Today’s April RBA meeting is not of much interest for the decision itself. Futures markets imply a 9% probability of a cut today (and basically only one further cut this cycle).

Markets are, however, keenly anticipating this decision — for they are nervous about the possibility that the RBA will drop their easing bias.

The reason folks are thinking this far ahead is that the RBA spent only a small period on hold at the end of the prior two easing cycles. In these two cycles the period between the last rate cut and the first hike was around six months (in the 08/09 easing cycle the last cut was April 2009 and first hike October 2009; in the 01 cycle the last cut was Dec’01 and the first hike was May 2002).

I think this cycle is different. The RBA was easing rates at the end of 2012 as they were concerned that the end of the mining boom would depress demand. While the most recent Capex data suggests that mining investment will stabilise at a high level in the near term (somewhere between the two SOMP forecasts in the above chart) there’s little reason to think the mining investment will remain permanently elevated.

We are going back to 4% of GDP at some point … which means policy will keep waiting for the end of the boom. It’s also premature to call the end of the easing, as it’s likely that the economy will require additional policy support when the mining investment drop-off arrives.

Thus, all the talk of tightening seems premature.

This cycle seems more like the long easing cycle that began in 1996 — where the first hike didn’t come until 1999. In the 90s, the structure of the economy was changing in a dis-inflationary way (helped by enterprise bargaining — from which we have since taken a backwards step); the looming end of the mining boom is also likely to change the economy’s structure in a disinflationary way.

In any case, in both of these ‘quick reversal’ cycles, there were two obvious positives that are presently lacking: unlike in these cycles, the present prospects for residential and non-residential investment are not especially good.

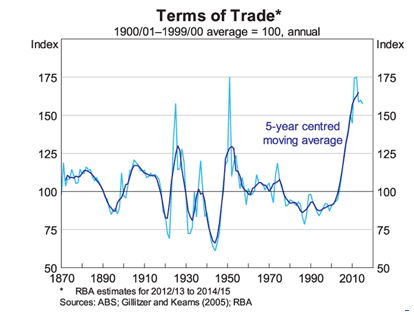

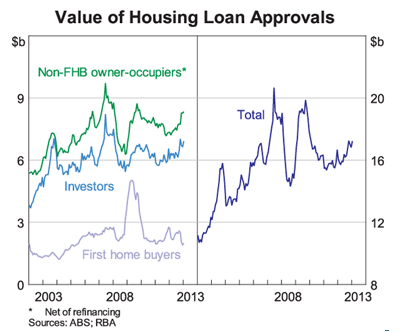

In 2002 and 2009 the terms of trade were rising and housing was firing due to a mix of government incentives and low(-ish) mortgage rates. We have neither just now. The prospects for mining investment are dimming, and despite some froth at the top end due to microeconomic reform (which has made it easier for wealthy foreigners to buy expensive properties) broader housing — as measured by housing finance activity — remains subdued.

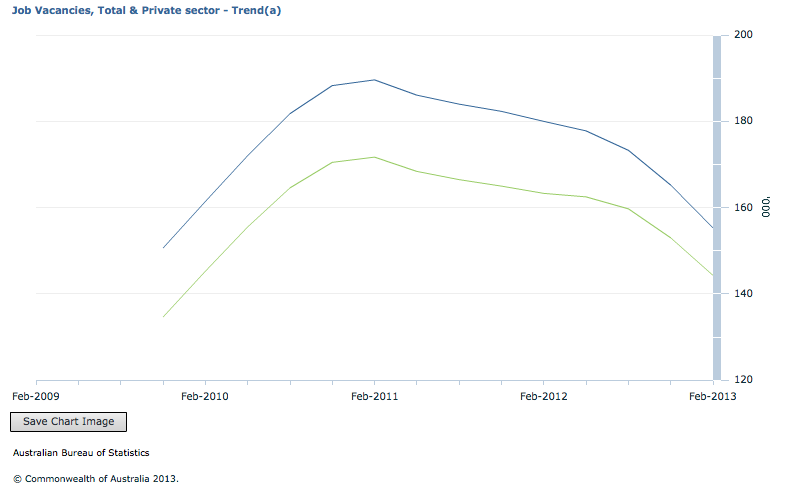

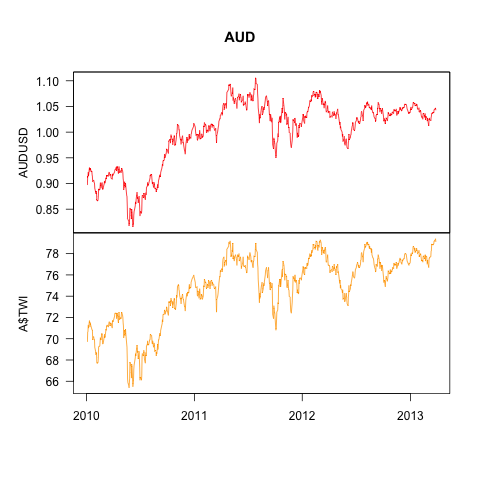

Reflecting this, I doubt that the RBA will drop their explicit easing bias this month. The high AUD (in TWI terms) and falling bulks prices mean that concerns about the end of the mining investment boom will be higher this month. Further, the drop in job vacancies has undercut the confidence one might have had in the labour market following the February ABS employment report.

What I expect from the post-meeting statement:

Global growth: unchanged at ‘a little below average’. The US has been better than might have been feared given the drag from higher taxes (see my note on US consumption). The EU is probably looking a little weaker, given weakness in the Feb PMIs and other timely indicators.

Commodity Prices: i was surprised they didn’t upgrade this last time; Iron Ore and Coal prices have fallen since, so they had the better judgement. They could again leave it unchanged if they please — as prices have run back down to early Q1 levels: they may downgrade.

Financial Markets: unchanged at ‘much improved’. Things are good, but setbacks remain a risk (even Europe wasn’t able to topple things this time via their handling of Cyprus).

Domestic demand: unchanged at ‘around trend over 2012’. We may see something about a below trend end to 2012. They can leave in the bit about green-shoots in consumption, investment and exports. They probably need to say something about the labour market — they’ll probably say that it wasn’t as good as the headlines suggested (my take on the Feb report here, and some more medium term stuff about slack here).

The case for a firmer labour market would have been stronger if vacancies hadn’t collapsed by 6% in the quarter to Feb’13.

Inflation: there has been no new information on inflation. They may tweak the bit about the labour market softening (for even if the Feb jobs report wasn’t 70k jobs per month strong, it painted a picture of a stable labour market which is better than they expected). However, given the drop in the official measure of vacancies, this can await more information. Given this, the outlook is pretty sure to remain ‘consistent with the target over the next one to two years’.

Monetary conditions: Here we get a test for those who claim the RBA has had a ‘tactical’ easing bias — aimed only at holding the currency down. Due to the weakening of the EUR and JPY, the TWI has been to fresh all time highs between meetings. This is despite easing commodity export prices. The interest rate sensitive sectors continue to show the ‘normal’ early signs — though the response is at the low end of the expected range.

Conclusion: the RBA holds rates at 3% and continue to say that the inflation outlook affords scope for further easing, should that be required to support demand.

The easing bias has been conditional on inflation — they ought to wait for more information about inflation before dropping it.

FWIW, I think you will be right on what the RBA says in its statement.

As for this cycle generally, I think we need further easing even if mining investment sticks at 8% GDP. The difference with previous cycles is not so much about absolute levels or magnitudes of various factors (mortgage rate, FHOG, etc). It’s about the RBA’s approach to communication of the expected path of policy. In 2008-9, the RBA cut hard and kept cutting even as the government announced stimulus measure after stimulus measure. They indicated that they wanted to see growth remaining strong, despite a high trailing headline CPI from high oil prices. This time, despite government rhetoric about cutting and surpluses and gloom from the retail and housing sectors, the RBA tells us we’ve never had it so good. That was their error and remains so. As I’ve commented here ad nauseam, if the RBA broadcasts to the market that it is comfortable with a particular state of affairs (ie 4% NGDP growth and weak employment growth), economic agents will respond accordingly – they’re not stupid! Yet some commentators continue to prattle on about how monetary policy is super-stimulatory and how rate rises will soon be needed. Policy is not super-stimulatory, it’s slightly more so than neutral and the minute future world growth expectations hiccup due to Cyprus or China or whatever, we go back to the doldrums. This is very disappointing behaviour by the RBA and if I were Joe Hockey, I would be seriously considering a move to NGDP targeting. Otherwise, the Coalition could face a similar situation as the UK Conservatives and risk being a one-term government. This might sound overblown, but tax revenues are growing well below trend and spending cuts alone are not going to generate a surplus or fund more goodies unless the RBA commits to offsetting fiscal policy appropriately.

It depends on if they are right to tell us the outlook is good. I agree that expectations are key, but if expectations are unreasonably low, then expected future returns will be also and this will depress activity. Lower rates will then be the remedy. The rba is heavily invested in this asian century stuff — they may be right, and keep our spirits up might be correct.

Still, i think the outlook is challenging.

Yeah, the easing bias will be there, same wording in the conclusion as last time. If not, shares prices will contract until next meeting and TWI will go even higher, that’s not what the RBA would want right now.

We discussed it here before: rate are peaking at lower highs in each cycle on their way to zero…. well, this time there will not be higher rates at all. At most, we will have the RBA dropping the easing bias at some point in the future and then a new easing cycle will start. THAT will be all of the rate increases we will have for this cycle, the temporary dropping of the easing bias.

With the US, Europe and Japan fighting disinflation at infinitum, Australia won’t be able to fight gravity for much longer.

I suspect you are right. If financial markets seize again, it could get away from them very quickly.

Just read this: according to the NAB, since the RBA last moved rates in Dec, TWI is up 3%. It equals at least 50bp of tightening under an appropriate ‘monetary conditions’ rule.

One graph says it all.

David Scutt : S&P/ASX 200 in USD terms is back at pre-GFC peak (same as the US S&P 500)

That’s the level of deflationary drag the high Aussie dollar has and will keep having on our economy.

I get the idea, but I don’t think your conclusion is right. In October 2007, AUD was trading at about 90 US cents. So XJO is not back to its pre-GFC peak, even in USD.

2007-04-05 to 2013-04-02 (6 year chart)

XJO : – 17%

http://www.google.com/finance?q=INDEXASX%3AXJO

iShares MSCI Australia Index Fund (ETF) (NYSEARCA:EWA) + 3.77%

http://www.google.com/finance?q=ewa

Not really the peak you are right, but just before.

Aussie dollar started appreciating and approaching parity already before the GFC.

EWA is more similar to XFL (S&P/ASX 50): http://www.google.com/finance?q=XFL

XFL that is – 12.36% vs. 3.77% of EWA over 6 years

Anyway, it gives the idea of the impact of the high AUD on local share valuations.

Pretty spot on Ricardo. Perhaps slightly more bullish than expected in parts, but also plenty of downside caveats.

Yeah, i think they are a little more confident about the handover than i am. Perhaps they judge that more of it is due to their policy steps than i do — i think they got a gift from financial markets.