Vice Fed Chair Clarida gave a very interesting speech entitled Sustaining Maximum Employment and Price Stability on 30 May.

It was interesting not only because it laid out two paths for rates cuts in 2019, but because it strongly suggests that Clarida is the leader of the dovish camp that keeps popping up in the Fed’s Minutes.

I feel the section laying out the path for cuts has been distorted in most reporting, so I’m going to cut and paste the entire section:

… [1] if the incoming data were to show a persistent shortfall in inflation below our 2 percent objective or [2] were it to indicate that global economic and financial developments present a material downside risk to our baseline outlook, then these are developments that the Committee would take into account in assessing the appropriate stance for monetary policy (my emphasis, and I also added the numbers)

So the two paths to a cut are: 1/ continued low inflation; or 2/ the accumulation of downside risks (not eventualities, just risks).

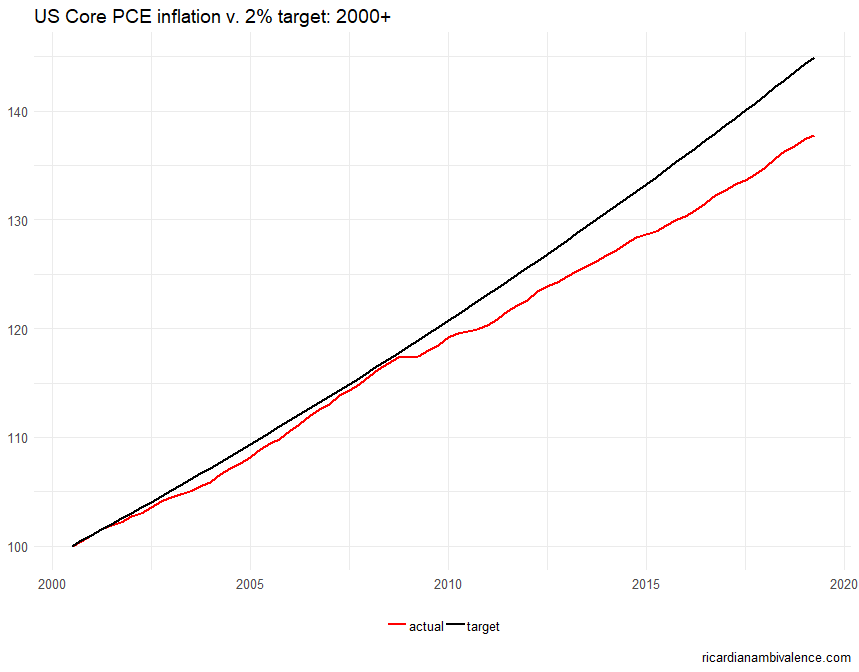

Trump seems to be working on the downside risks — but who really knows about forecasting shocks … but we can say pretty clearly about core PCE. Q1 core PCE was only 1% and the Cleveland Fed nowcast for Q2 is presently 1.2%. The Fed needs inflation ~2.85% for the second half of 2019 to hit their 2% target (and forecast for 2019). That’s clearly not going to happen. If the Cleveland Fed Nowcast is right, the the Fed will cut by 50bps before the end of 2019.

I noted right after the minutes that the staff appear to have lowered their assessment of inflation expectations. I thought this was staggering. What I didn’t emphasize was the dovish camp among the fed members (or participants, as they are called in the minutes). I had mistakenly believed that it was Jim Bullard — a nice bloke, but not currently at the center of the FOMC.

I was wrong. The speech today suggests that Vice Chair Clarida is the King of the Doves: and this has a meaningful impact on the probability of easing this year. In my view, Vice Chair Clarida is campaigning for a rate cut to protect against declining inflation expectations.

And it’s a good campaign. There’s good reason to worry about falling inflation expectations: the Fed has done a terrible job of hitting their inflation target over the past twenty years. The accumulated miss is ~500bps, with most of that miss being due to inflation averaging ~1.6%y/y since 2009.

Finally, for reference, here are a few excerpts from the Fed minutes and Clarida’s speech.

Compare the below from the minutes of the 1 May meeting:

Some participants also expressed concerns that long-term inflation expectations could be below levels consistent with the Committee’s 2 percent target or at risk of falling below that level.

With this from the speech:

I judge that, at present, indicators suggest that longer-term inflation expectations sit at the low end of a range that I consider consistent with our price-stability mandate.

… and compare this from the minutes:

… a few other participants observed that subdued inflation coupled with real wage gains roughly in line with productivity growth might indicate that resource utilization was not as high as the recent low readings of the unemployment rate by themselves would suggest.

… with this from the speech:

Wages have been rising broadly in line with productivity and prices and thus, at present, do not signal rising cost-push pressure.

and finally, this from the minutes:

Several participants commented that if inflation did not show signs of moving up over coming quarters, there was a risk that inflation expectations could become anchored at levels below those consistent with the Committee’s symmetric 2 percent objective—a development that could make it more difficult to achieve the 2 percent inflation objective on a sustainable basis over the longer run.

… with this from the speech:

… a flatter Phillips curve makes it all the more important that longer-run inflation expectations remain anchored at levels consistent with our 2 percent inflation objective.

One comment

Comments are closed.