A key reason for the AUD60bn increase in deficits in the 2013-14 budget (relative to the 2012-13 MYEFO) was the nominal GDP downgrade (see here for more on the 2013-14 budget).

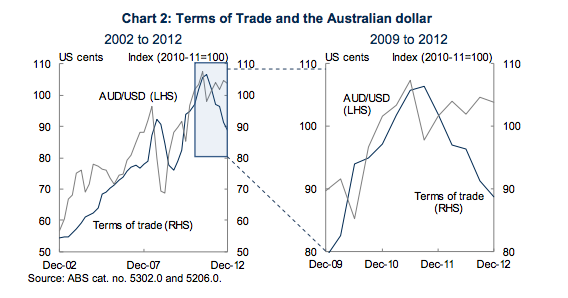

This nominal weakness is mostly due to the predictable impact of a decline in the terms of trade, which has partly been made worse by the fact that the AUD has remained higher than the historical camaraderie with the terms of trade suggested.

Given that the terms of trade are a key driver of budget outcomes, I figure that it ought to be a prime candidate for ‘prudent planning’ (the idea that you try to be a bit pessimistic, to protect against the downside).

That’s not what i see when i look at the Treasury assumptions:

The terms of trade are expected to decline by ¾ of a per cent in 2013-14 and 1¾ per cent in 2014-15, as increases in global supply, led by Australia, place downward pressure on some key non-rural commodity prices.

and for the medium term:

After 2014-15, the terms of trade are projected to decline by a total of 20 per cent over a 15-year period, settling around their 2005-06 level.

The 2005-06 level … so things ease to mid-boom levels by 2030?

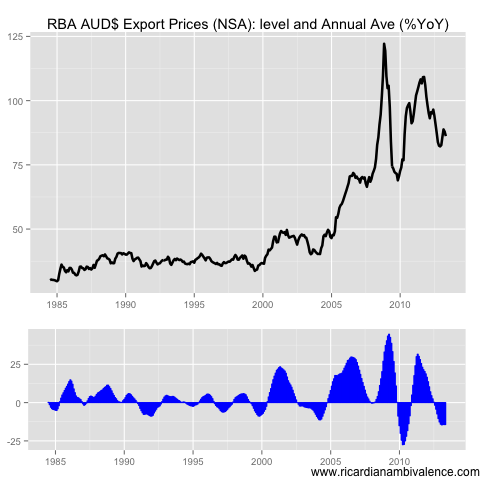

To make things clearer, I’ve added the short and long-term Treasury assumptions to the actual terms of trade to the below chart (along with the annual average YoY % change).

I note two things: first, that after booms the terms of trade typically move pretty quickly back to mid 50s (the average up to 2002 was 54, and the full sample average is 62); second, that this assumes that the terms of trade settle around the pre-mining boom peak of ~71.

Of course, most of this is movement is due to the spike in commodity prices (our import prices don’t move much). Export prices didn’t move much for 15yrs, and then tripled, and this boosted our terms of trade .

Most researchers believed prior to this episode that the relative price of commodities would remain in a long term down-trend. They may yet be correct, and they may not — the key to managing this uncertainty is prudent planning. A good start would have been actually saving the prior boom, rather than spending it (a mis-deed for which both sides of politics share blame).

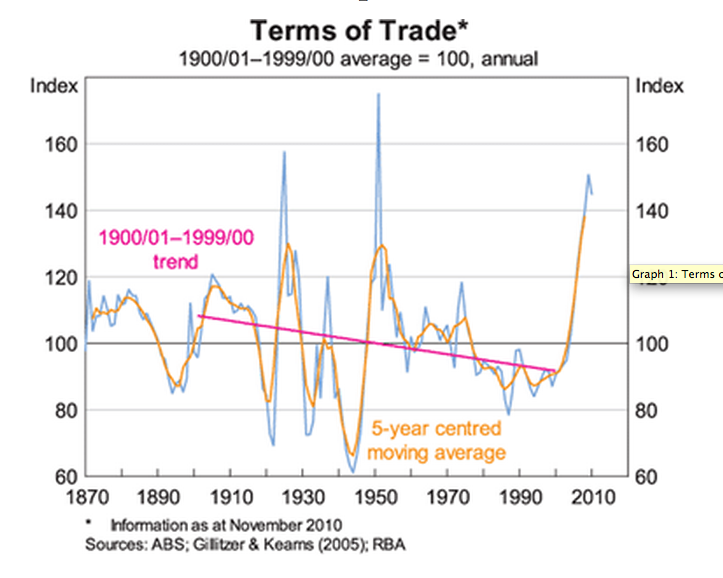

The RBA has done the definitive long-term work on the terms of trade, and they find (consistent with most researchers) that commodity prices were in a long-term relative price downtrend prior to the recent boom, and that prior price spikes have both corrected sharply and overshot on the downside to well below average levels.

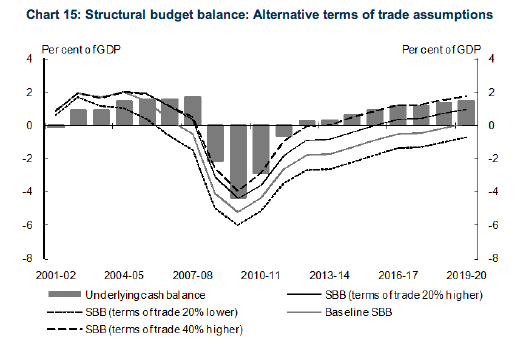

As Treasury have explained, the lower the terms of trade settles the greater the proportion of the budget deficit that is structural — which means that it’s not going to ‘correct to surplus’ as the economy recovers.

This is why I think that ongoing fiscal tightening is required, despite the fact that the nominal economy is weak — I fear that the terms of trade will do what they always do, and go back to average via an over-shoot to the downside. If that’s the case, we have a deep structural deficit, and are in midst of a structural slump.

The economy is merely soft just now, it’s not dire — there is scope for modest further tightening. It will protect against the downside risk of being caught penniless if the worst happens, and the economy needs firm fiscal support.

Quite scary really. But I believe another good reason for Hockey to broach NGDP targeting with the RBA quick smart. Even an announcement of a change in target would help stabilise expectations and potentially forestall QE if the worst comes to pass.

I’m not sure the previous Coalition government should have ‘saved’ more. Perhaps they should have not increased FTB and cut taxes by more instead, but leaving a big piggy bank for your successor to spend doesn’t seem very prudent, either politically or economically.

so the answer to a contractionary effect of the TOT falling more than predicted is to have greater contractionary policy here.

Are you doing an Ollie Rehn impression?

If it is structural, there is no choice. Best to do it slowly. Even Keynes was only in favour of counter-cyclical fiscal expansion.

of course there is a choice, you do it when nominal GDP gets back to normal levels.

mind you we do find out then if the structural problems are as bad then as well.

It assists growth then. It curbs growth now.

non mining GDP is barely 1%.

Keynes was only in favour of countercyclical fiscal policy when monetary policy didn’t work i.e a liquidity trap.

Despite my fervent disagreement this and others will be in the ATTs on Friday.

Very fair minded of you. Thanks. Keep up the contribution.

“Keynes was only in favour of countercyclical fiscal policy when monetary policy didn’t work i.e a liquidity trap.”

Then I presume he would have (wisely) disagreed with the Rudd-Henry stimulus.

The Rudd-Henry stimulus was completely reckless and over the top. They obviously were not spending their own money.

– It’s structural and there is nothing that can be done to reverse. If you cut more, the economy goes into a tail spin and your deficit increases anyway as revenues go down. If you do not cut, or keep the same pattern, deficit simply increases because it’s a structural deficit. Very similar to Europe, only starting from a better position, so our interest repayments, for now, are luckily much lower and we can still afford a primary deficit. Soon, we will have to account for repayments too, which will make the debt even more structural.

– The only thing that could prevent us from going down the same path of larger and larger govt debt, like basically every other developed economy, would be a mining boom part 3! But it’s crystal clear that we are now fully dependent on commodity prices, which are extremely hard to predict. It’s more likely that the term of trade comes down rather than goes up, but it would not be politically wise to deliver a depressing budget that forecasts deficits up to 2020 and more.

– On commodities, let’s not forget we have huge new capacity coming online starting from end 2013, that could pressure the prices lower. AUD will stay high, definitely vs EURO and YEN, maybe a bit lower with USD if US economy really picks up. But not much. Overall my money is on significantly lower ToT compared to budget base case.

Hard to argue with that. Short of a new mining boom or some other as yet unforseen productive revenue raising measure, we’re well on the way to emulating Europe. We’re not there yet, but we’re galloping towards it hoping that Plan A (mining) will somehow save us before we get there. Rather dispiriting really.

The fiscal multiplier would have to be greater than 3x for it to be true that cuts are self-defeating.

Can you imagine the panic that cuts (or tax increases) would create in a population that is already fully geared to the max? Are you forgetting the private debt that must be repaid at the same time? Families on > 100K that consider themselves as “struggling” and need family support? Already the fact that tax bracket are not moving with inflation will weight. And what would you cut then? Which taxes would you increase?

I am not saying that I would not like to have the budget balanced. I would. But that would mean making sacrifices now, impact on GDP growth, higher unemployment, possibly a recession. All in the short term for long term benefits. Yes, it would be a better choice in the longer term, but the temptation to have future generations pay for your current privileges is too big. I am very curious to see what the opposition will do when they are elected.

I doubt it. monetary policy was impaired.

Banks can’t lend money if they cannot get finds.

Credit markets froze!

Maybe initially, in Oct-Nov 2008. But auction clearance rates by the start of March 2009 were already >60%, so buyers must have been getting money from somewhere.

After RA’s Castle contribution how could he be ever left out?

Rajat there was a clear discrepancy between first home buyers and investors.

Ask yourself why

Yes, FHBs got a subsidy. But presumably they still had to borrow sizable sums of money in order to buy. So finance must have been available by early 2009. Ergo, they the government could have ditched at least the larger, second part of the stimulus.

LVRs for this cohort were very high. Banks raised the money thanks to govt guarantees.

I would even put the requirement of a balanced budget in the constitution. If you want to implement countercyclical fiscal policy, you first save a surplus and then you can deploy it as needed. Not the other way around.

Deficits are too much of a temptation for any governments, they are bills left for future generations to pay, future generations who can’t yet vote obviously.

SSEc, a balanced budget merely exacerbates the business cycle. Both the boom and recession are made worse.

nottrampis, you can run surpluses (if needed) but no deficits – ever. Once you have a surplus saved, then you can then use that surplus during the lows of the business cycles. Deficits are just bills left for future generations to pay. Europe is the result of the policies you are promoting: young people do not have a job and older people are retiring on their fat pensions and living up to 100 years old with free health care provided for them. Everybody knew this situation was sot sustainable, already since the ’90, but no govt ever cared, it was too dangerous politically. That’s why it must be put into the constitution.

I am also against bb- amendments. Also, they are typically signals that you cannot control yourself, like lots of rights in constitutions!

Yep, that’s exactly it, govt cannot control themselves. Spending money that is not yours and borrowing from the future is too much of a temptation.

really why did Ireland and Spain have surpluses and Italy a primary surplus then!

Spain had a better fiscal record than Germany!

Except they didn’t … Come on, no one ever thought that spain was a better credit than Germany. Show me the time spanish 10yr paper traded sub-Germany?

nottrampis, is Australia at the highs or the lows of the business cycle?

have a look at the fiscal record and debt levels of Spain and Germany!

SSEC we are at neither. We do have weak nominal GDP growth.

At these levels no-one can get get a balanced budget here. you allow the automatic stabilisers to do their job ( and also monetary policy)!

ah, yes, the NGDP excuse… forgot about that one…. but apparently our economy has grown 13% since the GFC … but still not the right time to balance expenses… but we will, really, trust us. we will

a small doubt… are we maybe spending more than what we can afford to?

With respect, i know them well.

so we have another person who wants lower growth.

Trying to get a balanced budget will make the economy weaker. you can only change the structural part of the budget. This has the strongest effect on the economy.

however it is the cyclical part of the budget which is the greater and that gets worse if you attempt to hack into the Structural part at the wrong time.

Europe anyone?

problem is: it’s never the right time. Europe? yes, we are following the same path of money wasting. But actually i think we would be better off wIth 2 trillion of debt, why limit ourself? lets splash out, just think how many hospitals we could build with that. it’s the USSR model. we could hire anyone that needs a job in the public sector. it’s quite simple isn’t it?

That’s right. There’s never going to be a ‘right’ time. If Australia can’t tighten its belt with the terms of trade at record levels, public debt still reasonably low and low unemployment, when are we going to be able to? You’d have to say never. The only real issue I see is the very high private debt levels, which as Europe has shown, can very quickly become public debt when the government invokes the various explicit and implicit bank guarantees. We’re only a crisis away from public debt at well over 100% of GDP. We may as well get started on the tough stuff now while we still can. If we don’t do it now, we will end up like Europe. It’s just a matter of time.