Terry McCrann (again) spiked the markets on Wednesday with an explosive article that warned that the RBA could cut 50bps in July.

Even an opposition surprising us all by behaving responsibly is now not going to stop — at the very least — a second rate cut. And the odds of it being delivered immediately, in July, shortened into Wynx-territory after yesterday’s unambiguously and decidedly unwelcome weak GDP numbers. Only a seriously strong jobs report on Thursday week now stands in the way. A seriously bad report could deliver a 50bps cut.

Terry McCrann: Bad news on economy demands both tax and rate cuts

For those that don’t know, Winx is a horse than won 33 consecutive races. So Terry’s claim is that a July rate cut is what you’d call a ‘racing certainty’ — or a very good bet. I’m not so sure myself.

What’s right about this is that the RBA is going to deliver at least 50bps of easing, taking the cash rate to 1%, and that tax cuts won’t stop this … after all, the RBA had assumed 50bps of easing in May and those forecasts were already poor — so 50bps of cuts is a minimum, and more cuts are more likely than fewer cuts.

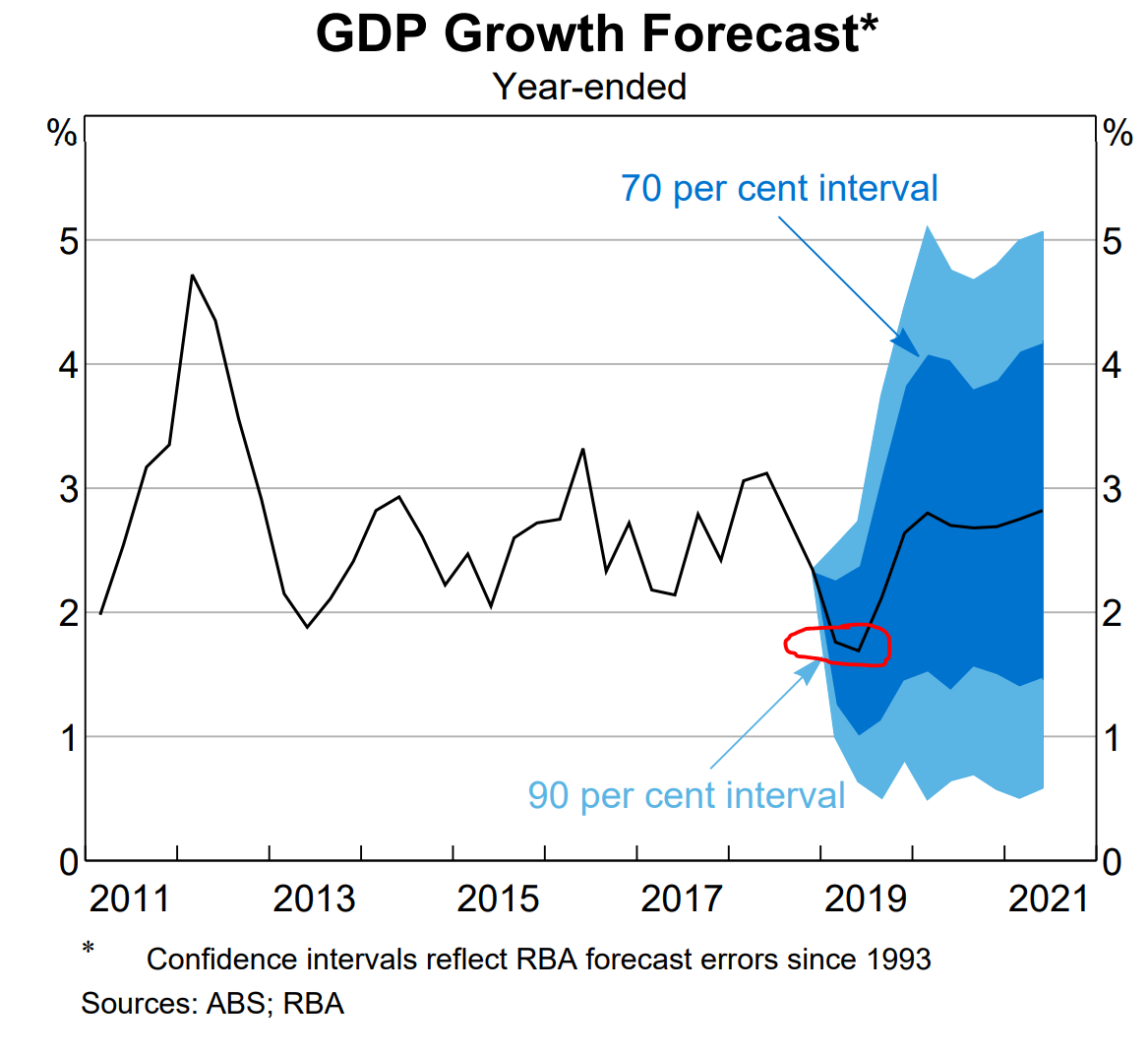

What is wrong about this is the claim that the GDP numbers would have come as a shock. The RBA only puts mid-quarter (%YoY) values in their forecast tables — but we know from the table that Q2’19 is expected to be ~1.75% and we can see from the fanchart that Q1 was also expected to be around that level.

So yesterday’s 1.8%y/y outcome looks like it’s basically in line with the RBA’s published forecast.

Looking forward, I both agree and disagree with Terry’s comments about the outlook. Here they are:

It makes it all-but impossible for the RBA to reach its — continually revised down — very ordinary 1.7%y/y GDP growth forecast for the June year just ending. It would need quarterly growth to double from March’s 0.4% to 0.8%. It will also take a miracle economic rebound for growth to come near the 2.6% RBA forecast for the 2019 calendar year.

Terry McCrann: Bad news on economy demands both tax and rate cuts

I never really believed that the May GDP forecasts were credible. So while I agree with Terry when he says that the RBA’s forecasts will be hard to hit, I don’t agree that it’s the Q1 print that makes those forecasts ‘out of reach’.

The fact is that both the pace of growth and the level of GDP in Q1’19 are where the RBA forecast them to be in the May SOMP. So we start Q2 exactly where the RBA expected to start it: at 1.8%y/y and needing a strong bounce back in Q2 to meet their projections.

Is a 0.8%qoq print in Q2 likely? No, I don’t think so. But then it never was (the May SOMP forecasts look too much like the April budget assumptions for my taste).

In his speech on Tuesday, Gov Lowe told us that his outlook for the Australian Economy was unchanged; and then Q1’19 GDP printed exactly as his staff had forecast in the May SOMP. So the argument from Q1 GDP to a July rate cut doesn’t persuade me.

I would have thought August is the go given it is after the next CPI.

some thoughts on QE pls