RBA Assistant Gov (Economic) Luci Ellis this morning gave a very careful speech on the household sector. In particular, it goes into some detail about why household income in the national accounts has looked so weak despite a firm labour market — but what’s really notable about the speech is that it seemed to add a consumption trigger for rate cuts.

“Household consumption spending is a large part of economic activity. A significant retrenchment there would lower growth and feed back into a weaker labour market, as well as into decisions to purchase housing.”

This means the RBA could cut rates if they become convinced that there’s a significant retrenchment of consumption underway.

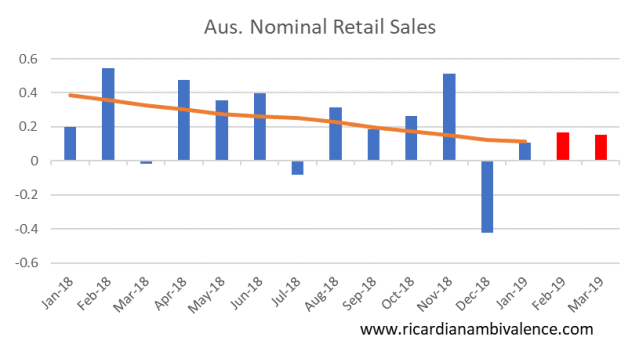

This is highly relevant, as the RBA gets both the Feb and March / Q1 retail trade reports before the May RBA decision. The Feb report is 3 April and the March (+ Q1) report is Tuesday 7 May — a few hours before the RBA’s May announcement.

If we assume that Feb & March nominal retail sales is ~20bps MoM (which is better than the present trend of ~10bps per month), nominal retail sales growth in Q1 will be about +20bps QoQ.

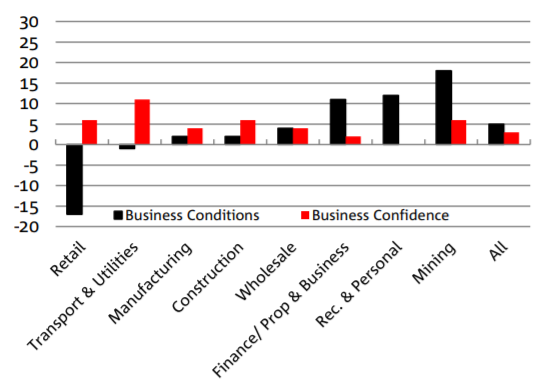

Assuming quarterly retail inflation is flat (the lowest over the prior year is +10bps), this would deliver real retail sales of +20bps qoq. The risks around this number are to the downside. The survey data suggests an ongoing deterioration of of retail conditions. The NAB business survey for Feb shows that conditions in retail sales continued to soften in Feb (chart below; Jan was -11pts; the Q3 average was -5pts).

I would imagine that the RBA is hearing similar things from their business liaison program. Perhaps this is the meaning of RBA Ellis’s comment that they are closely watching consumption. If the hard data follows business sentiment, the RBA would become fairly certain about a rising unemployment rate over time. The RBA could react to their higher unemployment rate forecast and cut rates in response.

Ellis concludes that:

“… demand for housing rests on the household sector’s confidence and capacity to take on the financial commitments involved in the purchase or rental of a home. Without enough income, and so without a strong labour market, that confidence and capacity would be in doubt. This is not the only reason we are watching labour market developments closely. But the nexus between labour markets, households and housing are crucial to our assessment of the broader outlook.”

This is the common-sense point that weakness in the retail sector would make the housing adjustment more difficult.

By the way, this much is true about any source of weakness — the downside risks to the Australian economy from slower global growth are amplified by the currently fragile state of the housing market. A global shock that pushed up the unemployment rate would increase the length and severity of the housing correction — and thereby increase financial stability risks.

Great post 😁

“A global shock that pushed up the unemployment rate would increase the length and severity of the housing correction — and thereby increase financial stability risks.”

This is exactly Lars Svensson’s argument against “leaning against the wind”: leaves you with a weaker starting point when a negative shock arrives.

I think i will put it down to good fortune that I’ve wondered into such good company.

retail trade is only 40% of consumption these days

So perhaps they need to see the national accounts to get a view on non retail consumption?

I thin bk that is what I was saying. Consumption of services is more important than the consumption of goods

That’s true — but there is more to it than that. For example it is also true that manufacturing tends to lead the global cycle and it’s by far the smaller part.