My judgement about the very short-term RBA outlook comes down to a judgement about the state of the Australian housing market.

To put it plainly, I think that you can see the work of easy monetary policy in the Australian housing market — and that the RBA shares this view. So, with policy already clearly expansionary, the burden of proof for further easing is higher.

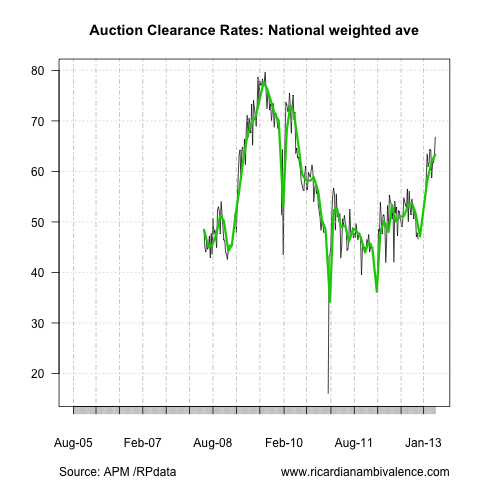

Happily for my theory, the Auction data supported my judgement last weekend, with the national clearance rate making a high for this year of ~67% (this may yet be revised, but it’s the latest data as of writing).

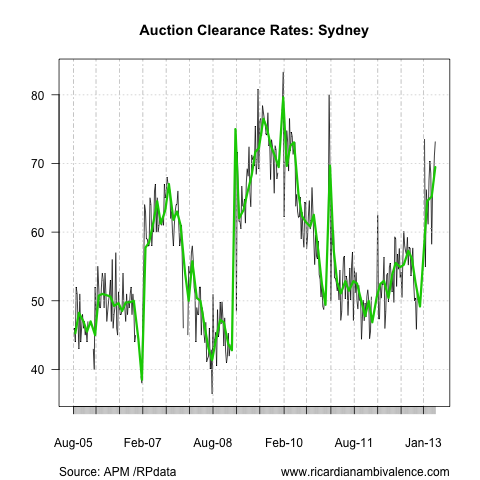

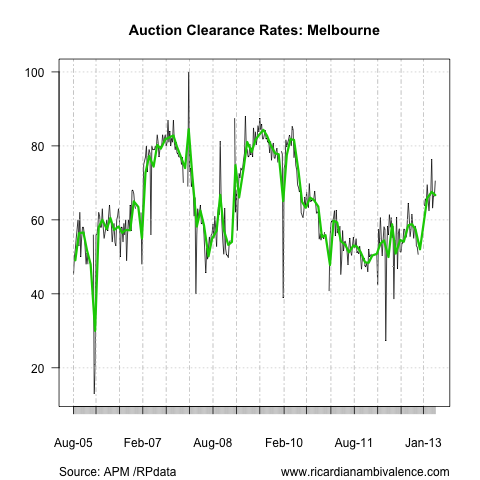

The reason it made the high is because this is the first weekend in which both Melbourne and Sydney clearances topped 70% at the same time — both have made it above 70% for some particular weekend this year, but not on the same weekend.

With these clearance rates, ongoing modest (single digit) capital price growth should be expected in the near term.

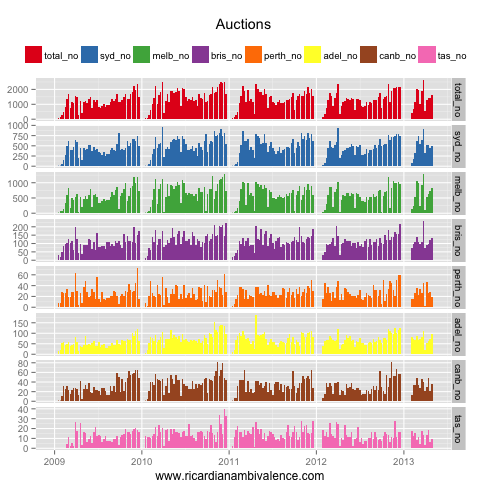

Another test of market tone is volume (probably because folks don’t like to sell at a loss, weak markets are characterised by low turnover) — and this has been firm of late.

Auction volumes nationwide were about 20% higher in April 2013 than 2012 — with Melbourne volumes +28%yoy (after +10%yoy in March) and Sydney volumes +15%yoy (after +25%yoy in March).

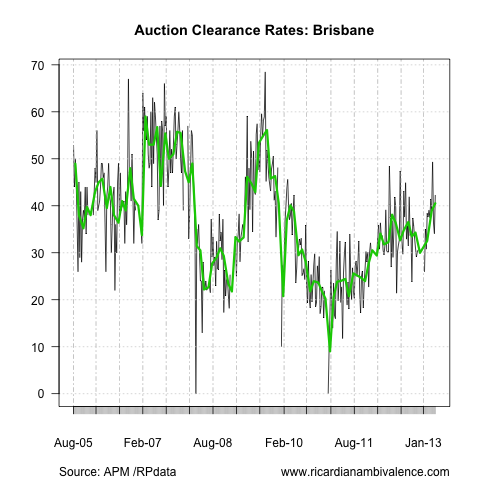

Even the depressed Brisbane housing market appears to be coming back, with clearance rates now ~40% (not fantastic, but it’s well up from the depressed levels seen in 2010-11).

Interestingly in April house prices were lower. The y/y increase is about the same as CPI.

I think the real surprise is how prices are NOT responding to rate cuts so far, for instance comparing to 2009. There are other factors at play this time. Auction volumes may be improving but overall transaction volumes are significantly down, see house finance data.

you should use RPDATA auction numbers published each Friday instead, they are much more reliable and with fewer unreported.

I don’t think that daily index is very reliable.

But it’s what the RBA uses? The monthly measure is just the daily index taken at the end of the month as far as I understood. It’s not seasonally adjusted so there’s a tendency to go higher in spring and lower in winter, so April lower is no “problem”, but the summer bounce had seasonality too. I am not saying housing is not in better shape compared to last year, I think a lot of activity last year was on hold because people wanted to see where rates were going, but housing is not a stopper for lowering rates IMO, should other indicators require it.

This is a great site for getting an idea of the current Melbourne house market situation, they are buyer advocates: http://marketnews.com.au/

You would not want to disagree with John Symond, would you???? :)

http://www.propertyobserver.com.au/news/rate-cuts-not-working-well-enough-aussie-john-symond/2013042860812

cheers

I am just not convinced that all the movements are signal — seems that there is a lot of noise in ere as well. It has had odd gyrations from month to month that i doubt reflect anything meaningful. I use it, but with caution.

I agree, there’s big movements month to month in the index that do not make much sense. I still do not understand how they treat data points that are coming in late, since there are no revisions. For instance the April number could be impacted by transactions that are coming in now for the summer. In general, auction results are the fresher data and the most positive data too (if you sell at auction usually the price is OK). Other data could come in via govt and takes longer I guess. Anyway, for me ABS housing finance even if delayed by a couple of months and RBA financial aggregates are a more important indicator.

I think they move the end point.

So if they didn’t get a bunch of expensive sales last week, and they came in this week, the expensive sales are added into the data they use to estimate the current price, but the old estimate of the current price is not revised — despite the fact that we now know it was flawed.

I would prefer an approach that simply aggregated the data as it becomes available, and revised the prior data if needs be.

So the index actually reflects the prices as the data is received, not when the sale actually happened? Is that it? So cities where the auction process is used and because of that data is more “fresh” more should be more real-time, e.g. Melbourne?

That is my understanding.

On a different note, last night I was reading a book called “Basic Economics”

http://www.amazon.com/Basic-Economics-Common-Sense-Economy/dp/0465002609

I would recommend this book to anyone who is not an economist but wants to learn the basic principles. One of the good points discussed was about all the activities that are not included in the GDP calculations just because money is not involved in the activity, such as home duties, garden vegetables, etc.

RA, if someone would want to read/learn about money creation, debt, central banks and the modern banking system, do you have a book to recommend? thanks

Blogging, stackoverflow … lots of the new media stuff is productivity enhancing and free so missed. Some is a drag too, i guess. Still i think we miss important stuff.

I learnt Mishkin at uni, and have read papers since. It is a patchy field, full of cranks. Working in finance has greatly helped my bs detector.

This sounds like bs, but interesting too

http://www.webofdebt.com/

what do you think?

The cover puts me off. Money used to be more private. If anything, modern central banks are more involved than ever just now. Debt is just how we trade future and present consumption. It is not an evil.

Also be careful about stocks and flows. Big enough stock and you have a problem as you have a finite life, but lower rates (which lowers flow repayments) can cover many sins.

Found this : http://mises.org/Books/mysteryofbanking.pdf

It’s free so I’ll give it a try !

This school is very clear thinking, but also a bit hard edged. They are cold shower types, like modern RBC but less maths. They are ‘austerians’ … Hayek’s folks.

I see they are part of the “Austrian School”. I like the idea that Austrian economics treat rising prices as a contingent phenomenon of an increase in the money supply, all rest being equal. It does not look like it’s happening in the US right now, but you would expect that in an environment with lots of slack due to unutilized resources. It’s quite peculiar how monetary policy in the US, even if extremely accommodating, is failing so far to meet the inflation targets. And also how, despite no inflation pressures, gold has appreciated considerably since 2008.

This is where Rajat chimes in and reminds us that low rates do not mean easy money.

What’s else can they do? 85bn per month and zero cash rate at infinitum not enough? Stocks at new high? It would have been better to prevent the whole thing, rather than trying to fix it? What are they going to do now with PCE core back to around 1% y/y. It looks to me like there’s a limit to what monetary policy can do. In a globalized world, deflationary / inflationary forces are huge and very difficult for central banks to control.

Agreed, it is hard to make inflation in the wake of a credit bubble. They could do more!

The BoJ’s current experiment will settle the question – does this stuff actually work?

RA, more data on transaction volumes, especially look at the last graph:

http://www.macrobusiness.com.au/2013/05/state-territory-stamp-duty-receipts-tank/

Thanks. V useful

Shame it is so late …