Regardless of what you think of the institution, the IMF’s article IV consultation reports are useful as a source of information (and in particular for a summary of what the ‘official family’ is thinking).

The Fund‘s 2013 Australia report reveals that staff think the AUD remains over-valued …

Despite some recent depreciation the real exchange rate, currently in the range of 89 cents to the U.S. dollar, is 5-10 percent above the level predicted by Australia-specific factors from a medium-term perspective

… and that the official family agree …

Like staff, they expressed some surprise during consultations that the exchange rate had remained high despite the decline in the terms of trade, although it has depreciated more recently. Going forward, a lower level of the exchange rate would help balance growth in the economy.

The too-high real exchange rate is a reason the RBA is unlikely to raise rates in response to the recent (AUD FX depreciation led) inflation bump. It would only make adjustment harder. Not only is the inflation likely to be temporary, but the higher rate of domestic inflation is pushing up an already over-valued real exchange rate; it would not do for monetary policy to make things worse.

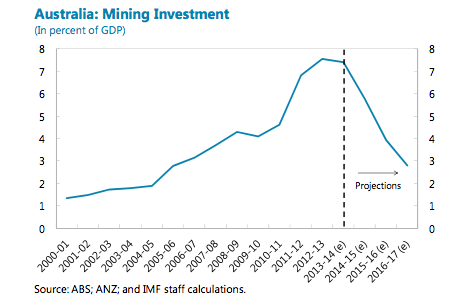

Like most other (mainstream) analysts, the IMF is concerned about the transition from mining investment. Note that the projected drop in mining investment is steeper than the boom, and takes us back to ~2005 rates of investment.

The Australian economy has reached a transition phase as the terms-of-trade-driven mining investment boom of the past decade has peaked and the economy is moving to the mining production and export phase. Mining-related investment is expected to drop sharply in the near term and a recovery in non-mining investment will be needed to underpin demand and return the economy’s growth rate to trend.

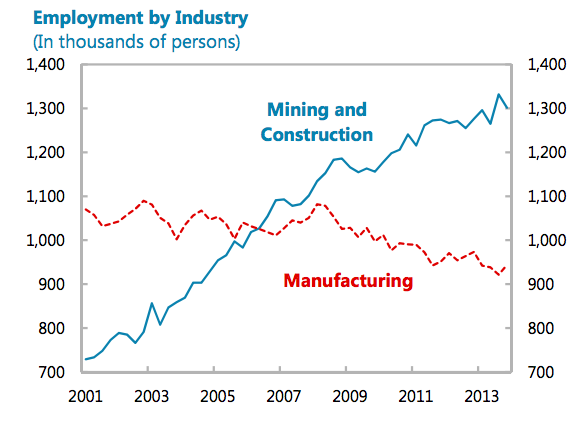

The fund support the mining story with a great medium term employment chart (below) which shows employment in mining and mining-related sectors v. manufacturing and manufacturing-related sectors.

A naive read suggests ~400k jobs in mining and mining related sectors will be lost if we’re going back to 2005. Sure, the sector is more than its investment share, but the move from investment to production will result in an employment decline of between two thirds and fives sixths of jobs (depending on the type of project) so there’s at least ~200k jobs at risk if mining is headed for an adjustment (and more still if China / EM cracks).

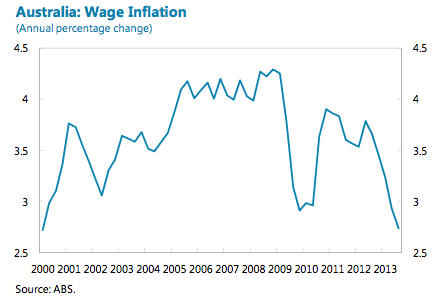

Given this outlook, and the currently low rate of wage inflation, it’s little wonder that the Fund is unconcerned about medium-term inflation risks.

Finally, on fiscal policy the Fund calculates that further fiscal tightening is required for the Government’s medium term objectives to be met. I expect further tightening measures to be announced in the May 2014-15 budget, following the recommendations from the commission of Audit.

The Government has committed to delivering a surplus of 1 percent within the next decade. Achieving this looks difficult on current spending plans without a large increase in budget revenue or a cut in spending or a combination of both

A tighter budget should help lower the AUD (less capital flowing in to buy bonds). The downside risks are low — the RBA can look after any demand short-fall by cutting the cash rate (which at 2.5% is high by world standards).

another good article.

What’s the beef about the IMF?

the budget will not be in balance if nominal GDP is 3%! when it gets back to trend levels the tightening isn’t so hard!

I like the fund, but not everyone thinks they are fair or money well-spent. I was trying to pre-empt that response.

Today’s unemployment numbers ….. I thought we were around the “peak” of our economic boom? Why are we at 6% unemployment already and the cash rate is already close to 0%? The last time the unemployment rate was at 6% (in June 2003) IR was at 4.75% after bottoming at 4.25%. It shows that monetary policy it’s slowly but inexorably losing its potency and it’s on its way to 0% (if not in this cycle then the next).

geeze don’t tell RA that. He needs looser monetary policy to offset his tighter fiscal policy which we do know actually works.

By the way when Swan brought down his very very tight budget the $A did not fall!

We need it ti fall if non-mining investment is to offset declining mining investment.

gosh if non-mining doesn’t offset the decline in mining investment and we get tighter fiscal policy we might just get a recession. might!

We all know there is no way non mining investment can fill that gap — it has got to be consumption, which is why the calls of ‘rate hike’ at the first sign of a consumption pick up are so odd.