My argument for a May rate cut by the RBA basically boils down to the observation that inflation is very low and that there’s no financial stability reason not to cut — plus the judgement that the very low pace of inflation means that the prior test requiring the unemployment rate to rise is no longer needs to be met.

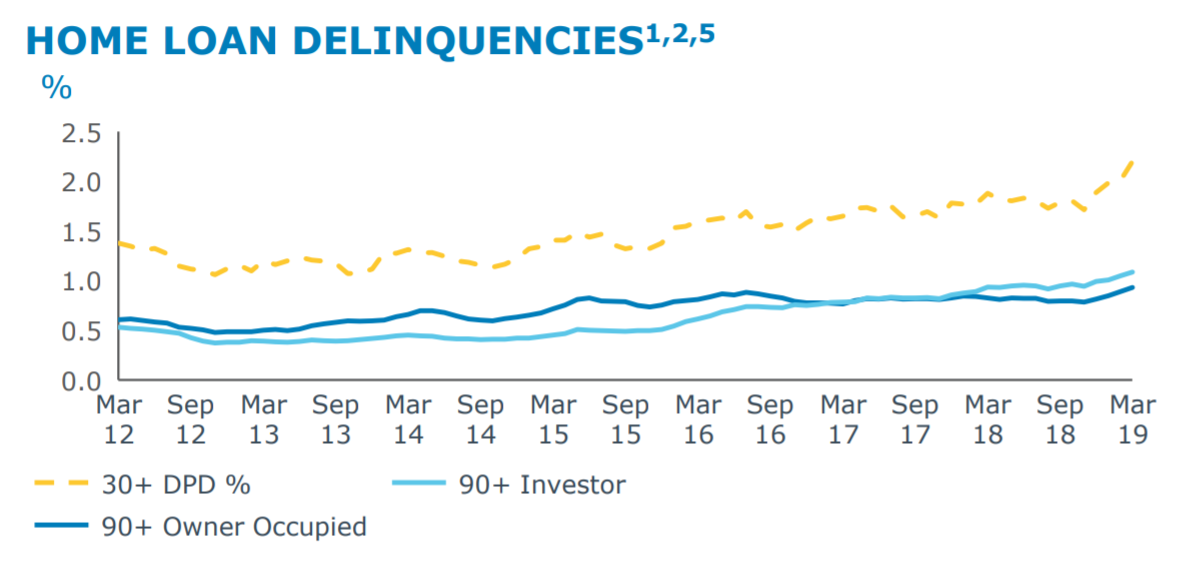

Looking at the ANZ H1’19 results pack suggests that there may even be a financial stability argument for lowering the RBA’s policy rate. The chart below shows the sharp increase in home loan delinquencies across the ANZ loan book over the past few months — and in particular over Q1’19. I think this is strong confirming evidence of a softer household / consumption sector.

This is no longer just a WA-story. The chart below shows the breakdown of late loans (90+ days past due) by state. Note the sharp increase in sour loans in NSW & ACT. Something’s going on Mr Jones.

Much of the trouble with repayments seems to be with the older loans. The 2yr seasoned 2017 vintage loans, for example, have lower delinquency rates than the 2015 and 2016 vintage did at the same time — though all are souring.

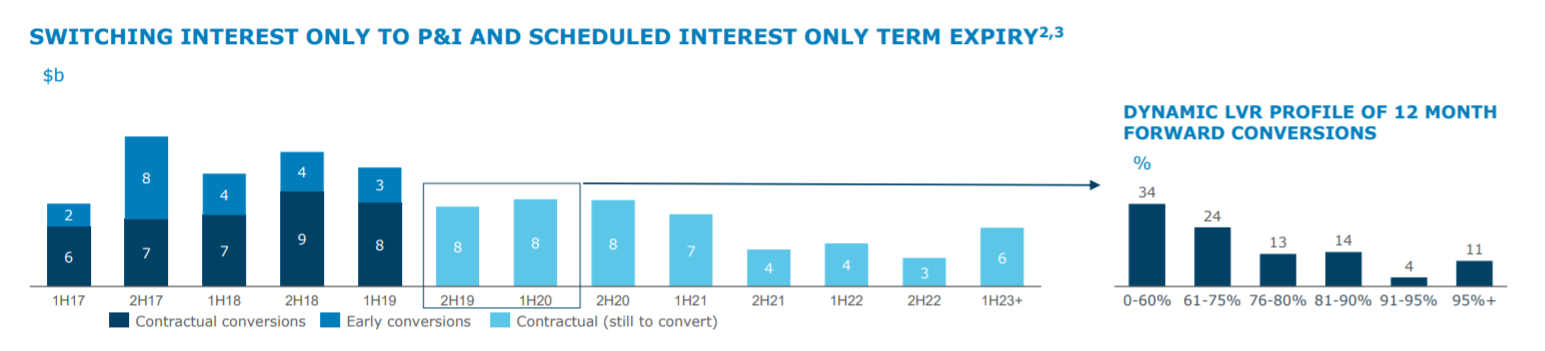

The pressure on loan quality from the expiry of interest only terms is likely to intensify — and this should keep up downward pressure on consumption. The ANZ forecasts about the same level of IO-to-PnI switching (for contract reasons) over the next two years. The issue with this is that about 30% of these households have LVRs greater than 80% — which means they’ll find it very hard to refinance into better / more suitable deals.

Given that house prices continue to decline, it follows that the proportion of loans with low equity will continue to increase (few people pay enough per month to keep up with the current pace of declines). At present, the share of the ANZ’s loan book that’s in negative equity has been stable at 5% for some time — but note that the orange bars for less than 80% LVRs are getting smaller, and that the 80%+ bars are getting larger. The mark-to-market from falling house prices is hurting.

This is a potential financial stability issue. The RBA can do something to limit these brewing risks. A lower cash rate would reduce monthly repayments and therefore mortgage delinquencies. It would also slow the decline of house prices, which increase the proportion of those trapped in mortgage arrangements they cannot afford to refi away. Selling into a weak market is bad for everyone.

wow,This is interesting

Yes I thought so. Clear evidence that the various changes to the mortgage market are causing a bit of stress.

You betcha.

I am in your camp now.

welcome aboard. we can be nervous together on tuesday.

no good. we missed

Thanks for sharing this post!!