I was a little thrilled when I saw a link to my blog from a Scott Sumner post on econlib (thanks Rajat!).

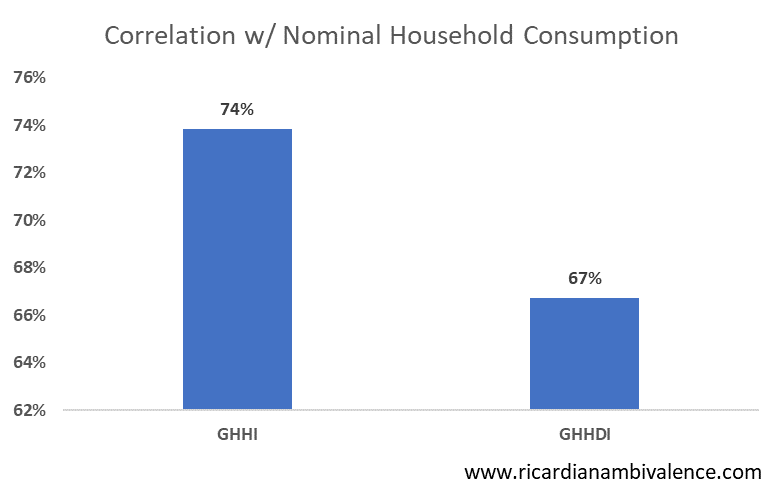

Scott took a look at my NGDP post and said that he prefers total labor compensation — which in the Australian National Accounts is called Household Gross Income (HHGI). The man knows what he is talking about — over the last 30yrs (1990+) the correlation between nominal consumption and HHGI is a bit better than the correlation with Household Gross Disposable Income (HHGDI). I had expected that variation of interest rates and tax rates over time would make HHGDI a better guide to consumption trends … turns out that’s not the case.

If you focus instead on GHHI, nominal growth is ~3.4%y/y, or about 70bps better than the growth rate of GHHDI. The difference between the two is “Total Income Payable”, which is growing at +5.75%y/y. That is an interesting story itself, but beyond the scope of this post.

In Scott’s blog about monetary equilibrium, he argues in favour of targeting a nominal income measure that is also adjusted for population growth. The growth rate of Australia’s civilian (15+) population is ~1.7%y/y, which brings the per-capita growth rate of nominal household income down to ~1.75%y/y (chart below).

From 1980 to 2012, the median growth rate of this measure was ~6%, so I would think that 1.75%y/y is a bit skinny. I’d love to know what Scott (or those of you who think this way) have to say about this development. I would suppose it means that monetary policy is way too tight.

I agree, of course.

Because I’m still stuck to my old ways, I am going to paste the deflated chart below. Annual growth of real per-capita income at ~20bps is around historical lows, and certainly consistent with the periods when the RBA has been cutting rates (the 1980 to 2012 average was ~1.75%). The wonder is that there’s any inflation at all!

Thanks for another post on nominal income!

I think Sumner’s claim is no so much that nominal GDP or nominal total labour compensation or whatever is a good guide to household consumption expenditure, but that stabilising that variable is the best way to help stabilise employment – which he sees as the main goal of monetary policy. He sees unanticipated slowdowns in nominal income growth combined with sticky wages & prices as being the primary cause of sharp rises in unemployment (ie recessions).

The question your previous posts raised for me is why would NGDP (in a highly commodity price-exposed place like Australia ) be a better lead indicator for employment growth than nominal gross disposable income. It must be something to do with the idea that firms hire based on how cheap workers are relative to the income firms are earning (eg N=f(W/NGDP)) – even if that income has not yet found its way into consumers’ pockets (via capex or government spending or taxes& transfers) and even (as you pointed out) it is destined to offshore to foreign shareholders. That seems a bit weird…

This post raises the additional question of why HHGI would be a better guide to consumption than HHGDI given that consumers only have access to money net of interest receipts & payments and taxes & transfers (which I presume HHGDI accounts for and HHGI does not). Again, it’s a mystery, but it must have something to do with the link between NGDP or HHGI and employment.

As for the recent ‘skinniness’ of HHGI, Sumner’s ‘musical chairs’ theory of employment and recessions depends a lot on expectations of nominal wage growth. Clearly, these have been ground down in Australia (as elsewhere) post-GFC. In Australia, this adjustment was delayed due to the 2009-11 ToT and NGDP boomlet, but people certainly don’t expect much growth now. That means that growth in NGDP or HHGI or whatever can be much slower than previously and still generate reasonable employment growth. Incidentally, one flaw I see with Sumner’s apparently-preferred nominal total compensation per capita measure is that it would be negatively affected by demographic factors – eg ageing – that might not affect negatively affect the unemployment rate. Hence, I’m not sure if it would be a great target variable.