The slow pace of inflation in Q1 makes a very strong case for a 25 bps reduction of the RBA’s policy rate on 7 May, to 1.25%.

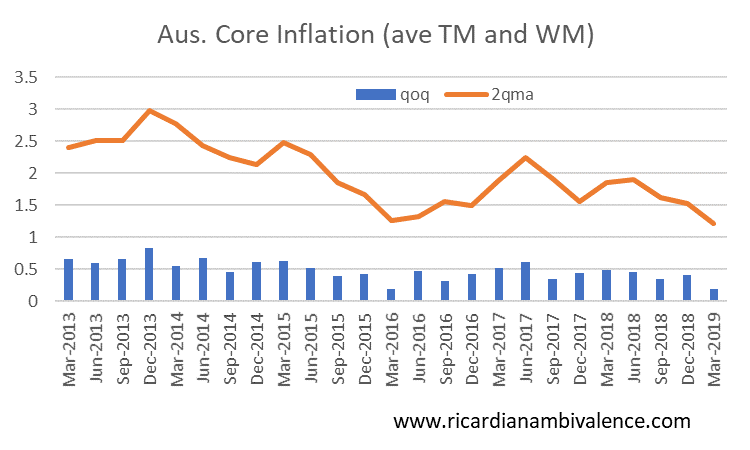

The key trimmed mean inflation measure increased 28bps to be 1.6% higher over the year. This is a 24bps deceleration from the Q4’18 print of 1.84% (it has since been revised down to 1.82%). Nor is the weak inflation pulse some figment of the trim’s construction. The weighted median measure increased by just under 10bps to be 1.24%yoy.

This took the average of the RBA’s two Core measures of inflation up ~19bps on the quarter to by ~1.42%yoy. This is being held up by the higher prior prints. The 2qma is a good balance between signal and noise, and on this basis core inflation was ~1.2%yoy. Both the two-core qoq and the 2qma are below the low inflation prints of early 2016 (of 20bps and 1.26%). These low prints led RBA Gov Stevens to cut the cash rate, despite a falling unemployment rate.

So coming into the May meeting, the facts are that domestic growth disappointed, inflation disappointed, global growth slowed, and the labour market cooled a little. There is some disagreement between the different data sets, but the story is substantially completed by CPI.

We learn a lot about the balance between supply and demand from the CPI release, and the message from the details of today’s report is that the output gap is widening — in line with the slow GDP data. This makes sense: the origin of the weakness is housing, and falling house prices are slowing consumption — so we should expect CPI to be weak.

That is exactly what we see — sequential slowing of CPI over the prior year.

The fact is that the current data means the RBA cannot present a credible case for a return of inflation to their 2.5% target within Gov Lowe’s term — with current monetary policy settings. So monetary policy must be eased.

The only reason i can think of to leave monetary policy unchanged at 1.5% would be to avoid the federal election–but that is a political act in itself.

The lack of progress toward the inflation target justifies a rate cut, notwithstanding mixed signals on growth. The least political thing the RBA can do is to follow their forecasting/policy process and deliver one.

I think the economic case for a 25bps cut is a slam dunk — because the economy can run hotter, and should be allowed to do so.

I am in complete agreement but still think they wlil wait a month.

It isn’t a Glenn Stevens moment yet

It would be odd to cut at a non-SOMP meeting.

elections are odd things

It’s a big miss on CPI, but just one month after saying (i) they can’t fine-tune outcomes, (ii) headline inflation is expected to fall due to petrol prices, and (iii) they need to see rising trend unemployment to cut… it would be quite contrary to guidance and a bad look for Lowe. On the other hand, they had expected underlying inflation to remain “broadly stable” and it has fallen. Plus, market economists have capitulated. (Jeez, ANZ really needs a cleanout – losing Hogan clearly wasn’t enough…)

On balance, I think they’ll wait. Lowe will be pleading for another quarter, arguing that while unemployment is steady and with petrol & cigs bouncing back, the CPI will recover.

Internet job vacancies was released about 30 mins before the CPI and was ignored as usual. Another poor result. It’s only a matter of time before employment growth rolls over.

tax revenues suggest a stronger economy does it not?