My call that the RBA would cut rates in May was originally a little speculative — but following the Q1’19 inflation data, and weak credit data, I now think that it’s very solidly grounded in vanilla macro.

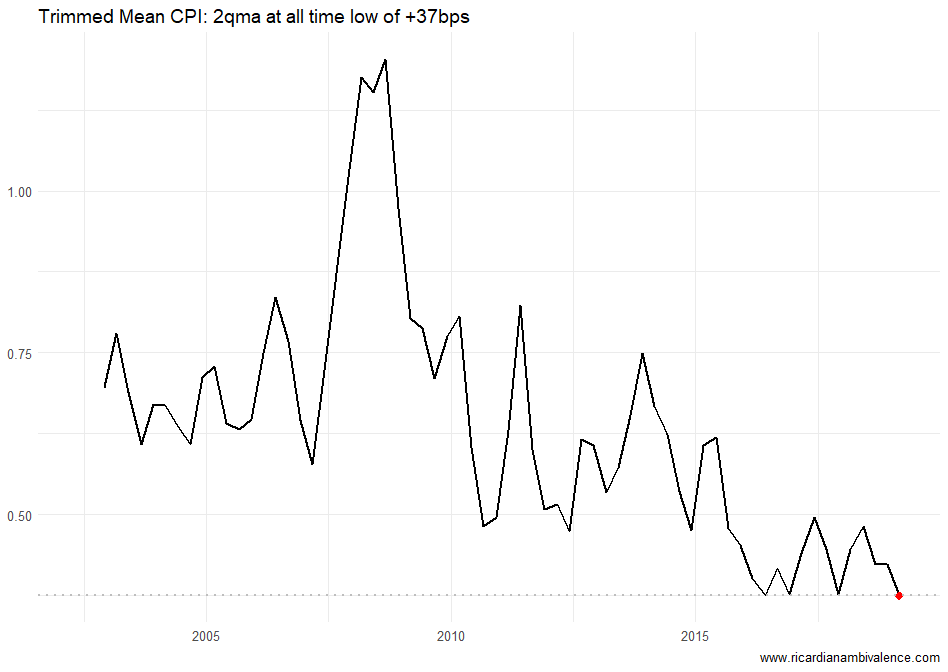

First of all, the very low inflation print cannot be dismissed as a once off. If you take the two-quarter average (as i have done in the above chart), trimmed mean CPI is at an all time low of 0.37%q/q. Given that growth is (at best) around trend, and that the unemployment rate has been stable at ~5% for two quarters, there is no reason to expect inflation to accelerate. Due to measurement issues, inflation is always overstated, so CPI at this level probably means that prices are flat — or perhaps falling a little.

So the question is, assuming current policy settings, can the RBA produce a compelling case that inflation will return to target in a policy relevant time period? I don’t think that they can do so — so the policy rate must fall.

Sure, inflation has been too low for some time, but for most of Gov Lowe’s term, there’s been a trade off between the inflation target and financial stability. This was laid out in Gov Lowe’s landmark speech, Inflation and Monetary Policy, on 18 October 2016. In that speech Gov Lowe emphasised the ‘third pillar’ of the RBA Act, ‘the economic prosperity and welfare of the people of Australia’. The point he made was that rushing the return to 2.5% inflation could have deleterious consequences for the state of household balance sheets.

Over recent times, we have considered the impact of our decisions not only on the future path of inflation, but also on the health of the balance sheets in the economy. Achieving the quickest return of inflation back to 2½ per cent would be unlikely to be in the public interest if it came at the cost of a weakening of balance sheets and an unsustainable build-up of leverage in response to historically low interest rates.

Gov Lowe, Inflation and Monetary Policy, Oct 2016

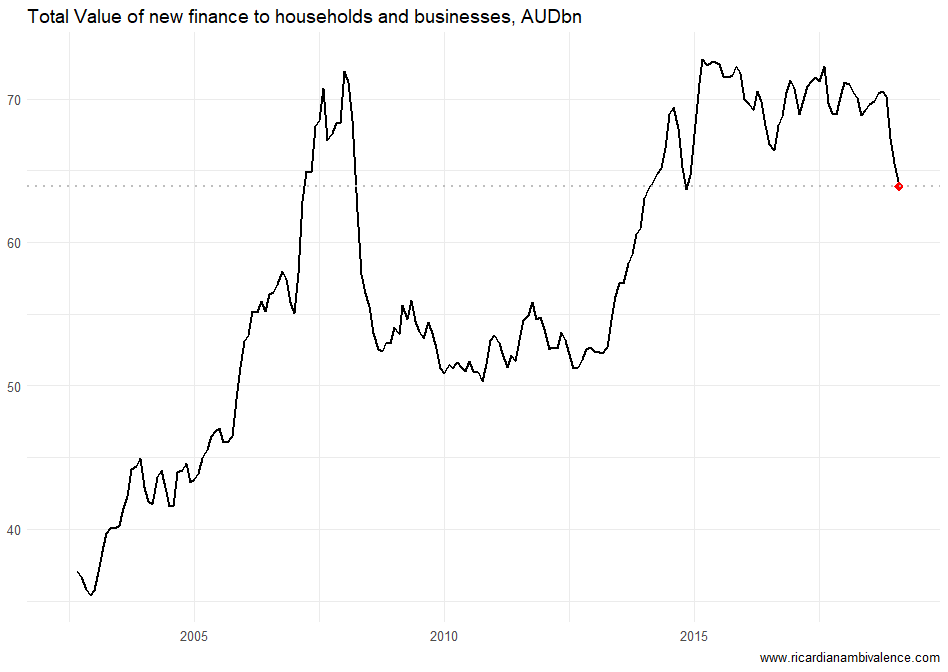

Does anyone think that’s still a barrier to rate cuts? The chart below shows the total value of new finance agreements (to households and firms, 3mma). As you can see, this has fallen sharply of late, and is now at the lowest level in 5 years (since 2014). If you adjust for the larger population / size of the economy this looks even weaker.

The RBA were already considering lower rates following a string of weak growth data — but were reluctant to cut until the famously noisy GDP data was confirmed by rising unemployment. Some argue that the RBA needs to see rising unemployment to cut — but i don’t think that test is relevant any longer.

The low CPI print totally changed the debate. Inflation is too low and the RBA needs above trend growth and a falling unemployment rate to make a case that inflation will accelerate. They don’t have a plausible story about a return to on-target inflation just now. On current policy settings, and assuming a healthy dose of optimism, I can’t see a plausible above trend GDP forecast until mid 2020 — which means inflation doesn’t get back above 2% until 2021.

When will it get back to 2.5%? Who knows. On current form you’d have to guess it’ll be after Gov Lowe’s term ends. Cutting the cash rate is the only way Lowe can have a chance of hitting his inflation target during his term. With a bit of bad luck he might even average something with a 1-handle.

A final point about politics: I don’t think the RBA will be constrained by the 18 May election. I doubt they will even discuss it. Therefore i find it curious that so many are calling a June or July cut. Such a move would look political itself. It would have to be very carefully managed.

Two thoughts.

tax collections are strong.

On the other hand economic data is mixed when the economy is changing

Impeccable logic; the contrary argument is as follows…

Guy Debelle’s recent speech referred to:

https://www.rba.gov.au/speeches/2019/sp-dg-2019-04-10.html

The RBA’s April minutes said something similar:

https://www.rba.gov.au/media-releases/2019/mr-19-07.html

While the RBA sees GDP ultimately affecting employment, the fact that they see a “tension” – rather than just talking about lags – suggests they don’t see a one-for-one relationship. As a believer in the importance of NGDP growth to employment growth, I think employment growth could well hold up for longer than most people think, so in a sense, they could be right for the wrong reasons – wrong reasons as in the RBA seems to have a cost-push model of inflation, as in a tight labour market pushes up wages and prices, rather than strong nominal demand pushing up prices and wages.

The fact that the market is not pricing-in a cut more strongly doesn’t mean the market thinks the RBA will reach 2.5% or even 2% any time soon; but rather than the market doesn’t think Lowe cares that much about the target. That’s a terrible sign if you think about it, but I believe he has spent too much of his academic and professional career devoted to leverage phobia. It’s very hard to jettison that sort of investment – the sunk cost fallacy is a very human response – and especially having just pointed to the important role of employment. If they were going to flip, I would have expected the RBA would have spent a bit more time in recent commentary covering themselves by saying positive things about diminishing leverage/finstab risks, but I don’t believe they have.

One thing’s for sure – the May decision and statement will tell us whether Lowe is ultimately an ideologue or a pragmatist.

i totally agree with you — Lowe has done a great job of telling everyone that he cares more about financial stability. but that doesn’t mean he can just dump the inflation target. I think he over-achieved when he was fighting the (internal) doves in 2016. He won with the financial stability counter argument — helps to be the boss — but the staff that thought the cash rate should be 50bps in 2016 mostly still work at the bank. I just don’t think the financial stability story is a strong counter-argument any more. and in my experience Lowe is pragmatic. let’s hope.

If i were the Government i’d be coming after the RBA hard. If he’d hit his target, nominal GDP would be ~2% larger — and the unemployment rate would be lower and the budget in better shape.

It’s now genuinely on a knife edge, however I think to dismiss his prior actions (inaction) and preferences is maybe looking at it too clinically, albeit not incorrectly. To cut now in the absence of any black swans is to admit error in prior policy, and men in senior positions are traditionally reluctant to do this.

The greatest “irony” / failing of this whole “financial stability” narrative is that their actions have actually weakened household balance sheets, by having asset values fall without the equivalent deleveraging. More problematically though, by keeping growth sub par they have also brought closer the potential for proper “financial instability” via rising unemployment, although (remarkably) it still hasn’t manifested.

I appreciate that everyone’s values have a point of capitulation hence why he could well cut in May but I think the ship has sailed on whether he is a pragmatist or an ideologue.

I think this decision is much more a human decision than a mechanical one, but that said, the one human factor in favour of a May cut is he might seek to stave off greater reputational damage given that the market is now demanding a cut and if unemployment spikes or there is another big CPI miss next quarter his reputation will be in complete tatters. A May cut could be a tactical withdrawl to at least preserve some of his esteem.

50.1:49.9 for a hold, with a cut to come if there is a bad move in UE (or a really bad one in job ads) or, if that hasn’t happed prior, another weak CPI next qtr.

Lowe is at risk of becoming mr 1%. The prior two governors hit 2.5% exactly. I can’t believe he could just ignore his target

He’ll argue in his memoirs he had bigger “financial stability” fish to fry. I think his actions to date reflect his prioritisation of so called financial stability over a mid range target. Also, he could arguably make the case that his 1% reflects consistency with his international peers in the way, I assume (without having the data), that their 2.5%s were probably in the ballpark range of their peers.

It’ll only sound reasonable if the housing adjustment works out. Else he will have allowed his ammo to depreciate for no reason.

Have another look at the April minutes — one read of the comments about cutting rates is that the board figured it wouldn’t create financial stability issues.

Maybe by implication, “the effect on the economy of lower interest rates could be expected to be smaller than in the past”. But immediately preceding that it speaks to no rise in inflation *and* higher UE being the trigger. Obviously inflation falling off a cliff wasn’t contemplated.

I still think they are going full Mick Malthouse with the Ox is slow but the earth is patient, but the reputational downside risk does have me worried a little that they’ll go earlier than I think.

I was already sold on the growth problem—and perhaps that was never going to be enough… but surely the low cpi changed the test? I would have thought so. If he doesn’t cut in May I doubt he will average anything starting with a 2-handle.