Yesterday’s Q1 GDP report showed some worrying signs for the domestic economy: in particular, it showed that the domestic economy has not grown at all in the prior three quarters.

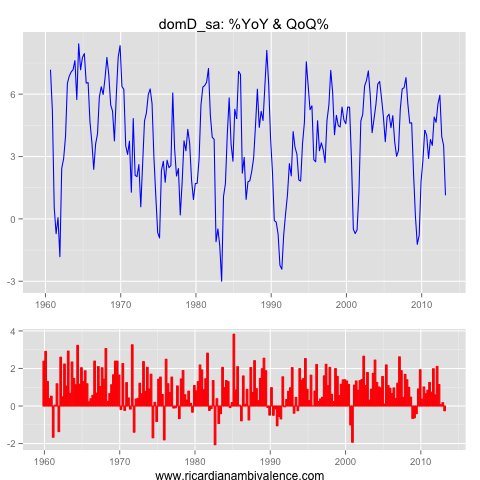

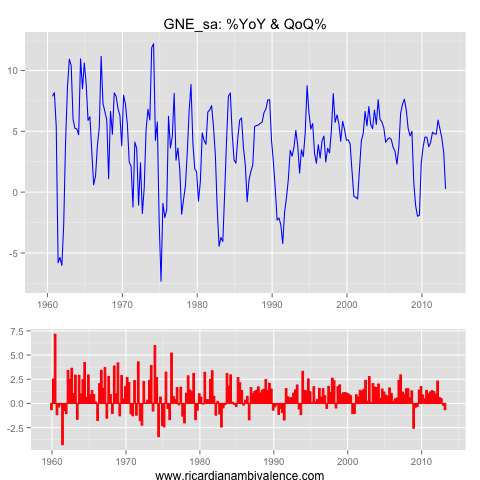

Domestic demand (C + I + G, excluding inventories) is flat since Q2’12, and GNE (Domestic demand plus inventories) is -0.3% lower over three quarters.

In Q1’13, domestic demand contracted by 0.25%q/q (after +0.2% in Q4’12) and GNE fell by 0.7%q/q (following a 0.2%q/q decline in Q4’12).

Both situations are uncommon — and have typically only been seen in and around periods where the economy is contracting (yes, in a recession!).

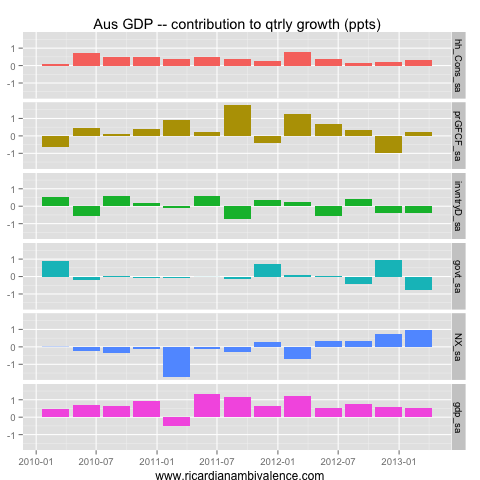

Looking at the contributions of the various sectors, it’s clear why the headline GDP data is not more alarming: net exports have been making an unusually large contribution to growth. As a result, broad measures of activity that include the external sector are showing okay growth.

This net-export strength is likely to be sustained — but can we avoid a sharp increase in the unemployment rate? Only if the RBA is agressive (and they really ought to be — starting in July).

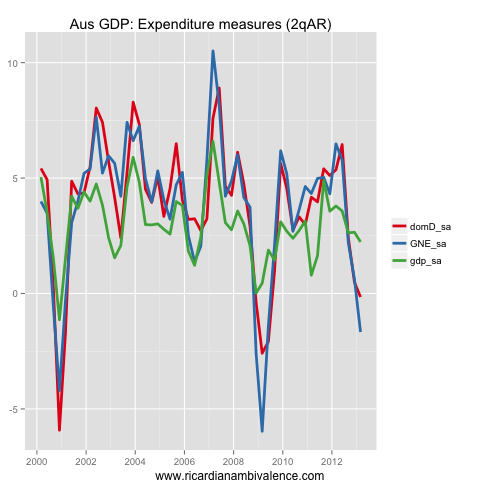

The 2q AR rates of growth put the situation into clear context — over the prior two quarters, the domestic economy has been weaker than at any time outside of recession.

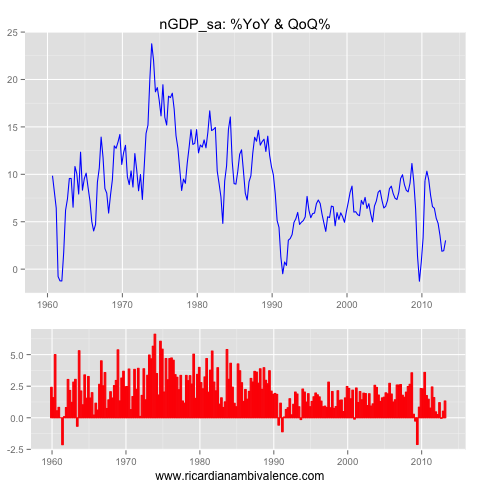

Finally (because I know you nominal-GDP junkies out there want to know) n-gdp picked up in Q1’13 (+1.3%q/q, after +0.5%q/q in Q4’12), though growth in n-gdp remains at recessionary levels.

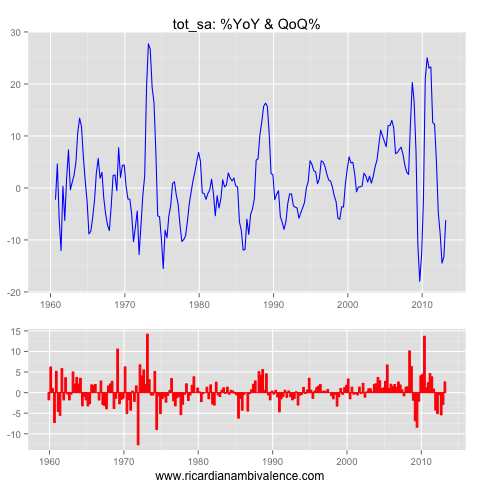

More-over, the improvement was due to a pickup up in the terms of trade (which had been trashed over the prior five quarters). With the terms of trade up ~2.6% in Q1’13, they are now down ~16% over the prior six quarters.

They had been down a record-breaking 19% over the prior five quarters — and have since resumed their decline.

Those looking for more ought to check the (awesome) GDP charts at Mark the Graph — his State by State splits are a worthwhile addition to any analysis.

Are you forecasting a July cut after yesterday’s GDP number? How does the GDP outcome compare with previous RBA expectations? thanks

be clearer after jobs next week, but yes i think July is now more probable than not. Regarding RBA gdp forecasts, they need 0.6%q/q in Q2 to hit their 2.5%y/y forecast, but i think the composition is less inflationary — as it’s basically all from NX and none from domestic demand sources.

perhaps the non-farm GDP forecast is more relevant — they need 0.75%q/q in Q2 to hit their 2.75%y/y non-farm GDP target. I think this needs to be cut to 2.5%y/y … and when the RBA cuts their gdp forecast they normally cut the cash rate.

All this money companies will be making from mining exports, which will boost GDP in the next few years, where will it go? Yes, taxes will be good, but how much of it is foreign profits and will leave Australia as dividends / share prices? How is that calculated in the GDP (I have no idea)? thanks

it will be a net income outflow for the most part, as their profits will go to foreign equity holders.

thanks, how does the ABS quantify that, where do they get their data on how this money moves, shares ownership and dividends distributions? Do you know?

it is all in the current account release — Q1’13 was published on Tuesday … too late for trading off, but it can give you an idea about trends.

OK – thanks

I have linked this to my major reason why the ALP will lose the election article as they are related.

It is of course first class

Thanks for the informative post. Now we need some action!

Our conversation about the RBA’s options once rbacor hits zero is looking a little more relevant today.

Just closed one third of my long USD position!

While I’m very skeptical of the GDP figures because they are just as useful as forecasts until the real data is incorporated, I was wondering, if this story is true and Australia is heading down the road of recession (which I highly doubt), how will this impact on Joe and Tony’s razor gang on government spending?

I don’t really have a political affiliation as I think both sides are made up by boneheads that exaggerate their importance and if this is true and oz is heading for a recession a change in government couldn’t come at a worse time. Whenever there is change there is incredible increase in mistakes and waste. Hang on everyone we are in for a bumpy ride.

It might be ambiguous it is RA’s analysis that is fist class not my hypthoesis

I believe that recessions are almost always caused by monetary policy failures. Unfortunately, while most of our central bank chiefs understand this, many of their colleagues do not. They have just done enough so far in Australia and the US to stay out of recession despite some moderate fiscal tightening. My concern is that they don’t do enough, recession follows and ‘austerity’ gets the blame. That could set sensible fiscal policy back a generation. Don’t the chiefs see this risk?

ahh, i think that monetary policy is fairly systematic and not too often the cause of shocks (i have adopted Chris Sims’ view).

I suppose what I meant was that recessions are caused by central bank failures to respond to shocks appropriately – that is, to keep their target nominal variable on target. How often do we see recessions (being persistent declines in real output) where nominal variables are on target? Too harsh a test? Perhaps. But I think all major central banks have been warned enough (and their chiefs certainly seem aware) that they need to be if anything easier than they are at the moment.

i agree with that — i think the volatility in markets reflects the uncertainty they have created by looking to change back to a ‘more hawkish’ rule. they ought to stick with their new policies until inflation is higher.

so yes, they see the ris — they are cutting because of it and will continue to do so.

“AUD/USD (Australian dollar/U.S. dollar) has now lost 10.6 percent in the last 40 trading sessions. In equity land that would be a correction, in FX that is a massacre,” Chris Weston, chief market strategist at trading firm IG markets.