The decline of the unemployment rate to 4.9% in February caused the market to substantially reduce the implied probability of a rate cut in May. This is understandable, but i think it’s wrong.

What’s wrong with this is that the unemployment rate is a lagging indicator. Monetary policy works with a lag, so a central bank must be forward looking. Because growth leads employment, being forward looking basically boils down to responding to changes in the growth outlook.

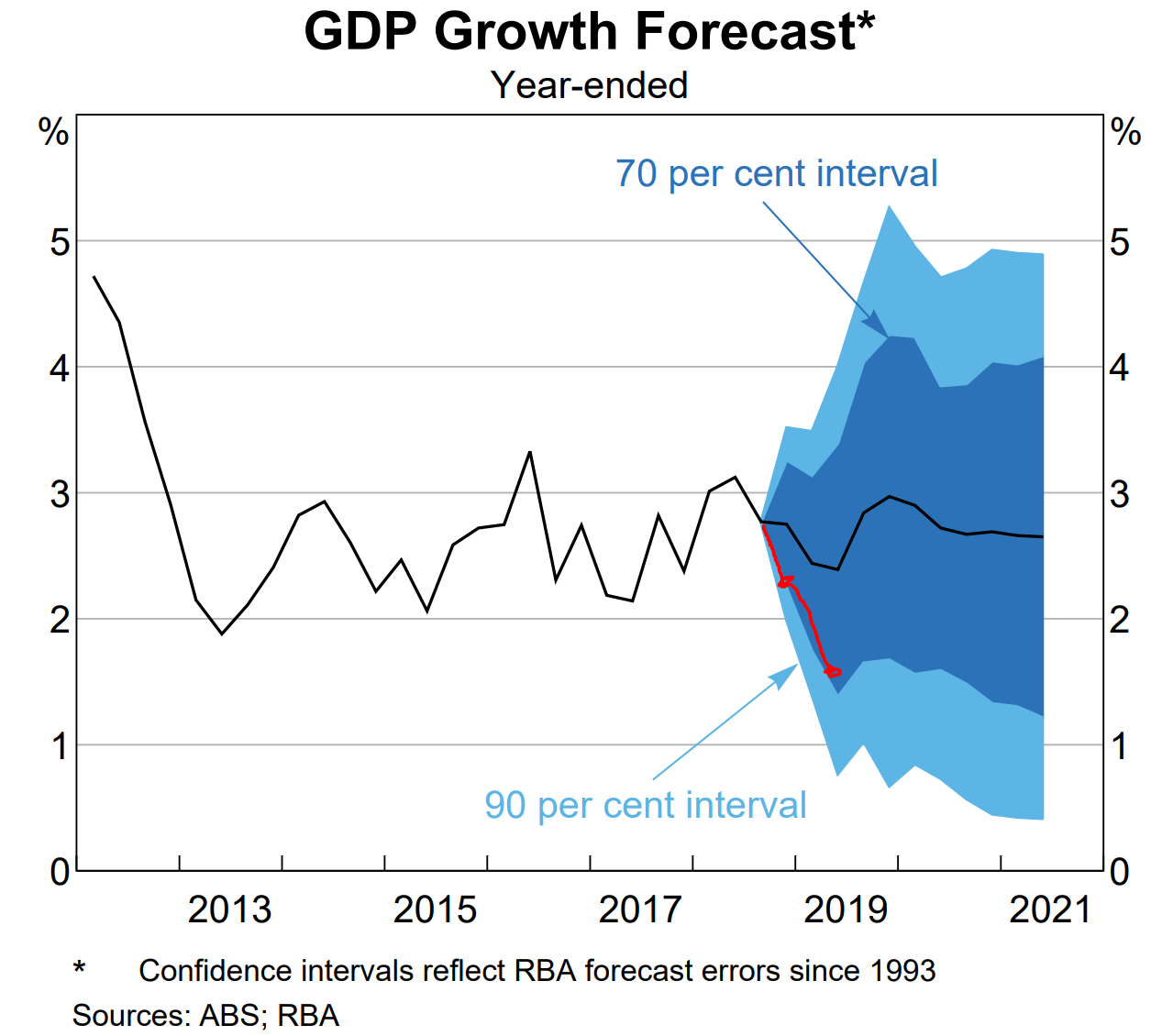

The growth outlook has changed a lot since the February SOMP. Q4’18 GDP printed at ~2.3%, or about 50bps below the RBA’s Feb SOMP forecast. Assuming that Q1’19 is around the same as the average of Q3 and Q4 2018 (the partial data suggests that it’s worse) the pace of growth will slow to ~1.5%yoy in H1’19, or about 100bps below the RBA’s February forecast.

Given potential growth of ~2.75%y/y, GDP growth of ~1.5%y/y should deliver a ~50bps increase of the unemployment rate by the end of 2019.

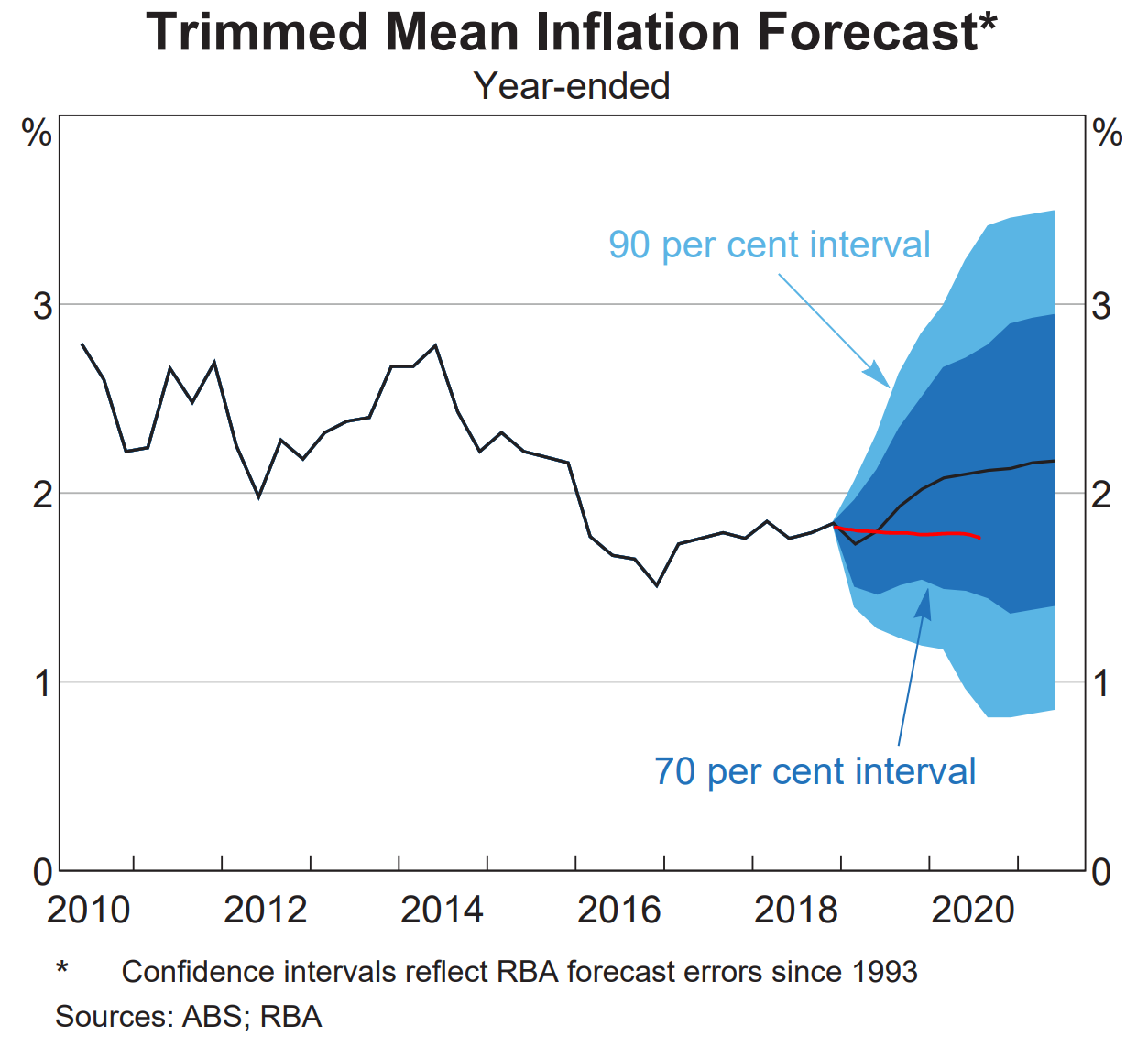

With the unemployment rate rising, i don’t see how the staff could forecast an accelerating rate of inflation. Increasing slack is typically associated with a decelerating pace of inflation. At best it’ll be stable at ~1.75%

Given the size of the GDP slowdown (that is pretty much baked in by the base effects) the staff are very likely to forecast rising unemployment and slowing inflation.

The question is if Gov Lowe will be forward looking and will respond to the forecast downgrade — or if he needs to see a higher unemployment rate and a still-slower pace of inflation to act.

When he last spoke to Parliament, Gov Lowe said that he would be concerned about inflation spending too long below 2% as it might depress inflation expectations. In the month since he spoke, that is exactly what has happened.

Inflation expectations have collapsed. The market thinks that the RBA doesn’t care about low inflation — and as a result market based measures of inflation expectations have fallen by ~70bps since mid’18 & ~15bps since mid-Feb (here i’m using the RBA’s 10yr bond and indexed yield from the capital market yields tables).

I think the market’s wrong. I think that Gov Lowe does care about his inflation target and that he will respond to slower growth and plunging inflation expectations by lowering the cash rate.

The obvious time to do it is at their 7 May meeting — in response to a slower growth forecast, a higher unemployment rate forecast, and a lower inflation forecast in the SOMP.

I respectively disagree – I think it’s pretty unlikely. Here are my reasons, based on Lowe’s statement to the HoR on 22 Feb (https://www.rba.gov.au/speeches/2019/sp-gov-2019-02-22.html):

1) I couldn’t see any concern about inflation spending too long below 2% and the effect on expectations. Did I miss it?

2) Lowe notes that since his previous committee meeting 6 months ago. growth has been weaker but employment has been stronger, and he cares more about the latter, which he saw as falling – rather than rising – as recently as a month ago.

3) He attributes low inflation to one-off factors like drops in childcare costs and petrol prices (although petrol seems to have risen lately) and appears willing to look through a weak March CPI.

4) Lowe *is* concerned about consumption growth, but he says the RBA is forecasting improvement due to faster wages growth and tax cuts. Unless the Government disappoints on this front at the (pre-election) Budget – surely, a remote risk – Lowe will remain sanguine. Intriguingly, Lowe seems to have a bastardised classical model in his head, where the supply side/ labour market drives real output growth, as well as growth in nominal wages and prices.

5) Lowe thinks monetary policy is currently highly stimulatory. He views the low level of rates as indicating the stance on monetary policy, rather than inferring stance from recent and expected inflation outcomes.

6) In describing the state of the world in which the RBA lowers rates, Lowe says, “But it is also possible that the economy is softer than we expect and that progress towards our goals is limited. If there were to be a sustained increase in the unemployment rate and a lack of further progress towards the inflation objective, lower interest rates might be appropriate at some point.” I take this to mean he needs to see the whites of the eyes of higher unemployment before moving.

7) Finally, I think Lowe is – if not quite an ideologue – hugely committed to maintaining or raising rates to deter debt accumulation and to provide more ‘ammunition’ for fighting the next downturn. His path of least regret is to wait until rising unemployment happens rather than be the wimp who wasted the RBA’s precious ammo on fine-tuning. The RBA got zero flak when unemployment got to 6% a few years ago when other countries rates were falling, so why not wait until it is at least solidly on the rise? Conversely, if Lowe left Australia with a 1% OCR at the start of a new US recession, he would be pilloried. The paragraph in his statement that refers to high private and public debt levels and low real rates also refers to ‘resilience’, ‘buffers’ and ‘room to manoeuvre’. Lowe’s idol, Claudio Borio, recently published a paper arguing central banks set real interest rates in the long run. https://www.ft.com/content/08c4eb8c-442c-11e9-a965-23d669740bfb If Lowe has any sympathy for this view, he will be most disinclined to cut before he has to.

There’s a section in Hansard where Lowe says that he’d be concerned if he thought inflation was going to stay below 2%. Ultimately that’s why i think they cut. I just don’t see how the forecasts can have a falling unemployment rate and accelerating inflation given the recent growth data.

“Lowe: If I thought inflation was going to stay sub two per cent indefinitely, then I would be quite concerned about that, because what would happen is inflation expectations would become lower and it would be hard to get inflation up eventually. So I would be concerned if inflation was going to stay for a long, long period below two per cent. But that’s not our central forecast. We see inflation gradually picking up.” Page 15. https://parlinfo.aph.gov.au/parlInfo/download/committees/commrep/b9c7ee3a-c926-4f3e-acc4-cf5b8809f649/toc_pdf/Standing%20Committee%20on%20Economics_2019_02_22_6971_Official.pdf;fileType=application%2Fpdf

That sounds a bit motherhood to me. ‘Indefinitely’ being ‘a long, long period’ is a very long time!

Re my point (2), I meant the RBA saw the UnN rate as falling rather than rising as of late Feb.

I see the Kouk is calling d for an april rate cut.

RA and the Kouk on a unity ticket. Me thinks the RBA does not think the economy is that weak as yet.

CBA says they have solved the tension between the labour data and GDP data. They say it is the result of falling real labour costs.

Gosh I wish I had said that. wait i did.

We have a deregulated labour market and people are only now starting to realise the implications of what it means