukie reckons this will push back rate hikes. But it’s being caused by a drop in the USD caused by looser US mon pol, which should be expansionary, for us as well as them.

I thought the RBA minutes were pretty clear that easier financial conditions were required – but that they were hoping the fed would gift it to them via lower FX. if the AUD stays at 95c the RBA will cut again. Another jobs report like the last and low CPI and we will see 2.25% in Nov.

I think we need another cut anyway, but I’m not so sure about whether this news is contractionary… We didn’t think a fall in the AUD would prevent a rate cut, so why would an appreciation support a cut? The issue for me is, as always, what is causing the currency change. In this case, it’s a loosening of US monetary policy relative to expectations. Also, the SPI200 is up 1% in response to the news, suggesting no taper helps ease local financial conditions. But I am happy for commentators (and the RBA) to think otherwise!