Following on from yesterday’s (somewhat contentious) post, I am going to compare Australia with eight other nations that are rated AAA-stable by S&P (I used this list). Once again, I use the 2012 data from the IMF’s fiscal monitor — because it is comparable across nations (and no one can forecast!).

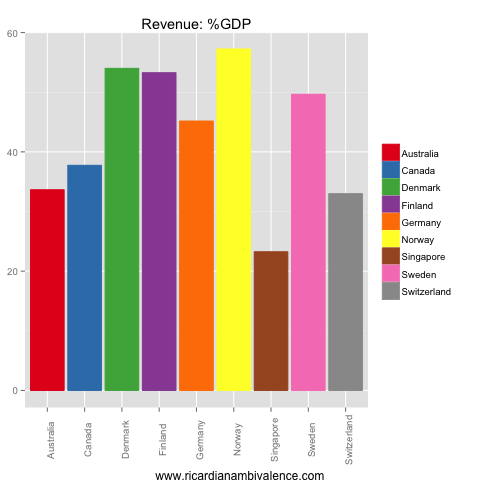

The first chart is of revenue: here Australia clocks up a low-ish 33.6% of GDP. The city-state of Singapore is lower, but they really are different. Switzerland is really the only comparable nation with similarly low revenue (~33% of GDP). I think the low tax effort of Australian Governments is a strength for the rating — there is scope to raise taxes without damaging growth too much.

On the expenditure side, Australia is similarly low among peers, at 36.6% of GDP. Again, Singapore is a different case due to it being a city-state. Switzerland at 32.7% is the only comparable nation that has lower spending as a share of GDP.

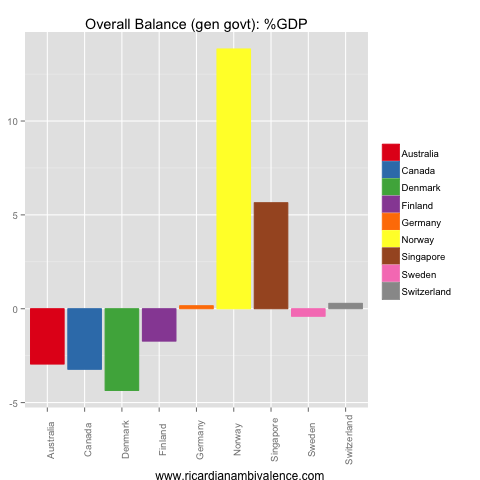

Spending more than you tax means you have an operating deficit. Australia is mid-ranked, with a deficit of ~2.9% of GDP. Norway and Singapore are special cases (oil and city-state), though here Germany (0.2%), Switzerland (0.3%), and Sweden (-0.4%) show a much cleaner pair of heels. I think Australia’s weak fiscal position at this point in the cycle in an embarrassment — and both sides of politics are to blame.

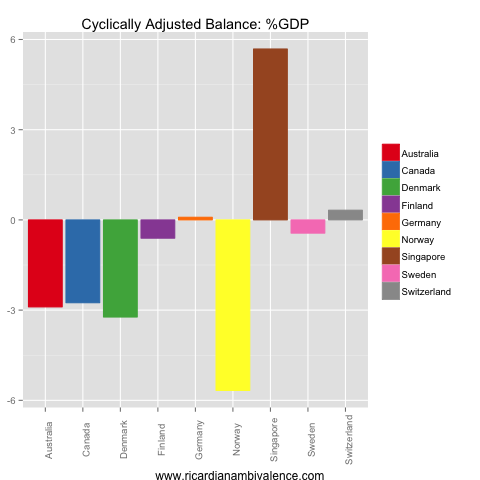

Much of the criticism in comments yesterday amounted to saying that one must take account of the economic cycle — well the IMF have looked after that for us as well with their cyclically adjusted data. Australia’s cyclically adjusted balance is around the bottom of the pack, with a deficit of -2.9% of GDP (Norway gets to be an outlier due to the way the oil money works). The weakest of my AAA club is Denmark with a cyclically adjusted deficit of -3.2% of GDP in 2012.

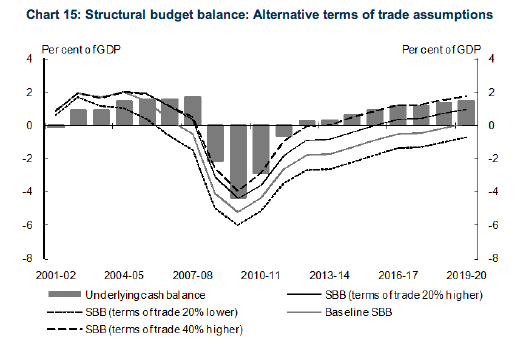

Note the IMF’s cyclical adjustment does not include the terms of trade, so if you think the high level of Australia’s terms of trade upswing is temporary, the structural budget deficit is larger (see this Australian Treasury note for more detail). After taking into account the terms of trade, I would say that Australia’s structural position is the worst of the AAA-club.

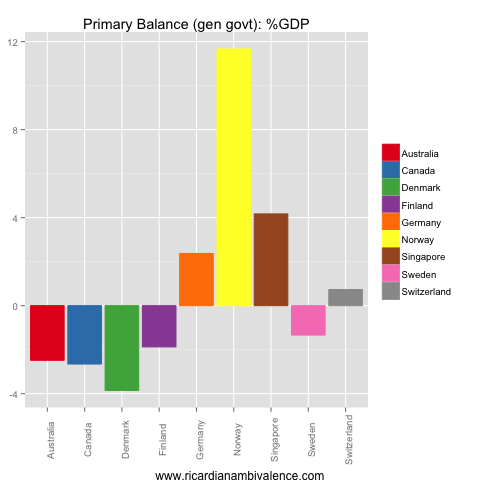

In the long run, what matters for debt sustainability is the primary balance (debt after interest costs). Here, due to small debt (and despite relatively high interest rates) Australia doesn’t get much benefit — the primary balance is only 40bps smaller, at 2.5% of GDP. Canada (-2.7%) and Denmark (-3.9%) are worse; Finland (-1.9%) and Sweden (-1.3%) are better; Switzerland (+0.7%) and Germany (+2.4%) are much better — and Singapore (4.2%) and Norway (11.7%) are special cases.

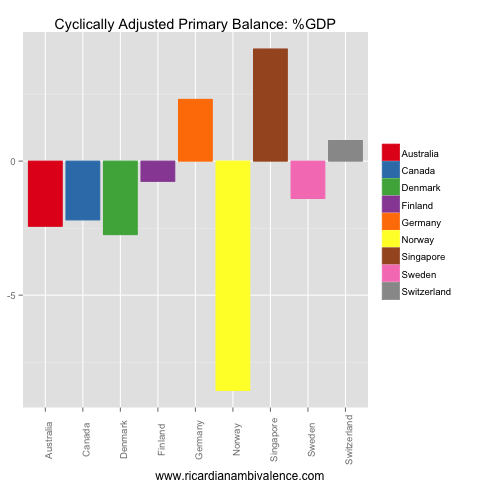

After adjusting for the economic cycle (but not the possibility that high commodity prices are cyclical), Australia’s cyclically adjusted primary balance clocks in at -2.4% of GDP. Only Denmark is worse (-2.7%); Canada (-2.2%), Finland (-0.8%) and Sweden (-1.4%) are comparable nations that are doing a little better; Switzerland (+0.8%) and Germany (+2.3%) are doing much better — and Singapore (4.2%) and Norway (-8.6%) are special cases.

I just want to make a final point about the terms of trade — Treasury were publicly warning about this from 2010 (see this edition of their economic roundup). They almost certainly were cyclically high, and they almost certainly will decline. This is a possibility for which we ought to have been prepared.

Indeed, that’s basically what’s happening just now. The recent decline in commodity export prices is a large part of the reason that Australia’s nominal GDP growth is so weak — which is currently depressing tax receipts. You can see in the above chart that the lower you assume the equilibrium level of the terms of trade to be, the larger the structural deficit.

You can also date the fiscal rot — it started in 2004-05 …

What about private debt levels in Australia? Australia actually can’t raise taxes as private households are too indebited. What will happen is that private debt will slowly (hopefully) be converted into public debt in the next 5 years (with consequential efficiency losses). This will happen because consumers will keep saving and govt will keep running deficits. The ratings are rubbish , Ireland was rated triple A until few months before the whole country was taken down by its banks.

Read exclusively RA’s reaction to Castle’s last episode last night here!

:)

In terms of CAB, I am more interested in what the public sector does to growth i.e is it adding to it or is it detracting from it.

When this is at odds with the CAB I go to the latter .

A look at recent history would show the CAB heavily distorted both here and in Europe!!

I am not so Ricardian that i think the government cannot add to short run demand by buying more stuff, but i do not think that the government can boost growth over any long period of time (outside some insurance type policies, like security, defence, and maybe health and education).

Why exactly should Singapore be treated differently? I guess the treatment of Central Provident Fund contributions and payouts is a bit of an issue, but I’m not sure being a city-state is a reason to put them in a separate category. Australia chooses to subsidise the living standards of people in rural and regional areas – that’s a policy decision that could be unwound. If agricultural and mining activities produce so much value-add, they should pay their own way in relation to transport, communications, health and educational services as well.

It would take a lot to unwind horizontal fiscal equalisation in Australia, but i suppose it might be done. But it seems unlikely — in a way it is what glues a fiscal union together. Sure, we might unwind it, but it would come with costs of its own. Singapore does not face this trade off, so it is a special case.

But how is that any different from individual European countries arguing that their high levels of social spending are the glue that holds their country together? Singapore also faces domestic inequality, in fact, their incomes are more unequal than ours.

It isn’t that different, so yep there’s tension in my views here. Services are fairly equal in singapore, even if income is not.

Are you saying you want a tighter fiscal poicy?

If so wouldn’t that just make nominal GDP weaker?

I want one for the last decade. And yes, as the problem is structural, they must continue to gradually tighten. This isn’t cyclical — unless you think the recent decline in the terms of trade is cyclical.

But over the long run, does anyone think that government spending = growth?

While I agree that too much government spending leads to waste, inefficiencies and malinvestment, there’s bigger issues IMO than government spending = growth or government spending != growth.

I was reflecting a few days ago on the Australian economic growth. Yes, the growth rate is and has been good for many years. But that’s because Australia is a relatively new, growing country. Population is growing. 100 years ago there was not much in Australia. Cities are growing. Can’t compare Australia with an old European country where everything is already there. Wealth has been built for centuries there. Population is getting older. It’s not just a question of public debt or private debt, they are just in a completely different situation. In a sense I think that their ever increasing public debt in Europe have been used to hide the intrinsic economic weakness, but I do not think it would be a much different situation if the debt was private instead. I just think they have lost competitiveness in a global world that has delivered cheap labor and free trade. They have survived during the credit boom, and have run out of options now. Take away mining from Australia, we are left with having to build more, but otherwise can we consider ourselves competitive now? So we’ll go down the same path, public debt is low, so we will increase it and we will try delaying the necessary reforms that are deemed to painful, as much as possible. I guess it’s human nature.

In a word it’s called Decadence. Once you “arrive”, you try to maintain the status quo,

I liked your comments about Castle better!!!

Are you saying you want tighter fiscal policy now?

Are you wanting the budget to take 1 % point ff GDP growth for example.

Put me down as a sceptic but when we get back to normal growth perhaps some of the structural problems would have dissippated!

Yes, i want and expect ongoing gradual fiscal adjustment. The deficit is mostly structural.

BUT do you want TIGHTER fiscal policy?

Yes. Not a lot tighter, but a bit tighter.

so you want tighter fiscal policy when nominal GDP is slowing.

That would mean a higher overall deficit as Treasury advised Swan.

not sensible policy but Castle asked Beckett to marry him so I do not care!!

Pfft … That is ridiculous, it implies a fiscal multiplier that exceeds 3x.

Australia’s total govt situation is as follows:

gdp = 100

Rev = 33

Spending = 36

Deficit = 3

Say they cut spending by 3 in an effort to get back to surplus. For there to be no improvement, the fiscal multiplier would have to be > 3x, as GDP would have to fall below 90.9 for revenue (at 33%) to fall more than 3bn short of the new lower spending level.

We are not at the ZLB so that is basically impossible.

err this budget will detract 3/4 of a % point from growth.

You want more ( which means anything up to 1%) which would entail nominal growth of maybe less than 3% when monetary policy is doing little and the $A seems determined to stay higher than it should.

I really do not know where you get your multipliers from as I didn’t even imply that.

you have been deflected because of Castle me thinks

You claimed that more tightening would lead to a larger deficit – the multipliers drop out of the math required to make that statement true.

yes for the reasons outlined above. The economy weakens.

If the detract say 1% from GDP where is that going to be offset given the $A and housing only moderate

Say you cut by 3ppts of gdp, and gdp drops by 4.5ppts (which is the sort of fiscal multiplier you would get in your dreams if you are away from the ZLB), then leaving tax at 33%of gdp, the deficit closes by 150bps.

In your 100bps case, you need to have gdp drop by 3ppts to get no deficit improvement on net. Not going to happen.

I like this post much better than the first one. Very interesting!

The addition of the CAPB charts, or the peer group made the difference?

Both. Its just a more relevant comparison now. The CAPB charts give some context and the peer group provides a useful discussion point. The things you’ve discussed as a result really touch on some really important issues ie terms of trade and where the australian economy sits in relation to other comparable countries.

Excellent post!

Hi,

We are from FocusEconomics, and we find your articles very interesting. Just wanted to let you know that we have shared your post in our latest Blog Mash-Up of the Week. I’ve included the link below for you to check it out*. One of our in-house economists has selected your article and commented on it would therefore be more than happy to be in touch with you. Please drop us a note if interested. Keep up the good work!

Cheers

*http://focuseconomics.wordpress.com/2013/05/17/2354/

Sure, happy to keep in touch. Thanks for your support. Email is ricardianambivalence@gmail.com