The June employment report has nicely set up the RBA to cut rates at their August meeting, so long as the Q2 CPI report is around (or below) their forecast of ~0.65%q/q. Given that global CPI pressures were very weak in Q2 this seems very likely.

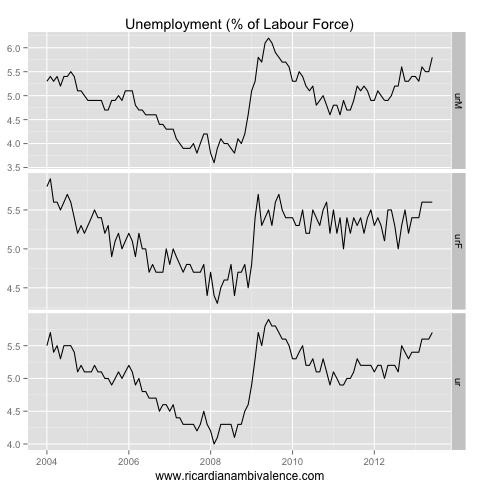

The report itself was fairly unsurprising — but it’s important as it confirms that the uptrend in the unemployment rate continues. This month, the seasonally adjusted estimate rose 18bps to 5.73%. I normally eschew second decimal accuracy with this report as it’s mostly noise, however ~20bps is around the threshold where we can be sure the unemployment rate has increased (the 95% range on the change is 0bps to +40bps).

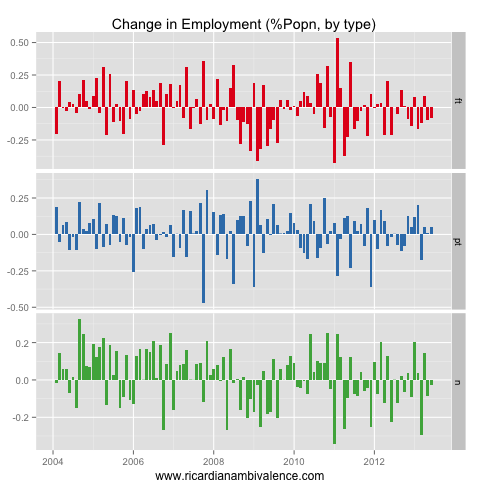

Those who want to put a gloss on the report might emphasise the employment numbers (though it’s not really what the report is designed to measure): overall employment rose 10.3k, thanks to a 14.8k increase in part-time employment offsetting a 4.4k drop in full-time employment.

The part-time / full-time movement from month to month is mostly noise. The big picture remains a slow uptrend in total employment, which is too slow to stop the unemployment rate from rising.

If we re-express the above chart to take out the impact of population growth (so we look at the change at the proportion of the population in either class of work) you can see that FT work is not keeping up with population growth; part-time jobs are growing at a similar pace to the population, leading to a slow decrease in the proportion of the population in work.

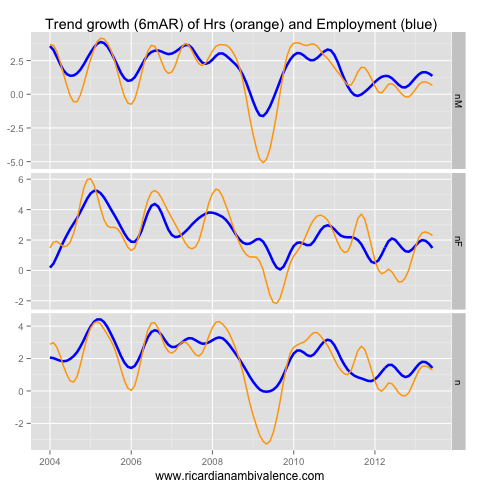

If anything, trends suggest labour market weakness is increasing, following a period where labour market weakness was ebbing (which I guess means there is no long-term trend … it’s just sideways at too weak). Both employment and hours worked trends are turning down again.

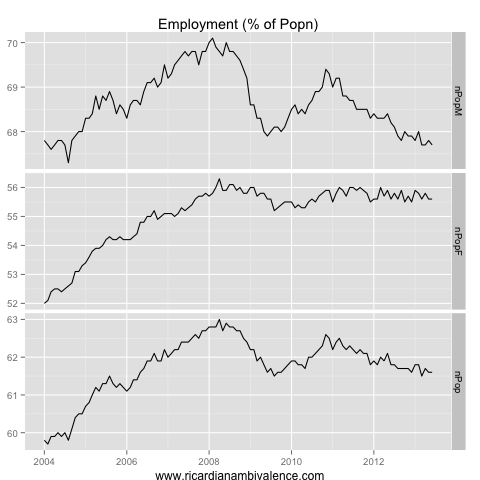

There’s not much change to employment to population measures: male n-pop is around the cycle low, and below the GFC low. I am getting a bit more open-minded about the possibility that structural change is depressing participation rates — which means that looking at the n-pop rate to gauge spare capacity may be misleading, though it’s too low just now for that to really matter.

Again, here the big picture is of widening spare capacity in the labour market. Given this increase in spare capacity, and a low Q2 CPI report, my guess is that the RBA board will judge that the inflation outlook does accord scope for further easing (assuming I am right about Q2 CPI being ~0.5%q/q, of course), and that they will use 25bps of that scope at their August meeting.

welcome back from blog holidays.

I think can speak for all of us in that you were sorely missed.

This article shows why

Welcome back :)

When the ABS reports that “overall employment rose 10.3k, thanks to a 14.8k increase in part-time employment offsetting a 4.4k drop in full-time employment” what population growth do they assume month to month? And what about per-state population growth? I find it strange that we have strong population growth with unemployment trending up.

Let’s see, quick calculation… the ABS reports that: “a net gain of one international migration every 2 minutes and 15 seconds”

In June we had 43200 minutes. That would mean a projected 19200 new migrants . If we assume that 65.3% participate in the labour force (same as the “old population”) that would give us 12537 new potential workers. Of these, 5.7% is unemployed, that leaves 11873 new migrants who got a job…. about the same as the amount of new jobs created reported. mmmmmmm. I do not think population growth is currently as strong as projected: it does not fit with the story of growth in the unemployment rate.

What about natural increase? Some kiddies get old enough each month as well.

Could not find those stats. The “theory” is that unemployment (which the ABS actually tries to measure) is going up but we are still creating some jobs because population is growing faster … well, that is true only if ABS population projections are correct. Otherwise we are losing jobs actually.

I have no idea if the ABS asks new migrants if they have a job. But I guess it would be hard, since they do not even know how many are coming in nor who / where they are yet! So they must be assuming based on last year a certain amount of migrants come here and a certain fraction of them has a job (maybe based on the rest of the population stats?), but I am sure it is guess work at this stage. The “new jobs created” info published by the ABS is not very useful to say the least!

This piece by Bill Mitchell makes heavy use of the “number of job created”. But it makes no sense to do that before we have population revisions. These numbers can change very significantly.

http://bilbo.economicoutlook.net/blog/?p=24619

Having “a net gain of one international migration every 2 minutes and 15 seconds” is significant. Are they part of the ABS survey too?

ahh, i see what you’re getting at. The population assumptions (they are assumptions, and are not measurements as you point out) are 0.134% /m, or about 1.6%y/y for the 3m in Q2’13. This is down from ~2.2%y/y rate in the qtr to March. You can find the population benchmarks in table three of the 6202 publication.

I believe so but have not checked. If the migrants are eligible to work (or merely say they are willing and able, the surveyor doesn’t care if you are illegal), presumably they must live someplace, and the household is the unit of the survey so i doubt they would be excluded.

Bill is very good, and i don’t think his note relies too heavily on ppn numbers. Certainly there is more sense in yoy comps than the more frequently emphasised mom comps.

Yes, welcome back. You didn’t quite manage a month, but a decent effort nonetheless :-)

It’s more of the same (the jobs report), isn’t it? If the RBA was keen to get us to zero, they couldn’t be doing a better job.

Speaking of which, a fascinating speech by Glenn Stevens last week. To me, it seems like a backside-covering exercise. Unfortunately, neither Hockey nor Bowen are up to the task of holding the RBA to account. Here are some bits I found most questionable:

Who cares about the CAD, the level of nominal interest rates, the exchange rate and sectoral impacts? The RBA shouldn’t. I find it striking that the RBA is defending the sluggish growth of the last 2 years on the basis that if we had stronger growth, some sectors may have found it harder. And I have no idea what he means when he says that if spending were higher, we would suffer more from the falling ToT. Something to do with gearing apparently… No – we are vulnerable now to the falling ToT because growth is already slow and UnN is rising. It would be much better to have UnN of 4.7% now rather than 5.7%. No one is suggesting we repeat 2006-08 – that’s a straw man. But to say that we couldn’t have enjoyed stronger growth this last 2 years is a major CYA exercise.

I did miss blogging – and my crew of regular commentators.

Funny you should say this (RBA pushing us toward the ZLB) as i’ve been looking at some VAR models and relative to prior history the RBA has cut too slow this cycle, which of course means the monetary policy shocks have been *tightening* shocks — as it’s the difference between expected and realised that ‘turns’ the model, so to speak. So yes, they are making the economy needlessly worse, and are lowering the cash rate trough.

Once you get into a VAR way of thinking, it makes sense.

In fairness to the RBA, the slowdown this time was more gradual and less severe than usual. Sumner had a good post a while back postulating that there are very few mini-recessions in the US basically because most recessions are caused by central bank inertia and desire to look responsible and not create panic by changing course too quickly and too radically. I think the RBA has been a bit lucky to date to avoid a mini-recession given that it has mostly been behind the curve for 2 years. The thing that worries me is that (just going on the RBA website) the Deputy Governor and most of the Assistant Governors seem to specialise in financial markets/stability rather than economics. Christopher Kent is the economics AG but he seems to be lower-profile than people like Guy Debelle. Just an impression. I know from a mate at the Fed that a similar thing has happened there – markets people have been greater prominence than economics people since the GFC.

I think this change has occurred as CBs have got interested in transmission mechanisms. 10yrs ago the entire financial market was a series of no arb eqns you might safely ignore. Not so any longer.

looks like somebody has spoken directly to the bank and u’ve picked it nicely ricardo:

http://www.afr.com/f/free/blogs/christopher_joye/august_interest_rate_cut_on_the_pFtRJ4dOuKP7WJAJak0qsJ

Thanks. I am a bit rusty … Good note by Mr Joye.

A strong return to the blogosphere. I think you meant to say the 95% range on the change is -20bps to +20bps.

I did check the ABS pub – pretty sure they had the range at 0bps to 40bps for June. I guess you mean the 95% range is -20bps to +20bps (which implies a point est of no change).

I should have called it the welcome RA edition but there is some good reading.

Simin Wren-Lewis has been really good of late

make that the Welcome BACK RA edition and Mark the Graph is at a gallop as well!!

Lots of good reading, that’s a pretty great reading list.

Typically one-eyed article by Adam Creighton in the Oz, entitled “August rate cut hopes dampened by RBA minutes”. The article and the small rise in the dollar since the release of the minutes seems to be grounded in the idea that the AUD depreciation would reinforce low interest rates in fostering a rebalancing of growth, thereby avoiding the need for another cut while at the same time increasing inflation slightly.

What he failed to mention was the crucial final sentence, which reads:

I was surprised too by the market reaction which sent the AUD up a bit.

When I read the minutes myself, I read the sentence “Given the exchange rate adjustment that was occurring, and with the substantial degree of monetary stimulus already in place, members assessed the current stance of policy to be appropriate for the time being.” as meaning “for now” e.g. for this month. I think this is more dovish than previous minutes.

Anyway the CPI will seal the deal. Since the meeting we had worse business confidence and worse unemployment. There’s no risk of inflation in Australia now, when credit is barely growing y/y and salaries are slowing down. If anything I think a lower dollar may put a lid on non-tradable inflation too and actually be deflationary since it will make it harder for people to save as much as they wanted to.