The January PCE report suggests that it remains way to early for the FOMC to be looking for the exit. Inflation is low, and personal income remains depressed.

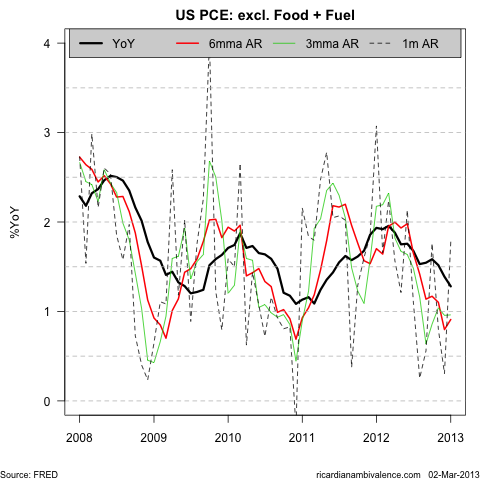

There is a hint of residual seasonality even in the seasonally adjusted PCE deflator. After a period where core PCE inflation has been low, the core PCE deflator picked up a to 1.8% AR. An acceleration is common in January (the AR was 3.1% in Jan’12 and 2.2% in Jan’11). Over the prior three months, core inflation has been running at ~1%y/y, and over six months, core inflation has been running at ~0.9%y/y. The Fed’s target is 2%, so this is clearly too low.

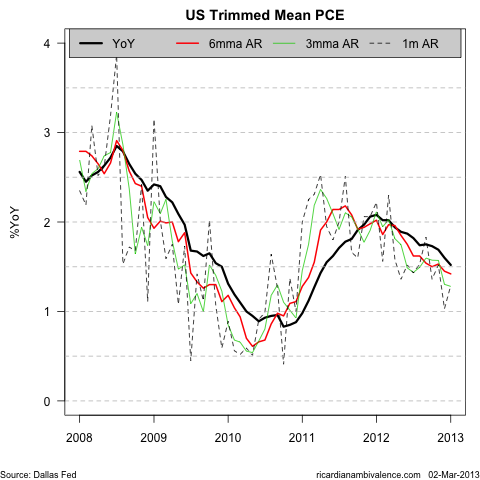

Being Australian, i prefer statistical exclusion measures, and these are also low. Trimmed mean PCE is also low — but not quite as low. In January, trimmed mean PCE was ~1.3%, which is around the average over the prior three months, and a little below the prior trend (6mma AR is 1.4% and 12mma AR is 1.5%). This reflects the absence of headline commodity price driven inflation pressures.

A part of the weakness in global inflation reflects the stability of commodity prices, and the other part reflects the weakness of personal income (weak income growth means weak spending power).

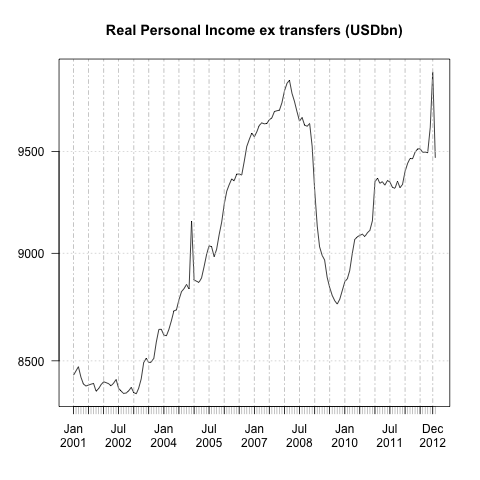

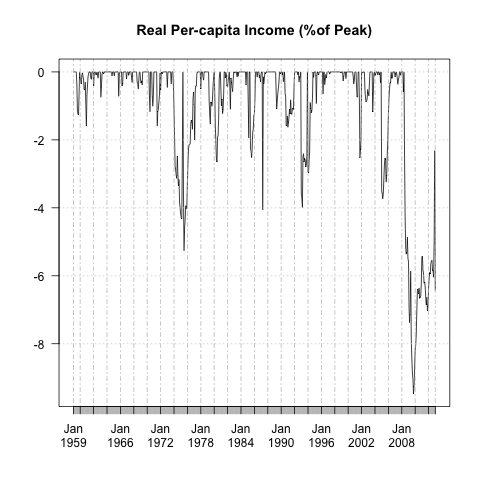

Excluding transfer payments, real personal income remains below the pre GFC peak.

The drop in personal income looks recessionary, but it’s not as bad as it looks. The move is exaggerated by folks having pulled forward income into Q4’12, in part to beat the tax hikes. Smoothing through all this, income (excluding transfers) probably remains about 4% below the pre GFC peak.

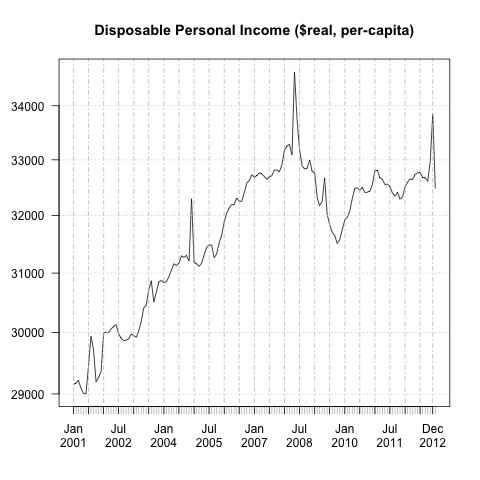

Taking population growth into account, folks are even further behind. Even with the recent income spike, real per capita income remains below the 2008 peak, and after smoothing through the noise is probably ~6% below the peak.

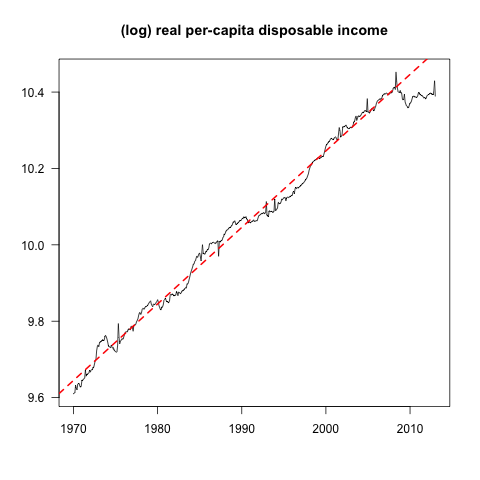

This is where i think folks like Sumner are on the money — that income growth has not met (reasonable) pre-crisis expectations is depressing activity and demand. The trend for real pre-capita income growth used to be ~2%y/y — but since 2008, there’s been basically no growth at all.

I think that these two trends are closely related. Weaker than expected income growth is depressing demand, as households with less income than expected are be more careful with their money — and this tends to reduce firm’s pricing power.

Very good so it has been added.

Why is this being done on the week-end?

My excuse is rain has caused cricket to be abandoned.

by the way I love the dig about trimmed mean etc

Yeah, the rain has kept me in. Also, i like this pce inflation report. And it was an excuse to play with r and vim…