I think the RBA will — and should — cut their cash rate 25bps to 1.25% at their 7 May meeting. They have a chunky downgrade to put through for growth, inflation isn’t expected to get back to their target ever, and there are no financial stability reasons for maintaining the current cash rate.

The Q4 Growth problem

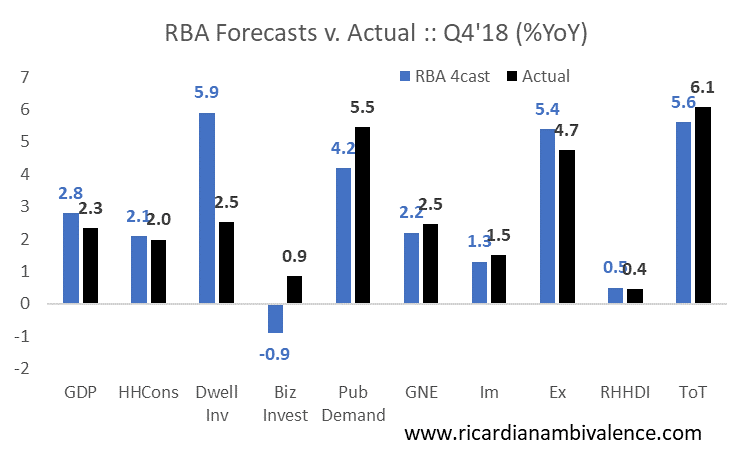

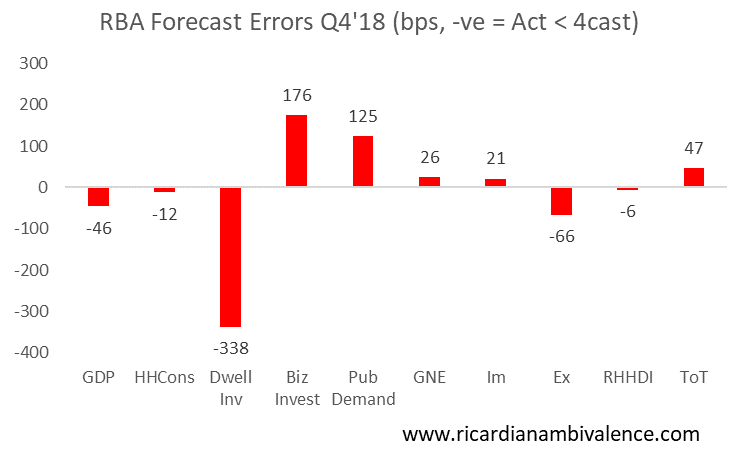

The charts above and below shows what happened v. the RBA’s forecasts. The basic story is that growth was ~50bps weaker than they expected due to weakness in household consumption and dwelling investment. This was offset by surprising strength of public demand. That’s probably not going to be sustained going forward.

The Q1 slump

It’s early to declare Q1, but i feel okay doing so given base effect and the weak data we’ve seen to Feb’19.

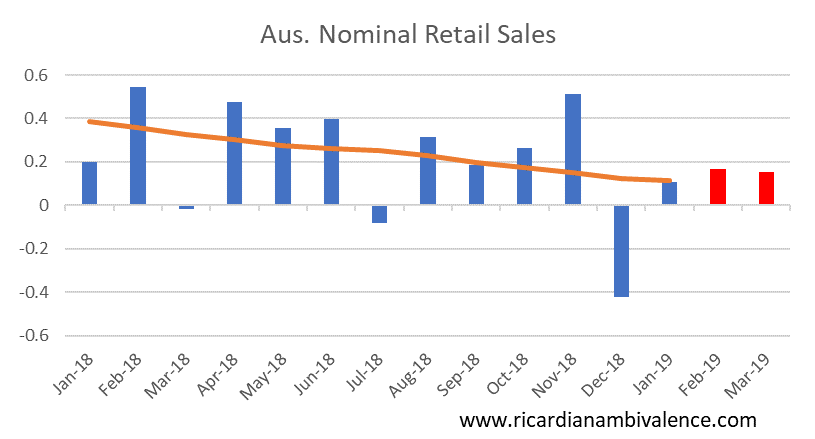

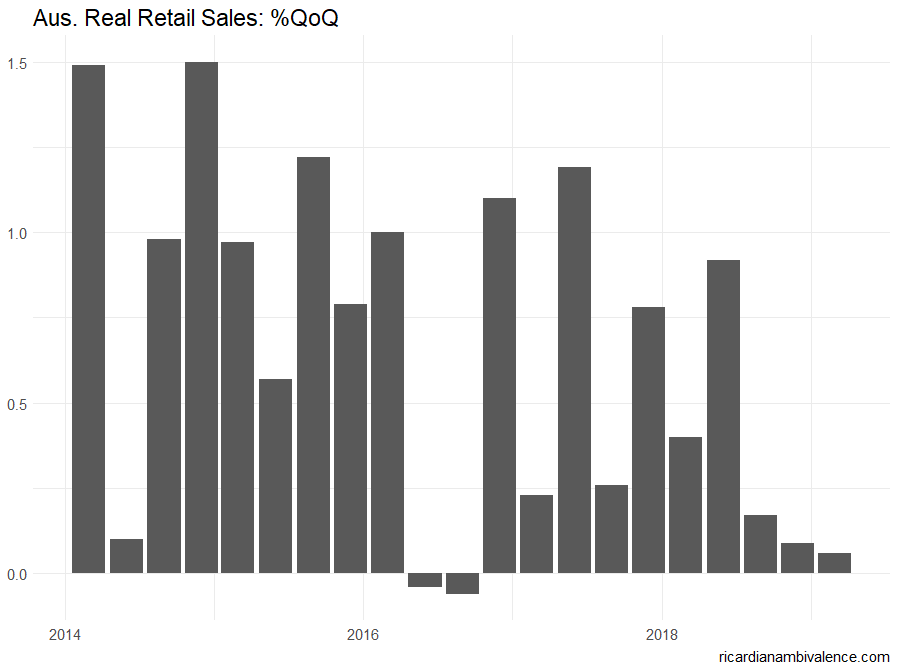

The base effect of the weak end to Q4 is particularly challenging. Consider retail sales, for example. We only know Jan’19 (+0.1%m/m) but we can say with a high degree of certainty that Q1 real retail sales will be soft.

To see why, consider the below chart. Let’s assume that we get slightly above trend outcomes for nominal retail sales growth in Feb and March.

This would yield nominal retail sales growth in Q1’19 of ~20bps.

Assuming that retail inflation is flat (the lowest it’s been year is 10bps), that means the best you could expect for real retail sales is ~20bps.

Personally i think that retail inflation of 10bps is realistic, which gives you the below chart for real retail sales growth.

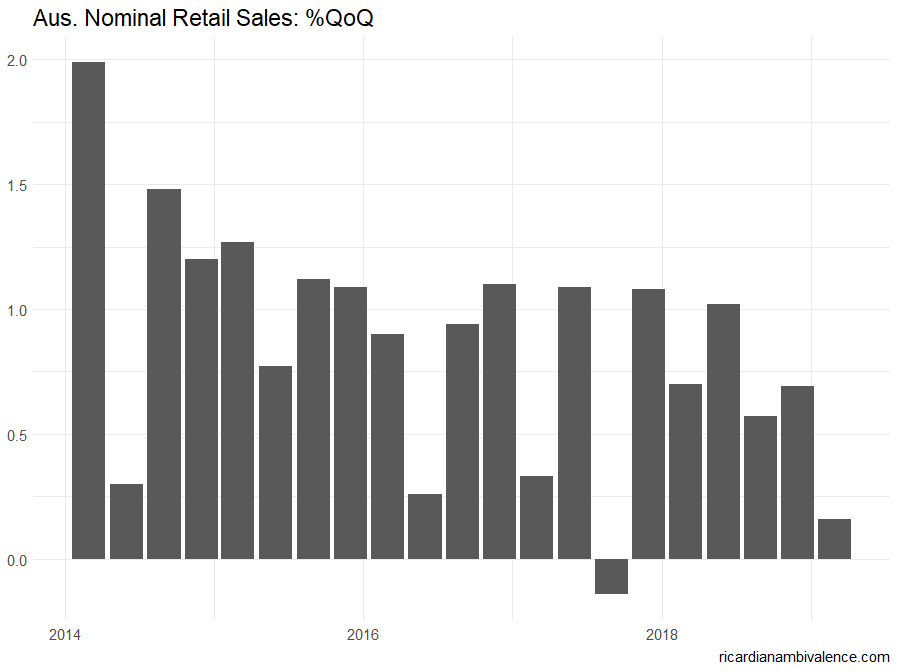

See the problem? So the growth downgrade should be larger than the ~50bps miss in Q4’18.

The RBA has been worried about a retail slump — and they have got one. Their is no financial stability reason to resist cutting the cash rate, and on current forecasts they never get (core) inflation back to target.

The only argument for not cutting is the Federal election (likely 18 May). The RBA has moved during an election campaign before. The most political thing they could do would be to NOT move despite the downgrade due to politics.

Sorry,

Beg to disagree,

Cutting cash rates from 1.5% to say 1% overtime will do little.

On the other hand boosting infrastructure spending would boost GDP in far better terms.

Our largest problem is wages. we Amy have entered US territory . Even re-regulation will not work as Unions are far too weak

Mario draghi agrees — but ended up he’s at negative rates and doing qe. Fiscal policy isn’t in Lowe’s gift.

RBA should cut in May, but they are too stubborn given the ongoing ridiculous growth forecasts and I personally can’t see it happening this quickly.

nottrampis – I agree that a rate cut will do little, but IMHO this does not mean the RBA should do nothing. If it lowers the AUD by enough, it will still be more than nothing. Infrastructure spending is already boosting GDP and to be honest the additional future benefits from many of these projects are marginal at best.

For sure the rba thinks thay it is worthwhile even if the banks don’t pass it on. The fx channel still works. As for the rba they have been upbeat and then surprised with cuts before. They may do so again.

There must be two labour force reports before May 7. Don’t you think Lowe would want to see some sustained evidence of an upward move in the UnN rate before he moves?

I think a forecast increase in the unemployment rate is all they will need.

If Philip “Borio” Lowe cuts after all this time on the basis of lower-than-forecast historical growth and a forecast rise in unemployment following many months of very robust jobs growth, it would represent a major easing in the RBA’s reaction function (ie stance). I predict a Dornbusch-style overshooting reaction of at least a 5% fall in the AUD/USD.

Punchy but possible. I am sure the RBA would enjoy that.

It occurs to me there is a divergence between GDP and Labour force figures.

Which ones are more accurate?

If it is labour force then no rate cut.

If not a rate cut ( and it is never just one) after the election

GDP leads. I have a hunch that the massive surge in government spending drove the jobs boom (ndis?).

On the money. Non-market sector employment hours up 4.2% in 2018. Market sector hours up 0.6%. Unless the pubic sector can repeat that effort employment growth is likely to hit the skids and the RBA will be cutting. It’s just a matter of time. Rubbish Feb and March figures and May is definitely on the table regardless of the election.