The Federal Reserve’s decision NOT to announce a slowing of the pace of their asset purchases at their September meeting caught the market by surprise. Even with Bernanke’s prior guidance that “asset purchases are not on auto-pilot”, and that the policy was data dependent, few guessed that the economic weakness would stop Sep-taper (I made the same error).

In my view, the most interesting part of the decision was not the decision to continue buying at 85bn per month — it was the 2016 projections.

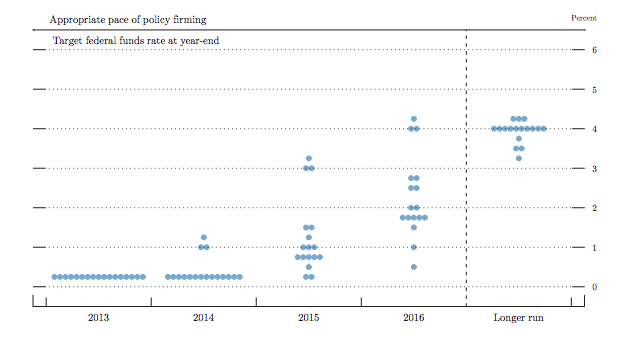

The voter-dots for the funds rate at year’s end in particular are far below market implied rates. Even after the post-fed rally, the Dec 14 Eurodollar (EDZ4) is about 16bps cheap (it should imply ~40bps); the Dec 15 Eurodollar (EDZ5) is about 18bps cheap (it should imply ~1.15%), and the Dec 16 Eurodollar is about 25bps cheap.

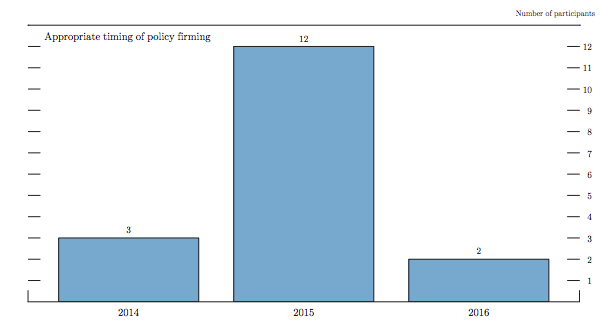

Even with the expected decline of the unemployment rate and increase of inflation, the median voter does not expect to get started with tightening until 2015 – and some think they ought to wait until 2016.

Why’s that? I think it’s because the headwinds to growth are very strong, so the natural rate has declined. Think of it as the voters saying that unemployment would be too high and inflation too low if not for easy money.

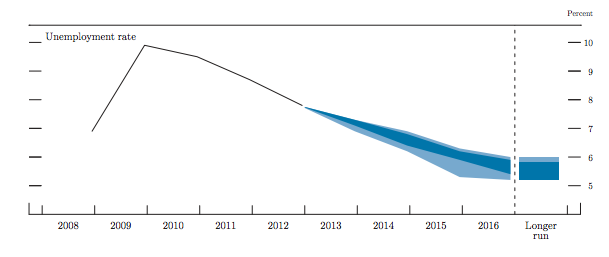

Unemployment projections were around where the market expected, with the economy returning to something like a full employment level of the unemployment rate in 2016. That seems reasonable to me.

Inflation projections seems a little too high to me. I don’t see much inflation pressure. In any case, the projections are for a pickup from here.

I have included the above projection charts mostly to give a sense of how broken the Taylor Rule framework is just now.

The technical way of saying this is that the natural rate of interest is lower — but i think the common sense way of saying it is that there are many headwinds to growth (both damage from the crisis, and other things such as the need for ongoing fiscal tightening) and that getting back to normal policy has to wait until these headwinds abate.

Additionally, the weaker USD has led to a stronger AUD. I think that an AUD above 95c certainly brings the RBA back into play for rate cuts. It also delays the hikes that are expected in other markets (such as Scandis and NZD) — i don’t see this as a fillup for growth, due to the Fed staying easier.

The Fed are staying easy because they cut their growth numbers.

Finally, did anyone else think that Bernanke’s coy answer about Fed leadership might be a hint that he’s staying on?

Monetary policy in the us is going to stay easy for a generation and the us is now definetely following japan. i think this shows what happens if a housing bubble burst. think about it… we are 5 years into this and the fed are still too scared too reduce buying by 10 b, the economy fundamentals must be very weak. At this point is legit to ask again for are the objectives of QE , it only looks like making the economy dependant on low rates. it also shows that as soon as printing is removed rates shoot up and the econony can’t handle it (so much demand has been carried forward). The RBA will not be able to cut rates much more if at all, that means the high dollar is something Australia will have to live with, which implies low rates, low inflation and low asset appreciation compared to the past. This decision by the fed was huge, it showed they will never be able to exit.

Ah, the Oz implications debate continues here. True, perhaps, that the Fed are staying easier because they cut their growth forecasts. But is that big news? And why would the US and Ox sharemarkets rally if that was the dominant message? As I said at the old thread, I am happy for the RBA to think this is contractionary, because then we are more likely to get the easier policy I think we need anyway.

Thanks for the voter charts. I think you’re right on inflation – will PCE really rise to 1.75% by the end of 2014 with those fiscal and other headwinds? Hmm..

what do you mean ‘why markets are going up’? they have just told markets that for now bad investments do not exist , it’s green light everywhere. everything can appreciate once again excl. usd. no matter if companies are good or bad, they will not be allowed to fail…. but the real economy, jobs, inflation that’s a different story.

My point was just that the so-called ‘green light’ should be seen as positive for our economy and hence, if anything, delay any further loosening. Ricardo and most others think the opposite. It probably depends on how one weights the importance of the various channels for mon pol to work and how rational one sees the markets. The fact is that investors think ASX200 companies are worth more due to no taper, presumably because it means their profits will be higher than otherwise. How could this be if the rising currency hurts them on balance? Maybe smaller companies or non-commodity exporters will hurt more.

Equity cost of capital is lower, but fx is higher – the question is if you think investment in non-mining is being held up by demand or cost of capital. My view is that expected returns are low as there is excess capacity, due to high AUD making imports cheap, and our exports expensive. If you think it is a financing thing, the higher equity market is easing. Of course, it’s made more complex by the wealth effect boosting consumption, but for equities i think that is second order.

RBA is closer to cutting after this … That is my firm view.

A 1% increase in AUD is much more restrictive than a 1% ASX 200 increase is easing. Since I still mainly play on AUD/USD over ASX200, I can tell you that the two are incredibly correlated. For instance today AUD is up 1.5% , ASX 200 < 1%. That is definitely tightening and it's significant to. However the last time AUD was at 0.95 it was may/jun and ASX 200 was 10% cheaper. So RBA cutting rates is not having much impact on exchange rate (that's more a fed play), but it does sustain shares and house prices. Actually I think FX is impacting house prices more than we think and more that rates, because it makes housing more expensive or cheaper for foreign investors who I understand are a big force behind Melbourne and Sydney house prices.

I hear the same about top end property and FX. Be interesting to see if things cool, now that AUD is 6% higher.

Hang on – equity cost of capital is lower because share prices are higher… sure I get that. But what caused the share prices to rise in the first place?

Change in US policy! I agree.

Now you might argue that this should send yields higher as it is good for growth – but we have a few effects working in various directions so it is not clear. I guess it is a judgement thing – my judgement is that we need non-mining to pick up, that the main impediment to this is the high AUD, and that the drag from the rise in the AUD more than offsets the boost from lower rates, higher equities, and better global demand.

Rajat, sorry to jump in, but the dynamics are clear:

– Australian shares are higher because RBA has cut rates (that’s the last 18 months medium-term story)

– Today Australian shares are higher because foreigners are in full force buying AUD + ASX 200 (ASX 200 in UAS is up 2.5% today). They have the prospect of AUD flat to rising that makes it easy to buy the 4% dividend yield of the ASX 200 and more for banks. Locals just buy because foreigners are buying.

– Prove of this is that when the fed announced tapering, the AUD started falling and the ASX 200 did too (why? because foreigners were selling to bey later cheaper) Foreigners were selling AUD and AUD assets. Once the initial sale was exhausted, when AUD stabilized around 0.90, foreigners came bank to the market and ASX 200 stopped falling and started rising.

– We are a small economy and a tiny market, foreign money is still dictating the direction of our financial markets so fx is key. When AUD falls, the market falls initially until AUD stabilize. When AUD rise, the market rises initially until AUD stabilize.

Ssec, you said: “Today Australian shares are higher because foreigners are in full force buying AUD ”

Ok, but if the rise in AUD is contractionary, why wouldn’t foreigners buy our bonds in preference to our equities, other things being equal? As in, if the market is in equilibrium before the change and bonds and equities are fairly priced in relation to one another, the no taper announcement means that bonds should become relatively more attractive than equities for foreigners. So bond yields should rise and share prices should fall.

it’s the old (boring) risk-on trade : more QE = USD down = commodities up = good for Australia. If commodities go higher , that could save us for a bit longer and RBA won’t be cutting rates anymore as we have more time to address the end of the mining boom.

reverse trade today… AUD/USD -0.5% , ASX 200 -0.5% (these are day trades, but over the longer term ASX200 does benefit from a weaker AUD, although one needs to account for commodity prices too, which usually track the AUD too and can weight on miners).

Buy everything, risk it’s ON! it does not matter WHAT you are buying. The fact that they downgraded growth and that obviously QE is not working as good as expected after 5 years is no concern for markets (today). If you have low rates and 7.3% unemployment or higher rates and 6% unemployment , for the markets make no difference. Money is being printed, inflation is contained, money is reaching for yields. Earnings are still OK. Poor are getting poorer and rich are getting richer.

There was a subprime mortgage company in the US (the name I forgot but it’s in this book http://www.amazon.com/Big-Short-Inside-Doomsday-Machine/dp/0393338827 ) that was impossible to short just before it collapsed in the GFC as it was paying a 12% dividend and it was too expensive to borrow and short…. then we all know how it all ended up.

My analysis of what is happening inside the fed is this:

– The US economy is actually doing not too bad. It would definitely warrant a taper of asset purchases right now. The fed agreed in the summer and things have not changed too much.

– Then the unthinkable happened. The USD shoot up and so did rates, especially mortgage rates. This was not expected. The market has tighten for the fed, much more than the fed intended to!

– So now the fed has started a fight to try regain control of rates and the (lower) USD which is needed for inflation They definitely do want to taper but without rates going too high, which the economy obviously can’t withstand, and again especially the housing market (shares are well behaved) Is that ever going to be possible???

– Can you have high bond prices and high share prices all at the same time without QE and money printing?

– If not, when will the US housing market ever be able to withstand higher rates? Never? It’s a dangerous game. The weakness in housing is going to persist for a looooooong time. And that is obvious now.

on the Taylor rule Glen Rudebusch from the San Francisco Fed had a god paper on that some time ago!