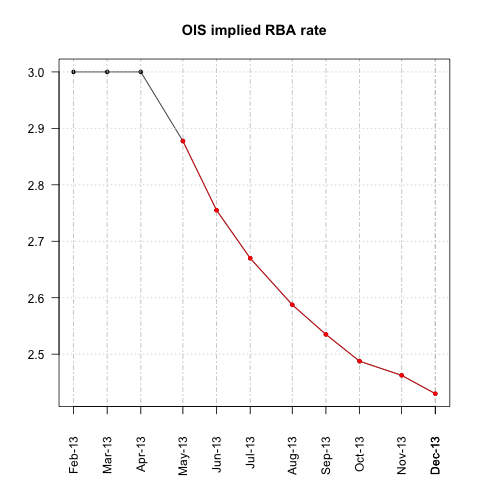

The RBA meets for their regular monthly meeting tomorrow (on Tuesday 7 May), and the market is split evenly on the outcome. A bare majority of economists expect rates to stay on hold, and market pricing is exactly 50/50 for May, with a cut priced as a certainty by June. Current pricing suggests that their cash rate will fall below 2.5% some time in Q4’13.

I’ve been of the view that the RBA’s easing bias is very real, and that they’ll resume cutting as the mining boom fades — but i’m not of the view that they’ll ease rates at their May meeting.

Why not? I do not think a rate cut makes sense in the context of the data and what the RBA has had to say about it.

I just do not see strong evidence of the downturn that seems to have struck my peers. My guess is that a big part of my problem is that i didn’t see the strength in the February employment report (see these posts: 1, 2, 3) — and therefore i didn’t get all over-heated when the March report showed things coming back a little (see this post).

To put it simply, the labour market is unlikely to have ever been Feb-good, and is also unlikely to be March-bad. It’s just soft.

Anyhow, it doesn’t matter what i think, what matters is what the RBA thinks. The most recent update we have to that thinking is the concluding paragraph of the April post-meeting statement, which went as follows (my emphasis):

The Board’s view is that with inflation likely to be consistent with the target, and with growth likely to be a little below trend over the coming year, an accommodative stance of monetary policy is appropriate. The inflation outlook, as assessed at present, would afford scope to ease policy further, should that be necessary to support demand. At today’s meeting, the Board judged that it was prudent to leave the cash rate unchanged. The Board will continue to assess the outlook and adjust policy as needed to foster sustainable growth in demand and inflation outcomes consistent with the target over time.

My read of this is that the RBA will cut if they think that demand needs a boost. So what’s going on with demand? And more importantly, how’s demand tracking relative to the RBA’s forecasts (for surely the formula above was meant to indicate that they’d ease if demand was weaker than they expected).

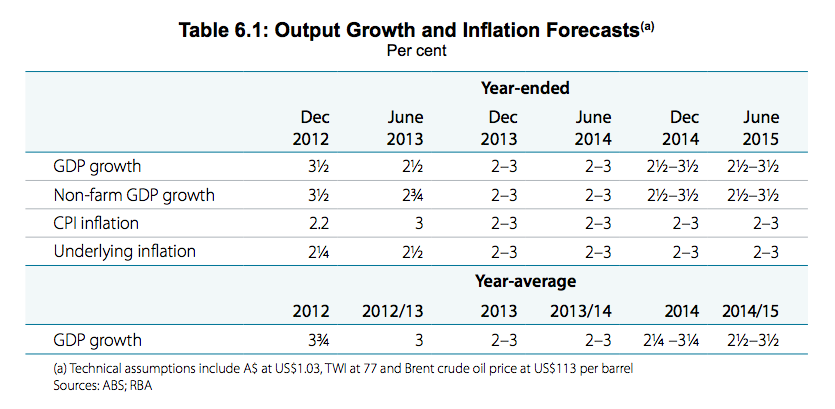

The RBA’s most recent demand forecast can be found in chapter six of their Q1’13 SOMP. This reports a forecast for real GDP of 2.5% for the year to June, and 2.75% for non-farm GDP.

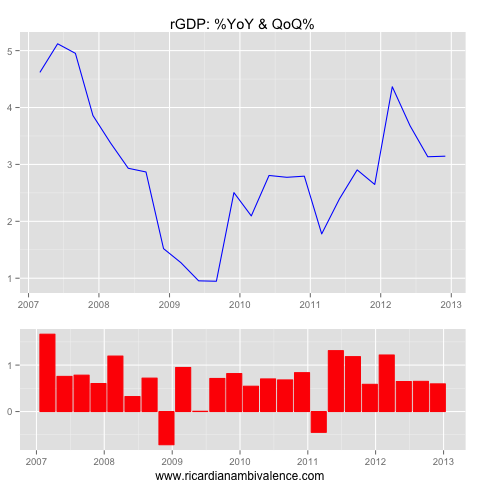

We do not have a forecast for Q1’13 GDP, but looking closely at this chart (from Box E, which shows forecast errors) you can see that their Q1’13 estimate is very close to the 2.5%y/y that they are also expecting for Q2’13. To hit this they need 0.6%q/q in Q1’13, and 0.5%q/q in Q2’13.

Remembering that the Q1 SOMP was published a month before the Q4’12 GDP data, we can peg the last observation (Q3’12 GDP) at 3.1%y/y. We have since learned the Q4’12 GDP was also ~3.1%y/y, which was a little lower than the RBA had expected.

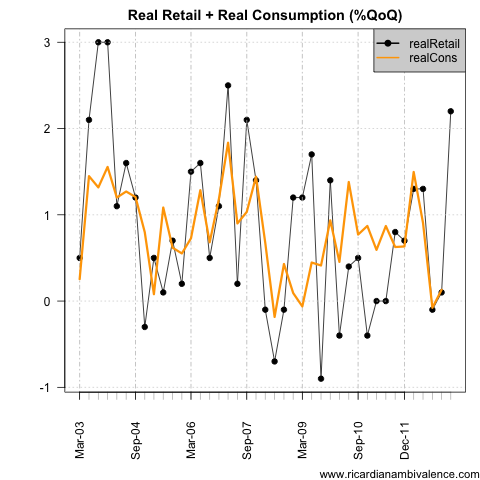

If this was the most recent data we had, then you’d think the RBA might cut — but it’s not all we have. We now have a lot of information about Q1’13 GDP. In particular, we have Q1 real retail sales — which were a massive +2.2%qoq. In quarters when there is very strong real sales growth we tend to also see strong consumption growth.

Total Consumption is around 70% of the economy (household consumption is ~55% of the economy) so it’s pretty hard to get a very weak Q1 GDP report when Q1 real retail sales was 2.2%q/q. It looks like net exports will add about 50bps to GDP, and given the strength of retail sales growth a consumption contribution of ~80bps is likely.

Given this, it’s more likely that the RBA will be upgrading their near term GDP forecast in the Q2 SOMP (which is released this Friday).

With that in mind, i think a rate cut would look a little incoherent. Sure, they could still cut, and emphasise the signs of weakness in the monthly data and global data — but that data is volatile and coming months will very possibly reverse all that weakness.

Alternately, they could just say that inflation is too low and cut … as for certain they will have cut their inflation forecast.

On balance, i think the RBA will stick with their prior test – which means they will ask “is demand weaker than we expected”? The answer to this question appears to be certainly not up to Q1’13, and maybe not in the Q2’13 data. Given this, they should wait for more information before easing further.

Great post! The upcoming *real GDP* numbers with weakness in nominal will be confusing their plans. But even if they do not cut, will they release a more dovish statement?

I think that is the key part. Commodities have come down since the last meeting and AUD has not moved. The soft labor report was released after their last meeting. Every industry index has been weakening considerably after the Jan/Feb jump. I think they could wait for more data but they already know what they’ll be getting. If I cut the prices of the product I am selling in order to get a sale, that does not necessarily reflect a strong economy. It actually destroys future demand. Anecdotal, but I heard of many small business that are now focused exclusively on cutting costs even the successful ones. In this instance I agree with Rajat that nominal GDP and inflation is the key, and that is also impacting govt revenues. I agree with market pricing, as things stand today, no cut in May and then a cut in June after more data will only confirm more cuts are needed. I think the capex numbers will be surprisingly weak.

Yep i think the statement will be more dovish. I think it’ll set up for a cut in june unless things turn up.

I think the post makes a lot of sense, especially in light of what the RBA has said, and you are probably right that they will not cut given the recent flow of data. But I don’t think the RBA is looking at things correctly when they place so much emphasis on (real) demand. Monetary policy is only good for targeting nominal variables and they have been low/weak. Real GDP may be growing at something close to trend, but I always believed that a mining boom should mean that our potential (real) growth is stronger than normal, at least temporarily. We don’t really know what potential real growth is at the moment. But as you say, we do know that the labour market has been soft. To my mind, that suggests the path of least regret is another cut or two. As I’ve said before, I think they are too focused on the absolute level of rates and the absolute level of house prices.

I agree with you – my focus has been on the nominal weakness for a few qtrs now and it’s for that reason that i’ve been sure the easing cycle is not over. However, as you point out, the RBA has not been emphasising this part of the economy (at least not up to now).

It is going to hurt doubly if i bomb this one, as i have had the right ideas … Hope i don’t have the wrong timing.