The Sumner stuff on per-capita measures of nominal income growth made me wonder if it made more sense to think about the flow of finance in a per-capita sense. I think it does.

With equivalent economic and credit conditions, you’d expect per capita funds flowing to be about stable (for a given demography … but this changes so slowly it’s not important in the present context).

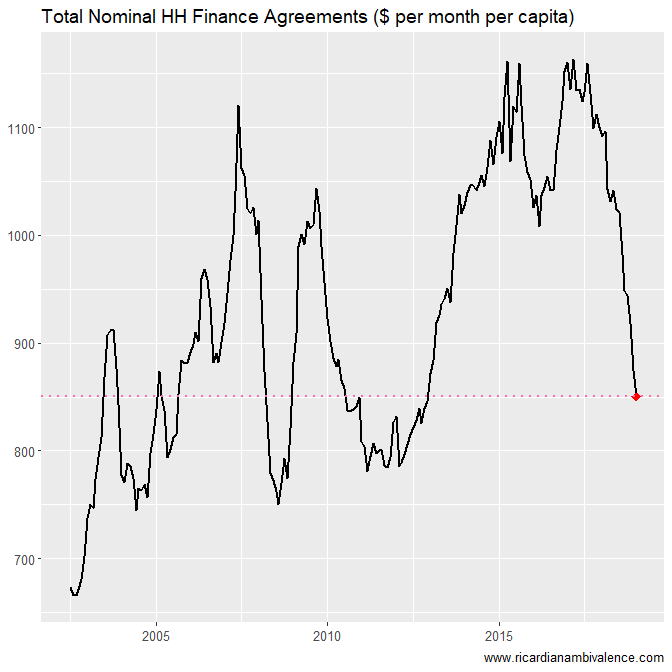

When you look at the recent decline in the value of new finance commitments in per capita terms (I use the civilian 15+ measure from the labour force report), you can see that this is around equal to the largest ever decline, and that we’re most of the way down to the GFC-low.

The pace of credit creation has declined from a high of around $1200 per person per month in Q1’17 to around $850 per person per month in Jan’19.

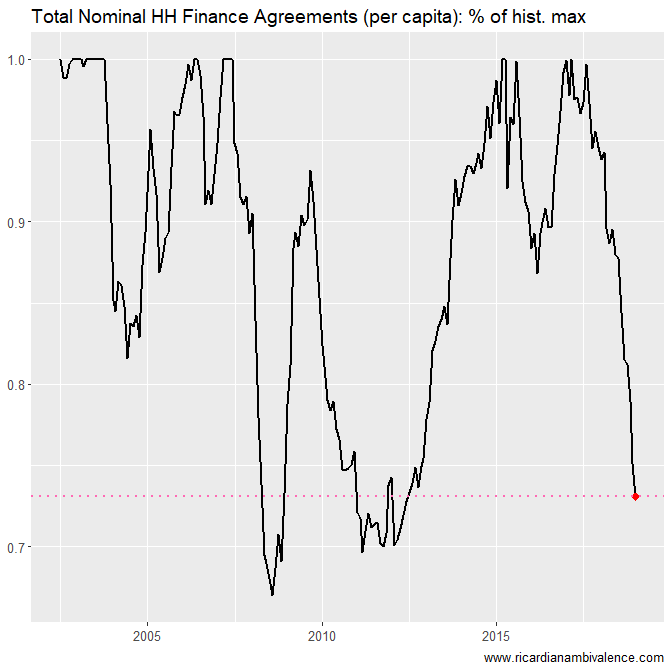

The below chart shows the current level as a percentage of the prior peak. So right now the flow of finance is ~73% of the Q1’17 peak (or equivalently is down ~27%).

The last two times the flow was down 30% the RBA cut rates. And both times by substantially more than 50bps.

I thought a credit crunch was when the markets don’t work as in what we saw back in 2008.

Even the CBA could not get funding

It isn’t that lenders are not lending because they are uncertain about the credit worthiness.

Less lending because of a housing downturn is more likely

perhap’s that is right. in that sense, the current situation is odd. Aussie banks have access to international capital markets, but aren’t lending. i suppose expected returns from both the demand (household) and supply side (lender) have changed in the last two years. however, i suspect that it also reflects that it’s much harder to get a loan.