The April RBA decision was another pause at 3% (last move -25bps to 3% in Dec’12).

This was well anticipated by both markets and economists — markets had it priced 96% by the 2.30pm announcement and none of the economists in the Reuters and Bloomberg surveys expected a cut.

The post-meeting statement contained the fewest substantial edits I’ve seen in almost two years — zero! I don’t see any at all.

With the statement a cut and paste job, its no surprise that the RBA left the easing bias in place. As I noted in the preview, the explicit easing bias was conditional on the inflation outlook, and it makes sense that they would wait to see the Q1 CPI print (late April) before moving on this front. Given that forecasting is very difficult it just does not make sense to move ahead of that information.

Picking through the detail it’s possible to identify a few tweaks. For the most part, the RBA sounds a little more confident that the non-mining sector is picking up — though the high AUD and falling commodity prices have their attention.

Here’s my paragraph-by-paragraph summary

Global Growth => The emphasis changed regarding Europe: it’s now in recession — rather than enjoying reduced financial strains.

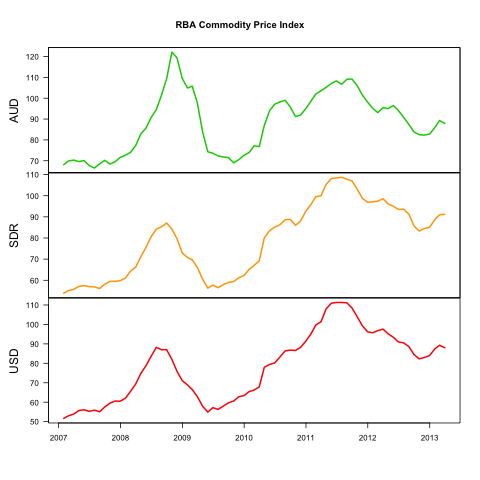

Commodity Prices ==> here the RBA has shown a pessimistic bias. They might have upgraded last month — but they didn’t. Given that they held despite price strength last month, they might have held despite weakness — but they didn’t. Here we got a small downgrade to ‘have declined somewhat recently, but are still at historically high levels’.

Financial markets ==> an upgrade to ‘very accommodative’. Here what’s notable is that Cyprus didn’t even rate a mention (how things have changed!).

Domestic demand ==> is there a difference between something that’s ‘approaching’ and ‘drawing close’? That’s what the mining boom’s end was doing, and is now doing … They repeated that as this happens there is scope for other areas of demand to strengthen.

Got it? The RBA wants these other areas that are currently gaining pace to get even stronger.

Green-shoots ==> There was a tiny upgrade to non-resource investment. A modest increase is now ‘likely to begin’ rather than there only being ‘some prospect of a modest increase’. They are also more sure of Dwelling investment: it now ‘is slowly increasing’ which is up from ‘appears to be slowly increasing’. This is an increase in confidence in their central case — not an upgrade.

Inflation ==> With no new inflation data, the inflation paragraph was mostly unchanged. The reference to labour market weakening was dropped following the odd jobs report (too hard to explain? reserving judgement? both?), and it now just says that ‘labour costs remain contained’. There is the same stuff about firms lifting efficiency and this keeping inflation low despite the FX appreciation waning.

Monetary conditions ==> a move in both directions. They are now more certain that their cuts are working, noting that ‘there are a number of indications that the substantial easing of monetary policy … is having an expansionary effect’; however they shook the stick at the exchange rate, noting that it had ‘risen recently’ and that it is higher than expected.

So policy still works, but FX is crimping their style a bit. Right now, it looks to me like asset prices are their main transmission channel, as they are not getting much traction from FX or credit growth.

Conclusion ==> cut and paste! It’s still prudent to leave their policy rate unchanged, and it’s still the case that the inflation outlook gives them scope to ease, should demand require a boost.

So what’s the medium term outlook?

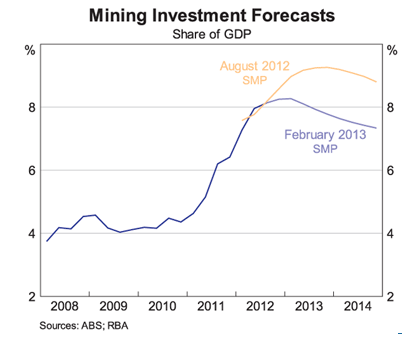

I still think the next move is a cut — probably in 2014. Right now, it seems like the RBA will hold policy at 3% waiting to see if the economy needs further policy support when the mining investment boom ends. When will it end? Who knows: my guess is next year.

The current lift in demand is desired so they won’t be freaking out, or talking about rate hikes. They want further strength as mining investment recedes. Right now, the RBA is simply getting the increase in non-mining sector activity they wanted when they were cutting rates in H2’12. The increase of house prices, consumer confidence and other leading variables are the desired and deliberate outcomes of their prior policy steps.

With the mining investment outlook a little brighter than they had expected when they were cutting in Q4’12, it’s possibly a little too much too soon, but inflation is low and there’s plenty of slack in the labour market, so that’s tolerable.

So the game plan for now is to hold at 3% and wait and see. If the AUD keeps going up, and commodity prices keep coming down, they’ll get a sooner end of the mining boom and have to re-start cutting. Similarly, if risk premia rise once again, and asset prices re-rate down, they may lose the wealth effect that’s boosting demand and have to cut again.

Going neutral is likely to prove challenging. I think that if they move to neutral bias that the AUD will challenge them by moving noticeably higher. Better to keep the easing bias while they wait and see about the end of the mining boom.

Sill, I could be wrong. Maybe mining investment will hold at 8% of GDP for ages and the non-mining sector’s acceleration will eventually produce too much inflation pressure.

Or maybe we’ll get mining boom III and mining investment will go even higher — which may mean that the economy needs both higher rates and a higher AUD to balance things out …

Maybe … my money remains on the horse named ‘bust’ — he’s still running the same race, it’s just a year or so later than i first expected.

Credit growth rate is not even close to what it used to be while mortgage rates at around record low already. Watch credit growth rate and TWI: these are the only two numbers that really matter. All the rest is consequential. Low credit growth + high TWI = low inflation = low rates (and house prices and share prices going no where from here).

Re-reading the statement, it explicitly confirms this, just before the end:

“There are a number of indications that the substantial easing of monetary policy during late 2011 and 2012 is having an expansionary effect on the economy. Further such effects can be expected to emerge over time. On the other hand, the exchange rate, which has risen recently, remains higher than might have been expected, given the observed decline in export prices. The demand for credit has also remained low thus far, as some households and firms continue to seek lower debt levels.”

Credit growth rate and TWI will dictate the cash rate.

And inflation and demand :)

No credit growth + high dollar = no inflation and tepid demand.

BTW, where are they seeing the recovery outside mining? Just released:

http://hia.com.au/media/~/media/Files/MediaMicrosite/Media%20Releases/New%20Home%20Sales%20Show%20Mixed%20Signals%20in%20February.ashx

Sorry new housing is just too expensive.

Let’s see tomorrow FEB retail sales and building approvals. The summer bounce looks weak so far.

FEB Retail sales VERY strong (including completely enumerated, but completely enumerated had one-off big months last year too). Combine that with higher consumer confidence and higher house prices in the summer… is this the start of something or just a one-off reaction to the big jump in share prices (which is kind of stalling now)?

Building approvals OK, huge jump in VALUE OF ALTERATIONS AND ADDITIONS TO RESIDENTIAL BUILDING.

NUMBER OF PRIVATE SECTOR HOUSES still almost at GFC low however.

no cuts and a horse named joye-boy is out in front in the 2013 race is my view

What’s his forecast on rates for 2013?