The March RBA meeting has the feel of a ‘dead rubber’, with only 3.5bps of easing priced (a 14% chance) and a sense that there needs to be a big shift in either direction for the RBA to move from their easing bias to something else.

There have been some developments that may boost their demand forecast – the decent Q4’12 capex report and the weaker AUD – however on balance i think they will retain their easing bias.

Even with this judgement, however, i don’t see a move in April. The easing from the financial market and commodity prices is still working its way through, and this takes pressure off the RBA. At this point, i still think that the next move is down, and judge that the earliest realistic easing window is at the May meeting, following the Q1’13 CPI report.

(Guessing) The March Statement:

Global growth outlook — unchanged. The better US data balances sequestration; China seems okay. The italian election jitters are the sort of instability the RBA has been expecting.

Commodity prices — watch for an upgrade. The RBA’s index was up again in Feb. A robust 3.6% increase in AUD terms (2.4% in SDR terms), taking the YoY decline to a modest 4.8% (7.2% in SDR terms). The declining AUD is helping out here.

Financial market sentiment — stable at a robust level. The way equities and credit handled the risk events of the past week is encouraging.

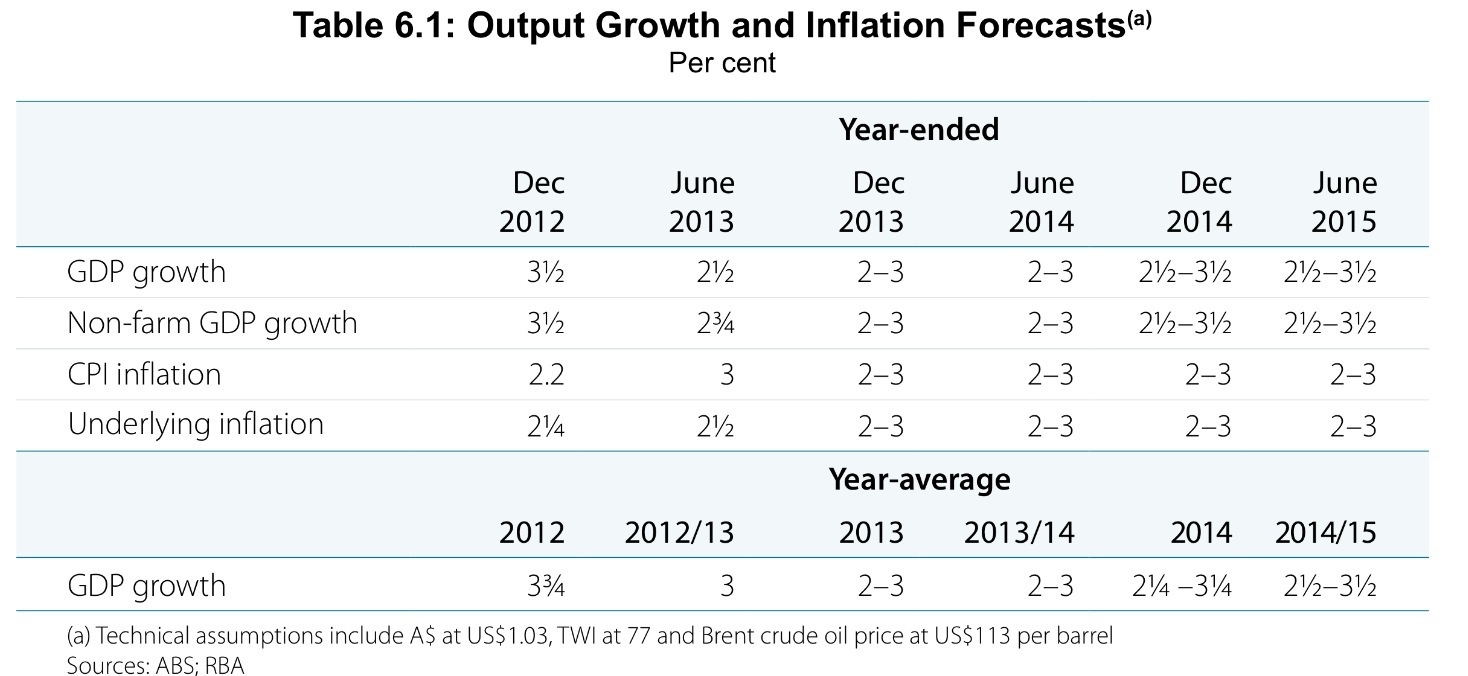

Domestic growth — this is where things get harder. The way the quarterly partials have been rolling in, it is hard to see the ~110bps of quarterly growth it requires to hit its Feb SOMP forecast of 3.5%yoy growth in the year to Q4’12, but the outlook may have improved.

Offsetting the current weakness is the decent Q4’12 Capex survey.

The RBA had been expecting a capex droop for 2013-14, but the first ABS survey suggests a plateau at ~8% of GDP in 2013-14. Without a capex droop, the period of sub-trend growth in the forward estimates (which really is the bit that monetary policy can hit) will be delayed (i do still think it must be traversed at some time).

This is not to say that things are going well, for they are not. The RBA has put the emphasis on GDP for some reason, when income measures that capture the terms of trade better tell the story.

This is why firms lack confidence and inflation has been weak – the aggregate economy has lacked for income growth. The recent increase in commodity prices should boost H1’13, and repair some of this damage.

In the inflation paragraph the RBA must balance up weaker than expected current conditions with a lower probability that their weak Feb’13 demand forecast (a period of sub-trend demand as the mining investment boom rolls off) will prove accurate. On net, i would hedge and leave this paragraph more or less the same. The Bank’s assessment is therefore likely to remain “that inflation will be consistent with the target over the next one to two years”.

I similarly expect that the monetary conditions paragraph will be mostly unaltered. The RBA may add something to acknowledge their pleasure at seeing a weaker AUD, but i think the probability is low. They may say it is more in line with fundamentals, given its lower level and higher commodity prices.

With all that, i expect that the RBA will retain their easing bias, but retaining the comment that the inflation outlook “affords scope to ease policy further, should that be necessary to support demand”. The risk is that they drop the easing bias due to capex, but that was only a first estimate, CPI may still be slowing, and current growth seems a bit sub-trend, so i expect it will remain.

Wow looks like Chris Joye has certainly been vindicated by the retail data on his thesis that the cautious consumer is way behind us….

Seasonal adjustment?

I expected this retail bounce too. Dec has been downgraded from -0.2% to -0.4%. January/February data has been good so far. But it’s summer data. After 3 negative months of retail sales incl Dec, people obviously waiting for January deals.

PS This is a great blog, it would be nice not to spam the comment section. I guess yesterday’s 0% TDI inflation number vindicated CJ too? By the way, where can we find CJ forecasts (rates, GDP, inflation) for 2013? Not that we care after last year’s call:

http://christopherjoye.blogspot.com.au/2011/09/officially-australias-biggest-dove.html

I think what’s happened is that christmas shopping has moved online, and therefore out of the retail trade survey frame. This means that the christmas surge isn’t as large as the historical seasonal factors ‘expect’ which means the seasonally adjusted number is biased down in dec and up in jan. the trend has improved from 0%mm to 0.1%mm, i think that is about right.

Trend 0.1% does not point to inflation above target… if anything below target.

Agreed: and also the strength was all in the little guys (the sampled or non- CE bit). Could be that the little guys were too weak before and that it is a correction back, but it is hard to put full faith in the MoM move.

Did anyone notice the 25%qoq surge in public investment? Wow. Surely that drops out in H1’13

Want to check some proper forecasting? :) Have a read:

https://ricardianambivalence.com/2012/08/18/lunch-still-costs-fx-intervention-edition/#comment-2175

then AUD was at 1.05 and ASX 200 at 4300

CJ has been incredibly accurate on house prices–calling recovery correctly in 2012, on equities, calling rebound in 2012 and 2013, and unlike others has got every Oct, Nov, Dec, and Feb RBA move right. i like reading him personally. his genius is undoubted. tho nobody is perfect

That’s fine, but why do you keep mentioning him on this blog? If we want to read about his genius thinking we know where to find him.

One more genius forecast here:

http://www.businessspectator.com.au/bs.nsf/Article/house-prices-property-rise-fall-forecast-market-bu-pd20120125-QTV3R?OpenDocument

Published 11:06 AM, 25 Jan 2012 Last update 12:05 PM, 25 Jan 2012

“If the RBA cuts again in February, and further thereafter, as some analysts believe they will, expect to see the return of rapid house price appreciation”

Rapid house price appreciation in 2012???? Genius.

I don’t mind is Chris’s fans want to talk about him in the comments, but i will put a stop to it if the real contributors get annoyed.

i figure that those who make a substantive contribution to the discussion add a lot, and that ‘likes’ for chris (unless they are on topic) add less.

I am sure you all will let me know as and when :)

+1 ssec

Without looking on a line-by-line basis, the RBA statement looks very similar to last month’s. Perhaps a bit more dovish than many expected?

I compared line by line and I think it’s slightly more hawkish than last month, on commodity prices, housing and positive impact of previous rate cuts. The conclusion is the same however (easing bias)

It contains this sentence which was not there last month:

“the demand for some categories of consumer durables has picked up; housing prices have moved higher; there are early indications of a pick-up in dwelling construction; and savers are starting to shift portfolios towards assets offering higher expected returns”

Basically exactly what Ricardo wrote in this post.

Agreed, I just meant perhaps others expected it to be even more hawkish – ie no easing bias. I take comfort in Ricardo getting it spot on because it means the RBA has not lost the plot (which looked like a risk at certain times last year).

They kept the note on the exchange rate and demand for credit: “On the other hand, the exchange rate remains higher than might have been expected, given the observed decline in export prices, and the demand for credit is low, as some households and firms continue to seek lower debt levels”

Diffchecker (google for it) is a great online app for line by line comps.

Hey Rajat, yeah i didn’t see much change. Perhaps a small upgrade to non mining investment and more confidence in the resi pickup.

They could have done more. Market seems to have been positioned for a more dovish statement. Meltdown post rba.

Interesting – shows how much I know about what the market is thinking!

Question: in my mind there’s no issue: the CPI inflation will stay within the target band as RBA is forecasting and that would allow RBA to cut further if needed. But the big question IMO is mainly re asset prices, shares and housing: if we get another 5-10% in shares and housing growing at 5-10% p.a, would that stop the RBA from further easing no matter what else? What’s the maximum asset price appreciation the RBA is comfortable with. I have in mind the 2007-08 debacle. That could be the real rate-cut stopper.

As you know, i think wealth effects are a key part of the monetary transmission mechanism, so yep i think another 10% on asset prices would be a big deal. More so the housing than equity wealth effect, but both are key and very stimulatory — and a substitute for further RBA Cuts.

We still have the end of the boom to get through, so the next move will probably be down — but that could be 2014 if the capex outlook was true.

On the 25% jump in public capex… It was at the state/local corporation level. Any chance an asset was bought off the private sector? Not sure how this would be accounted for but would suspect would have to detract from private capex to avoid double counting.

Thought it also could have been a PPP being delivered but think this would probably show up as general gov capex.

Whatever the case it looks funky and think it is more accounting than genuine activity.

Yeah, looks odd. I would be very interested if you find out what it is. Please keep us posted, if you do. Thanks :)

I rarely write remarks, however i did a few searching and wound up here March RBA – watch the tone

| ricardian ambivalence. And I actually do have 2 questions for you if you tend not to mind.

Is it only me or does it give the impression like some

of these remarks come across like left by brain dead individuals?

:-P And, if you are posting at other online social sites,

I’d like to follow everything new you have to post. Would you list of every one of your shared pages like your twitter feed, Facebook page or linkedin profile?