The proximate release of the Australian and New Zealand Budgets has prompted some comparisons between the two (see this odd news story).

To an extent, these comparisons are fair — both nations are small open economies that have been subject to basically the same shocks over the last few years. The exchange rates between the two is typically stable, reflecting the fact that the circumstances of the two do not vary over-much.

There are, however, a few differences worth noting: Australia had a mining boom, and NZ had a lot of bad luck. NZ first had an intense mini-financial crisis, when their small non-bank finance sector lost access to securitization based funding; next Christchurch (a major city) fell down following a series of severe earthquakes.

Perhaps that stored up some good luck for their successful rugby world cup campaign (they were certainly due) …

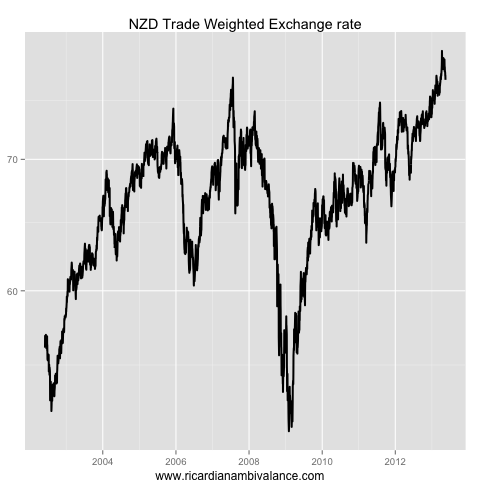

So onto the comparison: both nations have struggled with a very strong currency — you can see in the above chart that the NZD Trade Weighted Index recently made a new cycle high (though lower inflation has made the appreciation less painful — see this post for more).

As a result of the painfully high currency, RBNZ Gov Wheeler recently confirmed that the RBNZ had intervened in NZD FX market. Also, the RBNZ is looking at macro-prudential policies to slow the inflow of capital into the housing market: the RBNZ believes these would both reduce NZD appreciation pressures (see the above chart), and allow them to cut their target interest rate.

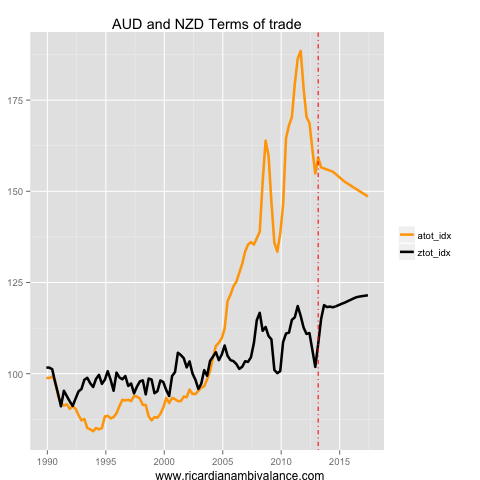

As both economies are small and open, their terms of trade are a key input to both economic and fiscal outcomes. Reflecting this, both Australian and NZ budgets include forecasts for their terms of trade (see here for more on the AUD terms of trade) — the chart below shows the history and budget forecasts (both indices are rebased so the full year average for 1989 = 100)

The thing that ought to jump out is that the Australian Treasury expects an ongoing decline in the terms of trade (not fast enough in my view), and that the NZ treasury expects the recent firm recovery of their terms of trade to both continue, and to take them to an all time high.

Naturally, I object to the NZ Treasury’s assumption: it’s imprudent to forecast this stuff — i would prefer a ‘back to average’ assumption in all cases.

The ratio of these two terms of trade give a sense of what has occurred over the past decade or so. Starting is about 2004, the ratio of Australia’s terms of trade to NZ’s terms of trade began to surge (this was also the year the Australian fiscal rot started).

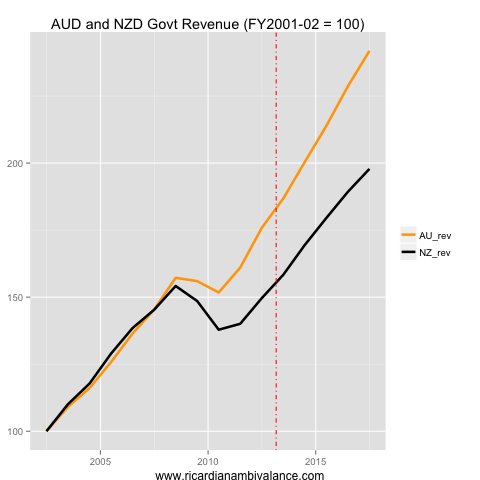

With that surging terms of trade came a surge in government revenue — this was particularly the case following the 2008 financial crisis, where-after the ratio surged to an all time high as ‘stimulus’ favoured hard commodities over soft commodities.

Partly because of this Australia continued to grow — but there was also a combination of good luck and good management. NZ, by contrast, had a heavy recession.

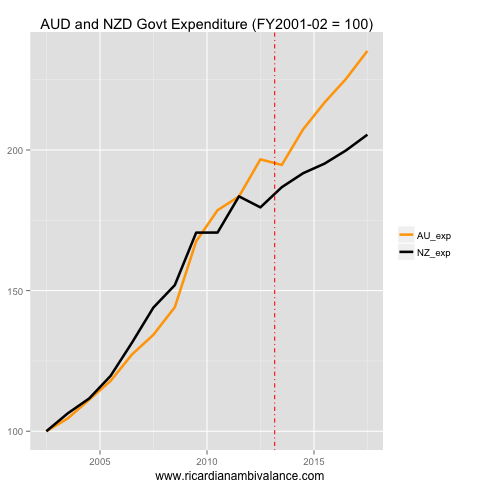

The great shame of all of this is that the Australian boom was (mostly) wasted — we allowed spending to rise along with our income. Even following the tight budget of 2012-13, Australian Government spending markedly outpaces NZ Government spending.

To those that say we must not tighten policy, as it would damage growth, i direct them to the example of NZ — there was a necessary fiscal adjustment, through which they lowered their trend pace of government spending. I was hopeful that’s what we would get something similar in the 2013-14 budget, following the reasonably sound 2012-13 budget — however spending just bounces back to the prior trend.

Yeah great strategy higher unemployment and lower growth.

You should remember in OZ expected revenues were much higher thus overall fiscal policy much tougher!

Never mind it is still in and you gain a new adjective.

I think we have a very different view about fiscal multipliers :)

No not really.

The thing I love about this blog is there can be a civilised discussion between people who sometimes disagree!

That is ‘our’ standard. I have deleted only a few comments, but that seems to have been enough to keep it nice.

The NZ Budget promised the part-privatisation of Meridian Energy (NZ$3.25 bn) and spending some (NZ$1.5 bn) of the proceeds. I assume the government spending figures above include the spending part? It just seems a bit odd that the growth in spending looks quite slow over the next year despite that cash splash.

It should do — i used the headline balances.

I think I know why you are confused.

You are believing I am saying the economy will go into recession whereas all i am saying is you wil have lower growth.

That is very cochrane of you !!

I wish i were as good as Cochrane!

well he doesn’t understand a simple accounting identity!!

I never buy into those characterisations – these ‘rockstar economists’ would have aced every course. You don’t get to be a professor at Chicago if you are a dunce.

really!

Ricardo why do you think the government has ownership of what is essentially bad advice from Treasury. Just looking at MarkTheGraphs most recent post (its good he’s back) and a few of yours and it seems to me that the ‘unexpected’ fall in revenues is simply based on unrealistic projections that were never going to stand up. If the Treasury had used the revenue projections of the 09 budget it would have been spot on and I suspect we would be having a very different conversation now.

For me the Treasury has provided some seriously bad advice over the past 5 years but the question is why? Is it just incompetence or have they become so political that they are no longer able to provide good advice because they are preoccupied with providing a suit of credibility for their political masters.

I believe that the budget is a political document. There is so much judgement required to make forecasts, and politics enters via those judgements.

But the judgements were so wrong it borders on the ridiculous. In fact if you use the ’09 forecasts as a guide the fall in revenue is make believe. I just find it astounding that even after the dodgy forecasts are shown to be wrong the credibility of those that have produced the original forecasts isn’t questioned.

Yes it might be political influence but surely the economists at the Dept of Treasury need to be held to account for such professional incompetence. I’m not sure how many other professionals could get it so wrong and still have credibility let alone keep their job.

Forecasting is tough – but that 12% revenue assumption for 12-13 did seem unusual.

I suppose what will happen though is that we will get an overly negative assessment of the budget position when there is a change of government. This will mean a re-assessment of revenue and expenditure forecasts that will reveal the renowned post-change in govt budget black hole announcement…so predictable and sad.

I’m very disappointed in Treasury. They seem to be, more so than ever, just a political spin tool of the govt of the day. They lack any credibility in my eyes, just economists prostituting themselves for their political masters.

Without seeking to defend Treasury – I agree, they seem to have become increasingly political in recent years – I’m not sure how many forecasters would have predicted 3% NGDP growth this year. I don’t think the RBA did.

Plug for you from Chris Berg in The Sunday Age!:

Not sure which post he’s referring to – Ricardo, if you were aware of this, perhaps remind us (and new readers)?

This is the post here: https://ricardianambivalence.com/2012/05/11/stimulus-update/