RBA Gov Lowe gave the ABE Dinner speech this year — a speech entitled ‘Some Evolving Questions’. The speech looks at the transition away from the mining investment peak , the broken link between jobs, wages and inflation, and the risks arising from the high household debt to income ratio.

The title of the speech is a little dishonest. There’s really only one question that’s evolving — Lowe has made his mind up about the mining bust (all done now) and seems to have made up his mind about the trade-off with regard to financial stability matters at least 15 years ago. Debt to income is too high, and he’s not cutting unless it’s falling.

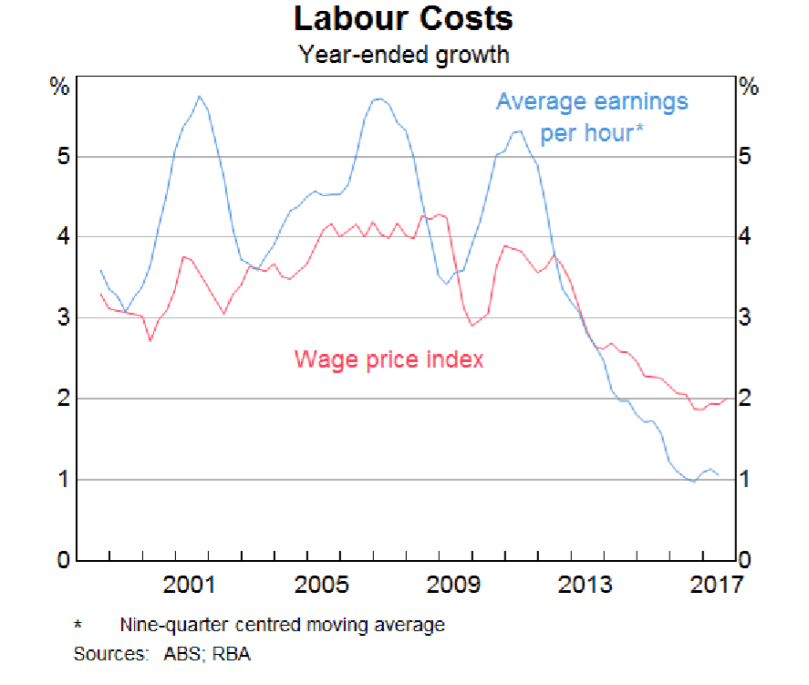

So the only real question is why solid growth and a tighter labour markets has not translated into wage and price pressures. The puzzle is summarised by the above chart — the NAB survey has detected labour shortages, and yet wages are languishing at all time lows of ~2% (and more like 1.5% if you take the Q3’17 number seriously). Indeed, if you allow for the fact that workers are transitioning from higher paying sectors to lower paying sectors, Average Hourly Earnings are actually growing ~1% (chart below).

The discussion of the mining transition in this section is a red herring. Australia isn’t exactly Robinson Crusoe. Even in countries that are clearly below historical estimates of full employment, such as the US, Germany and Japan, there is nary a sign of wage pressure. This isn’t about the mining bust or the transition to services.

So what is going on? Here’s my guess. Technology has massively increased global labour supply, and Europe is exporting their deflation.

It’s hard to measure, but my sense is that lower shipping costs and better technology has made it easier to distribute and coordinate work across the globe. This has increased the effective global supply of labour for any job, which is why there’s little wage inflation. This story, i confess, is not yet fully well worked out (hence my lack of charts).

The retail question is more obvious. A lack of organic growth opportunities in their home market — otherwise known as the depression in Europe — pushed European discount retailers to expand into new markets.

Attracted by the (previously) high margins in global retail, Aldi went into US retail, UK retail and Australian retail. These German retailers are private corporations and can ‘play the long game’ in these markets. This means multi decade expansions, as they grow their market share to ~25% (depending on the market they are single digits to low teens just now).

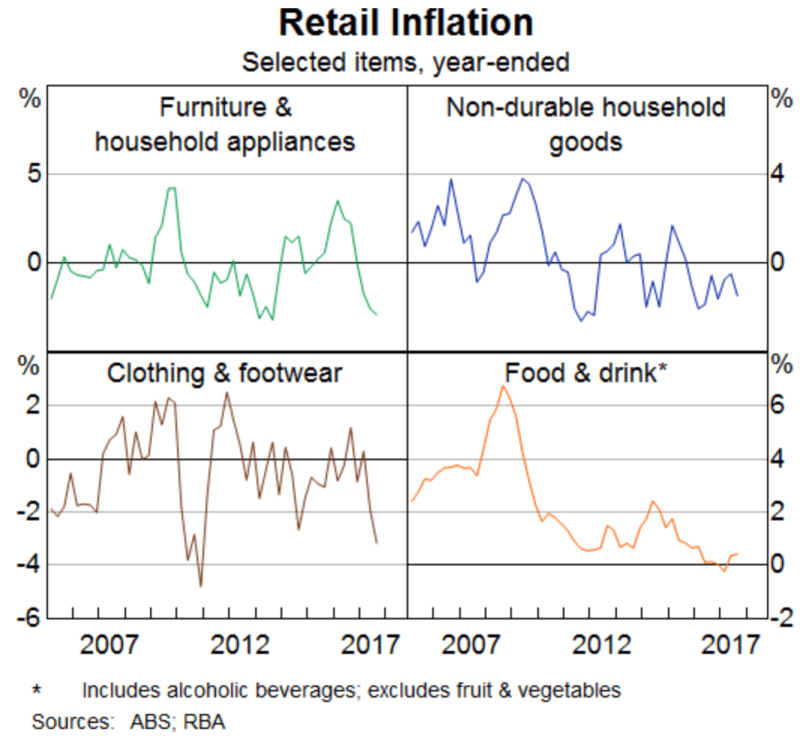

This hasn’t even got going yet in Australia. Aldi is still buying sites, and has barely opened in Perth and Adelaide. They’ll be able to screw prices down even further once they get a bit more scale. Their success will pull in other German discounters, and it’ll accelerate. This story is playing out to some extent in other categories too (H&M, Uni Qlo etc). This is why we’ve been seeing broad based retail deflation for a while now (below chart).

Amazon isn’t really a part of this story yet. This is just old fashioned German efficiency … Amazon will make it all hurt a little more.

Lowe acknowledges this in his speech, noting that ‘this still has some way to go’ and that wages and inflation are only expected to pick up slowly.

For me the policy take-away is clear. The RBA agrees that growth is much better, particularly the traditionally key labour market variables. However, they have low confidence that more jobs will cause wages to accelerate and drive core inflation back to their 2.5% target over the medium term. This means that they will be reactive to that pickup of wages and inflation — when they see it.

I find it hard to understand how folks can read this and still believe that Lowe will be raising rates preemptively, based strong growth and a forecast that wages will accelerate.

My guess remains that we’ll see the first hike in H2’19, but if wages remains subdued that’ll keep getting pushed back.

yep. agree.

It almost makes one a Marxist. Employers have all the power.

I have given this and the last article some modest publicity on my blog.

good to have you writing articles on a regular basis again.

Thanks mate

Do you really think he’s not cutting unless debt-to-income falls? That hasn’t really happened since the ’50s outside a recession, right? He seems to be putting a lot of faith (as is the Fed) in tighter labour markets stoking wage and price gains. I think this view is sustainable if unemployment is falling or at least steady – the RBA’s forecasts have given them a pretty easy pass on that. But if we see a hit to the terms of trade – say, because the Fed’s Dec rise spooks the market and we see some risk aversion in 1Q18, or the Fed over-tightens in general – then unemployment could rise. I think it would need to go above 5.75% to shake Lowe out of his complacency, but at some point his story would begin to fall apart. Any thoughts?

I think he has a very strong view that the stock of debt is the risk and that it is risky because it’ll accelerate any shock we see. To say he will cut in a recession is obvious I suppose. My takeaway is that the hurdle is high.

I guess the issue is how high. I don’t think it has to be a GFC-style event, even a slow melt upwards in UnN could do it… Anyway, it’s a bit incongruous how they expect businesses to invest and hire and pay higher wages if they’re basically saying they’re comfortable with slow growth. Markets infer the stance of policy from words backed up by actions, not exhortations.

Yes I agree. The bit about firms investing and that driving consumption growth via incomes was very classical.

The stock of Household Debt is too high because the stock of Government Debt is too low. All very easily explained by the sectoral balances….how it is possible for any professional economist including Phil Lowe is behind me.

https://www.bennelongfunds.com/insights/271/australia-the-lucky-country-or-is-it#.Wicrw7ZL0dU

If he wants households to de-lever he must front parliament and demand big tax cuts and/or spending increases.