The RBA meets today to talk about the 13th rate cut since 2001. Of the twelve prior rate cuts, this is the closest call that I can remember (I was more confident – or just feeling lucky! – prior to the 50bps cut in May 2012 and the pause at 4.25% in Feb 2012).

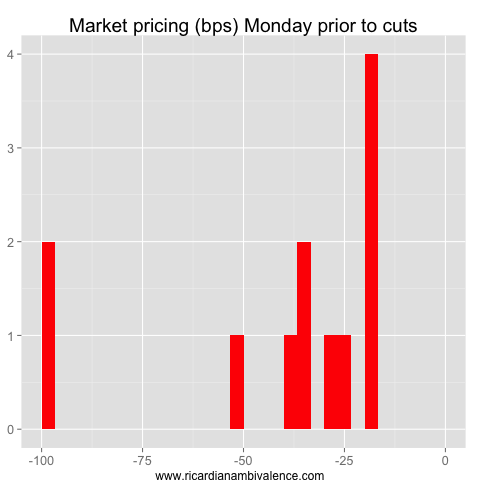

Market pricing remains about 50/50, which would make this the first time the RBA has cut with so little priced (since the IBs started trading in 2003). Since 2001, the RBA has eased rates only when the market had priced in about a 70% chance of a cut. I think that this reflects the degree of inertia in the RBA’s decision-making (that is, they like to be deliberate about how they do things so they tend to move when it’s obvious).

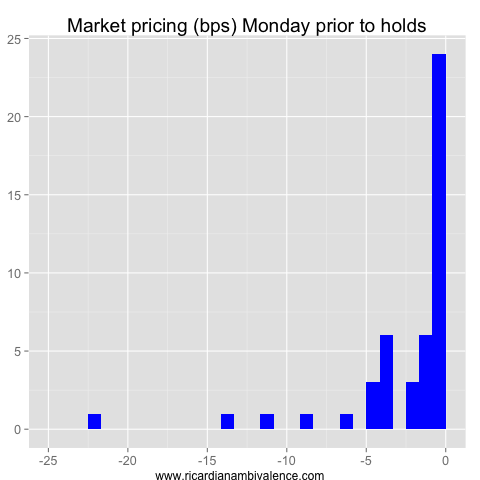

By contrast, there have been 47 meetings where the RBA has held their rate steady despite the market having priced in some possibility of a rate cut.

The biggest surprise was the March 2009 RBA meeting, where the market had 22.5bps priced and the RBA held steady at 3.25%. Other big disappointments were Feb 2012 (-14bps priced) and Nov 2012 (-11bps priced — which I bombed).

So what can we take from this? I think it’s that the market may be a little biased as a predictor of rate cuts. If this is the case, the true probability of a cut today is probably a little less than 50%. My subjective judgement is ~33%.

The main reason is that Q1 demand has been better than the RBA expected (see this post). My read of the statement has been that the easing bias is about the need to prop up demand — and demand has not been softer than the RBA’s forecasts.

This makes me think a hold is the more likely outcome today.

Sure, demand isn’t great either (especially the nominal stuff), but the RBA’s forecasts were already for weak growth, and the data simply hasn’t been worse than they expected. Thus, i think a rate cut would seem a little incoherent.

They might justify it in terms of low inflation, or flagging global demand, but i think it’s more likely they point to those things when setting up for a possible June cut. After all, the housing market is looking pretty good, financial market conditions continue to ease (Spain and Italy are ~100bps tighter, equities are +4%), and the data might just turn up.

In terms of market being biased: I think that will depend on how it prices other decisions: rate hikes, steadies.

Agreed there is more to it than 1d out ahead of cuts – and in any case, there are only 12 cuts in my sample so any conclusion is fragile.

How much of the May 2012 50bp cut was priced in at the time?

About 30bps … Yeah, that is a chink in the argument.

But my thrust is that the default option is to hold, and that the burden of proof for a move is high. So the (smaller) point is that is is only when it is obvious that the RBA moves — i hope!

you are talking about the real economy as opposed to the nominal economy

oops! but expected. Trend broken?

“Employment contracted at a steeper rate with the sub-indexregistering 29.8 in April, a decline of 9.4 points from the previousmonth.

This represented the weakest reading (and therefore the steepest rate of decline) in the 7½ years since the commencement of the survey.”

http://www.businessspectator.com.au/news/2013/5/7/economy/businesses-report-darkening-outlook

“A key measure of Australia’s capital spending outlook has fallen to its lowest level in more than three years, pointing to a darkening outlook amongst Australian businesses.”

Maybe they should move today….. C’mon RBA you can knock the AUD out of its trading range finally! LOL

Yuck … It is volatile and a good month in may will push the trend back up, but this is uncomfortable.

I would summarize the whole economy as businesses being unable to control costs (and especially salaries) but also being unable to convert those increasing costs into higher sales. One of the two will have to give.

IMO, this is the results of a decade structural domestic / salary inflation. One wonders how / if a lower dollar can help… yes it will help exporters (what’s left), but for importers and distributors the margins squeeze will be even more significant. A lower dollar will push up inflation and make the RBA unable to deliver further cuts. It’s going to be a tricky balancing act.

Wages need to decline — but how to deliver that? One way is via a long period of slow inflation.

Can Australia withstand a long period of slow inflation, after being addicted to high levels of debt for a decade or more? There’s lots of (private) debt out there that must be repaid. Debt that was taken because prices always go up. A lower dollar *could* be a way to make wages decline and outstanding debt easier to repay, it would bring Australia “back to the old normal”. But we can’t have it both ways. Both high AUD and high wages simply is not sustainable.

And now that I think about it, it is exactly that very high private level of debt which “commands / requires” higher salaries (growing salaries are required to repay the debt) and at the same time puts pressure on sales and the whole economy, as people use the extra money to repay debt faster, not to get into more debt. We are at “debt peak”. Combine this with high AUD and the resulting low nominal GDP is obvious.

CBA has real and Nominal GDP being about the same this fiscal year.

I would have thought real wag reductions were a natural corrollary of a deregulated labour market

I am glad history is wrong, maybe they are now looking at the nominal economy/

By the way I am examining the important issues of the day.

Castle of course.

Isn’t Kate Beckett smoking hot!

Whoa! 25 cut.

Ugh

Ouch for you Ricardo!

Glad to see it happen though.

Yeah, i was in the difficult position of thinking they would not cut when i would have voted for one. I would have cash at 2.5% by now. It is annoying to have a ‘right’ theme (RBA is not done cutting, economy will need more support) and then to totally flub the timing. Oh well …

I think ‘totally flub’ is pretty harsh! Much better to have had a coherent framework and a reasonably consistent position than to shift around as market sentiment changes. The Kouk has the former while CJ has the latter, but neither has both. Read a note from MQG who predicted a 2% cash rate. Hopefully if the RBA cuts again soon, that won’t be required.

Strange, they cut because imported inflation is too low. But I thought that was a desirable thing to have, the upside of the “mining boom”? Then they say “Growth of labour costs has moderated slightly over recent quarters while productivity growth appears to be improving. This should help to lessen increases in prices for non-tradables.” appears, should…. what the????

I think they realize they are not getting any traction in new housing construction and they will not get it for a while. There’s a huge amount of unsold stock out there. And it’s too expensive! This cut shows that they are now 100% confident that inflation will be contained and employment stay soft. I also think they are pretty confident we are not about to enter a new credit boom anytime soon! They must have relied on insider info too, for instance I am sure they know more about upcoming capex intentions than the public knows.

I would think they can get a good chunk of the capex survey from a few phone calls.

Yep. Poor C.Joye, he keeps getting it wrong since this easing started. But at one point it will stop, and he will be right finally!

Good analysis by Shane Oliver I thought. http://t.co/IsBXVLTgUl

Yeah, some interesting comparisons to previous cycles. He has a typo though – the early noughties easing cycle started in Feb 2001, not Feb 2002.