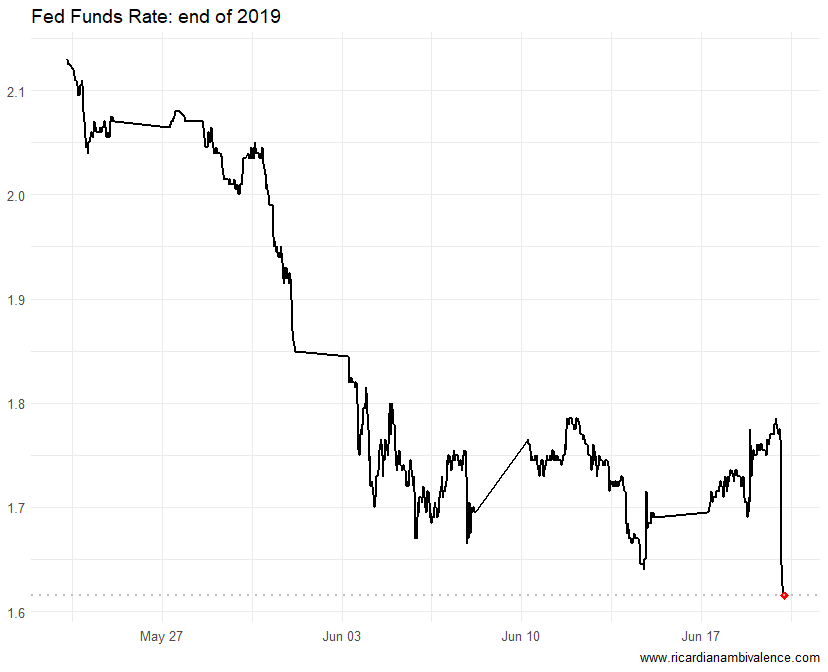

The Fed spiked the market with dovishness this morning. Taking the market implied rate for the end-19 fed funds rate down ~18bps to ~1.6%. I think the Fed is likely to match the market: delivering a 50bps cut in July, and 25bps cuts in each of September and December. This will leave the funds rate at 1.5% by the end of the year, which is basically what the market wants.

I don’t think this is about growth. It’s about inflation. The main forecast change was the (slightly) lower inflation profile (core PCE -20bps in 2019 and -10bps in 2020). All the growth related stuff was better: GDP was revised up a touch (+10bps in 2020), and the unemployment rate profile was trimmed by 10bps across the profile (though the LR fell 10bps too, so there’s no incremental signal about capacity).

So what happened? They lost confidence in the stability of inflation expectations.

As i noted earlier, the Fed has (finally) twigged to the fact that a decade of 1.5% inflation has consequences. Their May meeting minutes showed that the staff had lost confidence in the stability of inflation expectations. And of course Clarida’s speech entitled Sustaining Maximum Employment and Price Stability on 30 May, suggested that he was the King of the Doves.

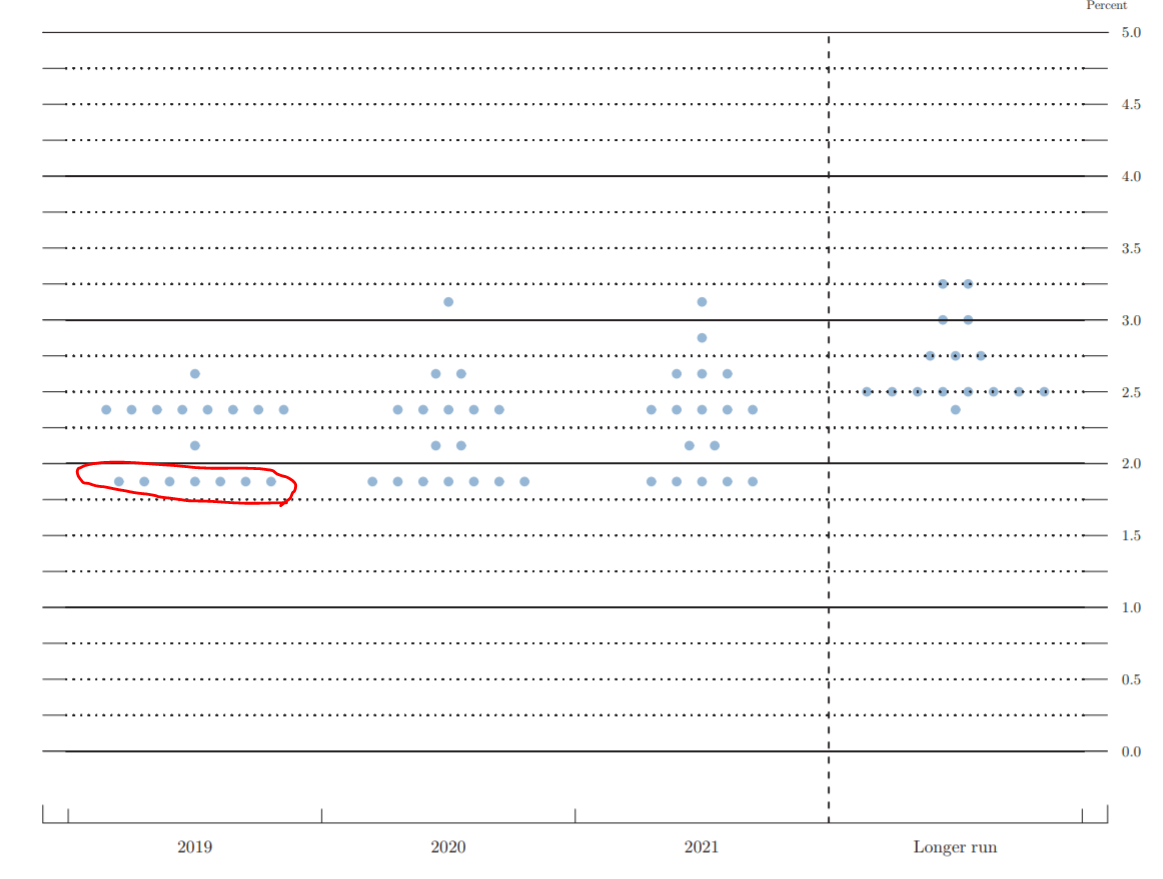

When you look at the dot plot, it’s clear that the committee has split into two camps. A group of eight voters that favour cuts (7 voters who favour 50bps of cuts and one that favours a single cut) and another group of nine voters that favour steady rates. It’s a miracle that there were not more dissents.

In the event, there was only one dissent that this meeting — the reliably dovish Jim Bullard. My guess is that Powell headed off a larger dissent at this meeting by saying that he’s open to cutting rates 50bps in July if data confirms the need. He said as much in the post meeting press conference.

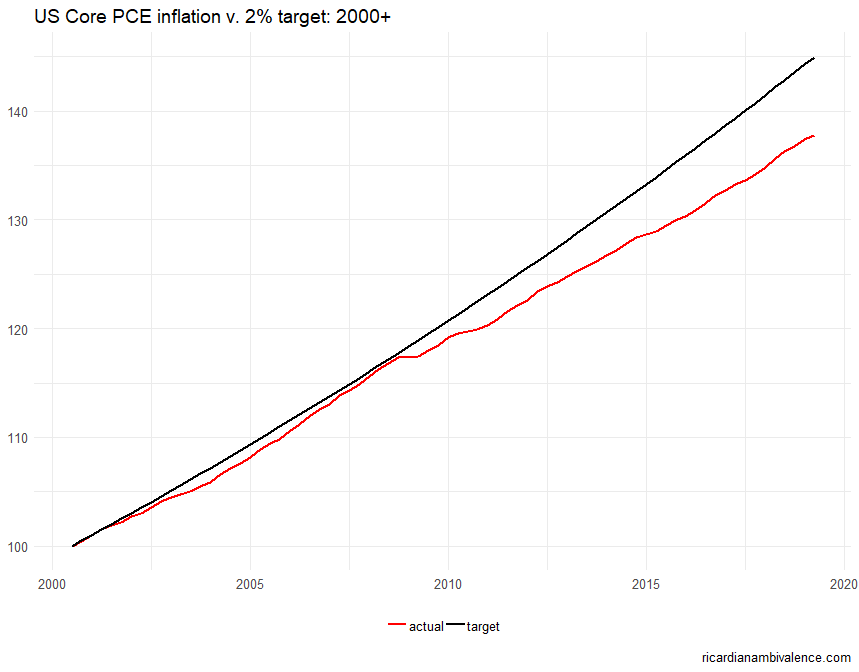

So what happened to ‘transitory’? All this stuff about ‘transitory’ factors lowering inflation is nonsense. The Fed has been delivering ~1.5%y/y inflation for most of the last ten years. Every year or two there’s a new transitory factor.

There’s a name of an ongoing series of transitory inflation shocks — it’s competition. If you get too close to it, there’s always a micro explanation that makes it seem like a once off (cell phone plans, etc) — but over the years, the 2% forecast always ends up converging to a ~1.5% reality.

They would not like an inverted yield curve either