My judgement is that the RBA was truly open minded about both the extension of YCC and appropriate pace of QE when they announced the review of QE at their 4 May meeting. A prospective upgrade drove their 6 July decision to taper; but if there had been a downgrade, things would have been different. They would not have tapered QE, and they may have extended YCC to Nov’24.

The current COVID/Delta outbreak has delivered that downgrade. Forecasting the pandemic and recovery has been hard, so don’t take the below too seriously — the main purpose is to show that the near-term is likely to be below the May’21 downside, and that the recovery to the May’21 baseline is likely to take some time. So easing should be considered.

The RBA created scope to reverse their taper, and potentially increase the pace of QE, in their (likely heavily airbrushed) July meeting minutes. The minutes noted “the high degree of uncertainty about the economic outlook” and reported agreement that the new framework gave them the “flexibility to increase or reduce weekly bond purchases in the future, as warranted by the state of the economy”.

Is there capacity to increase QE?

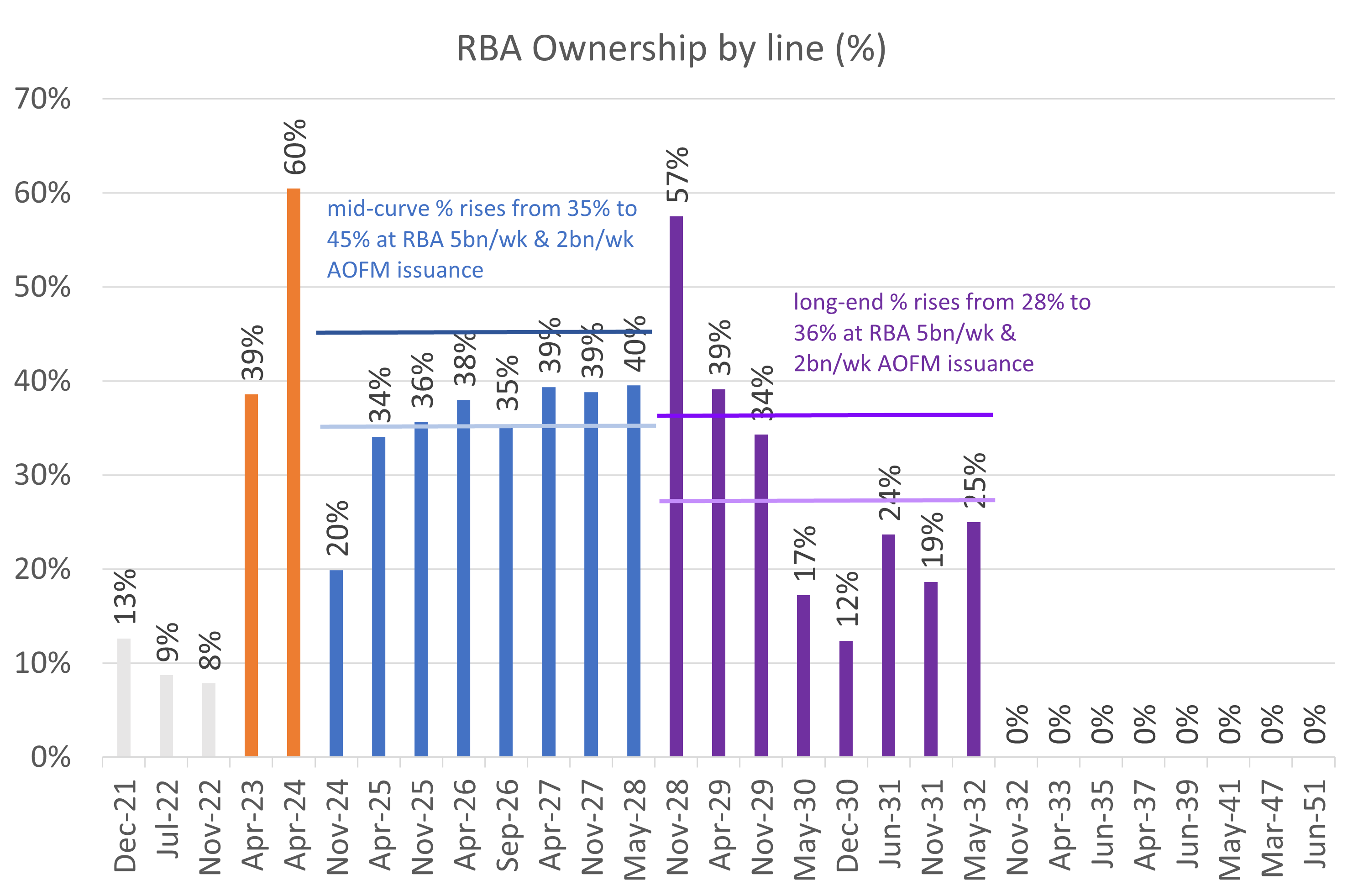

The problem with QE is that central banks can run out of bonds to buy. The design of the current QE package means that the RBA’s ownership of mid-curve bonds (the ones the RBA typically buys on Monday) may hit limits if QE goes for too long.

While that’s not a current problem, it is a looming issue given current QE program design & AOFM issuance patterns.

The RBA has purchased 136bn of bonds (not including their YCC related purchases) since the QE program began on 11 November 2020. The AOFM has issued 76bn, and only 69bn in the sector the RBA buys, since that time.

As a result, RBA ownership of the mid-curve and long-end bonds has risen to 35% and 28% respectively. RBA ownership will rise to 45% and 35%, respectively, by 11 November (assuming the RBA dumps the taper and maintains the current pace of QE at 5bn per week; that the AOFM increases the pace of Bond issuance from the current 1.5bn/wk to 2bn/wk; and that issuance per line is broadly consistent with H1’21). The RBA’s share of the mid-curve bonds will keep rising until the program tapers down below 2bn per week.

If the RBA accelerates the pace of QE, the problem becomes more pressing. Assuming the RBA buys 6bn/wk, RBA ownership of the mid-curve and long-end bonds rises to 47% and 38% respectively (on 11 November 2021). Some of this will be offset by faster issuance (a worse economy creates bond issuance), but it’s not much help for the mid-curve. The AOFM delivers only 30% of supply into the mid-curve bonds, so RBA holdings of mid curve bonds creeps up to 50% by the time QE ends.

Nor will the roll-down of bonds into the RBA’s eligible universe solve the problem.

The next bond to roll into the mid-curve group is the Nov’28; the RBA owns 57% of this line. So the addition of this bond to the mid-curve group won’t add capacity. The only fix is a change to the AOFM’s issuance strategy such that they issue more mid-curve bonds.

In contrast, the RBA owns none of the November 2032s or longer bonds. So as these bonds roll into the long-end group they will add capacity to the long-end part of the current QE program.

Happily this problem is self-inflicted and so easily solved. The RBA could add ultra-long bonds to their shopping list. This would add a little over 100bn to the eligible universe and lower the RBA’s ownership of eligible ACGBs by about 6 percentage points. It may also increase the potency of QE, as buying longer-end bonds would mean that the RBA was withdrawing more ‘risk’ from the market for each dollar spent.

The other option is to boost the share of Semis from the current 20%. At present the RBA buys 1bn per week of Semis, and holds 35bn of Semi Government bonds — which is about 16% of total outstanding bonds for the Semis they buy. If the RBA were to increase the proportion of their bond buying allocated to Semis, this would delay the day that concentration becomes a constraining factor for QE. If they extended to Ultras-Semis, it would increase the total pool of assets a little further again.

If things get bad, the RBA should consider doing both: buying ultras and increasing the share of semis in their bond buying operations. This would both increase the potential life of QE, and boost their easing-credibility (more ammunition = more credibility).

They should also re-consider the decision to freeze QE at the April’2024 bond. Rolling YCC to Nov’24 boosts forward guidance and is a substitute for QE. More non-QE easing defers the day that ownership limits might be a constraint on QE. Simply saying that it’s back on the table (or was never off the table) would be helpful.

Finally, I don’t see much prospect of the TFF returning unless funding markets become strained.

One comment

Comments are closed.