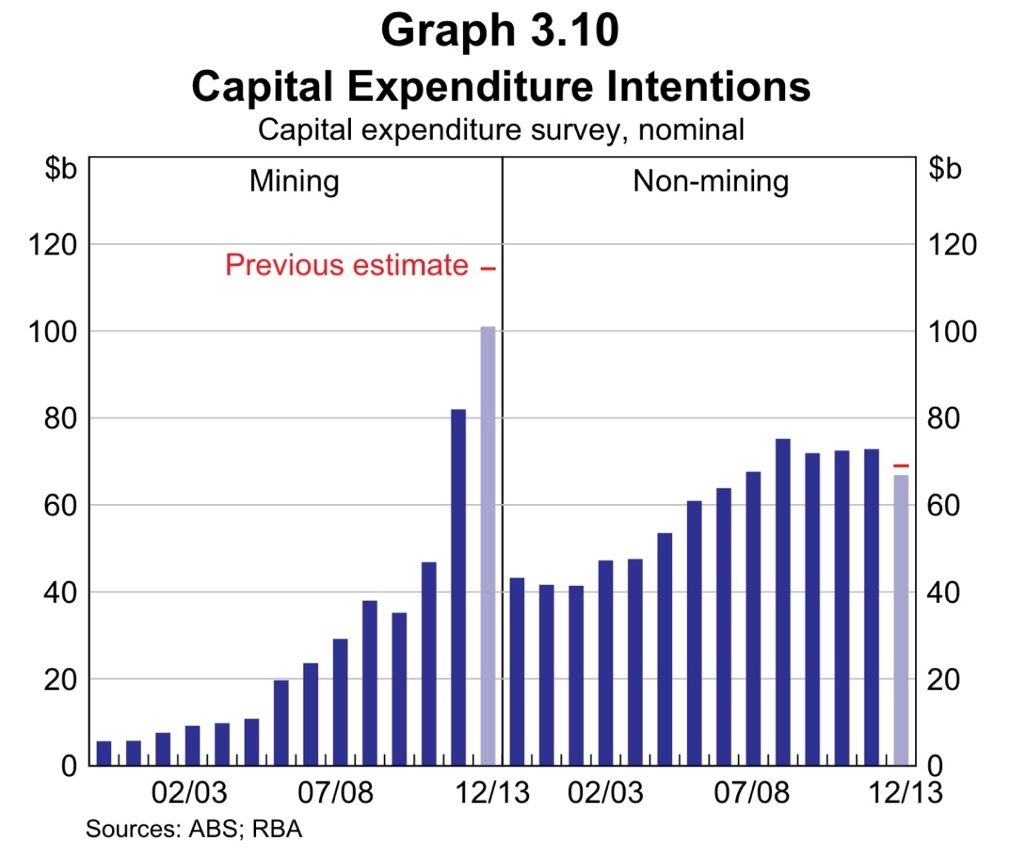

Today is the keenly awaited Q4’12 Capex report. The prior report showed an ongoing increase in current activity but signalled an approaching peak in mining investment.

As a result of this (and doubtless liaison with the big investors) the RBA cut their capex forecast in the Q1’13 SOMP.

This is a natural consequence of the decline in the profitability of investment. Mostly, the decrease in profitability is due to a decline in the terms of trade — however a part of it is due to poor cost control, including inept management of labour related issues.

With the RBA maintaining an explicit easing bias, the question really is what capex number would get them to act on that bias and to cut rates.

I think that clear evidence that the investment boom was about to end abruptly might get a rate cut in March. It would have to be clear enough that investment was anticipated to decline in both the mining and non-mining sectors.

The story of the boom has been of the non-resource sector slowing to make way for the resource sector. At first, inflation took our purchasing power, as the RBA did too little. Next, the RBA tapered demand (they probably did a little too much). Now, with the mining sector slowing there is scope for the non-mining sector to grow more (it must, to absorb the capital and labour that the mining sector will shed).

Right now, while i judge that things remain subdued, i can also see that the prospects of the non-mining sector have improved markedly. Financial markets have delivered a big easing of financial conditions (via asset and securities prices, and issuance conditions). This seems to be worming through confidence and ought to show up as increased demand.

Related to this easing of financial conditions is the ‘unofficial rate cut’ business already obtained in Q1. Corporate borrowers often borrow at a margin to the 3m bank bill swap rate, and due to the improvement in financial market conditions, this rate fell from ~3.1% after the Dec rate cut to a low of ~2.9% in mid Feb.

So while i do agree with Terry McCrann that a bad number could cause a cut in March, it would have to be a very bad number – for the RBA is already expecting a modest decline in investment over the projection period, and markets have already eased monetary conditions (which is a substitute for further policy easing by the RBA).

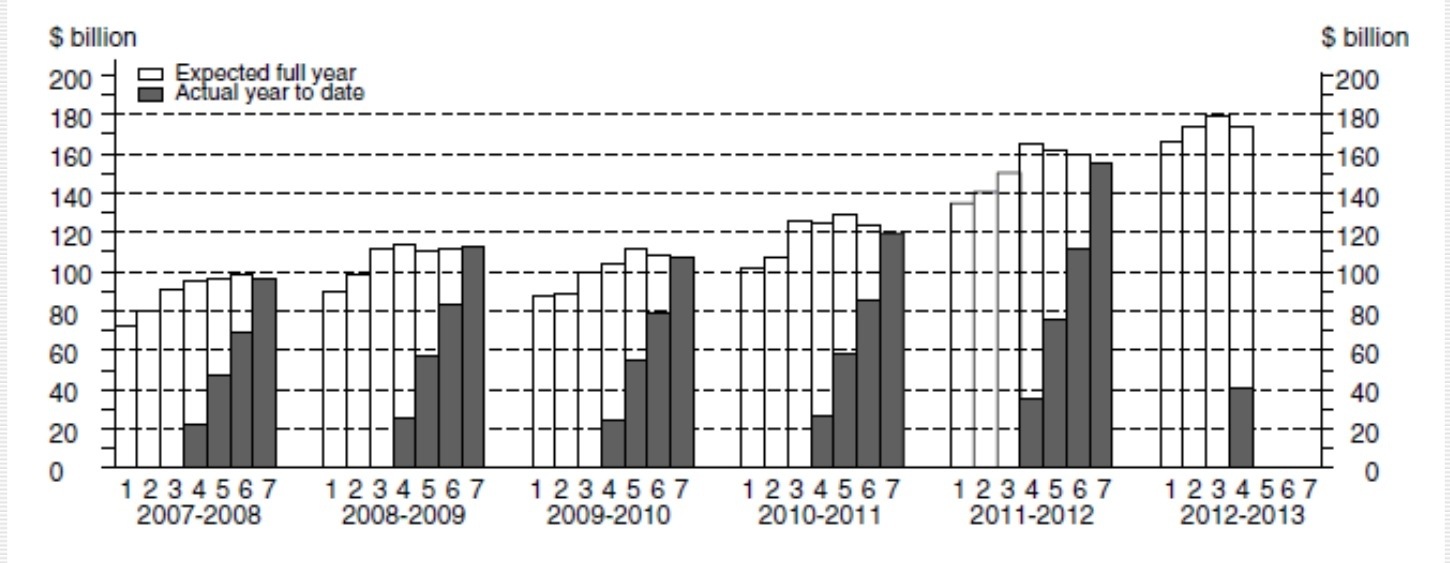

The RBA is estimating about 165b as total for this fiscal year. Last year we got actual just under 160b, and the report estimates, for this year, so far are at ~170b. Being this the Q4-12 report where many commodities prices were collapsing, there’s a chance the numbers are going to be weak. I’d say we get the same estimate for this year between $165b and $170b. But the key number is the first estimate for next fiscal year (no RBA forecast for that?). If the first estimate for next fiscal year is below $160b then the mining peak is clearly in sight. Actual year to date also important (will it be higher than last year?)