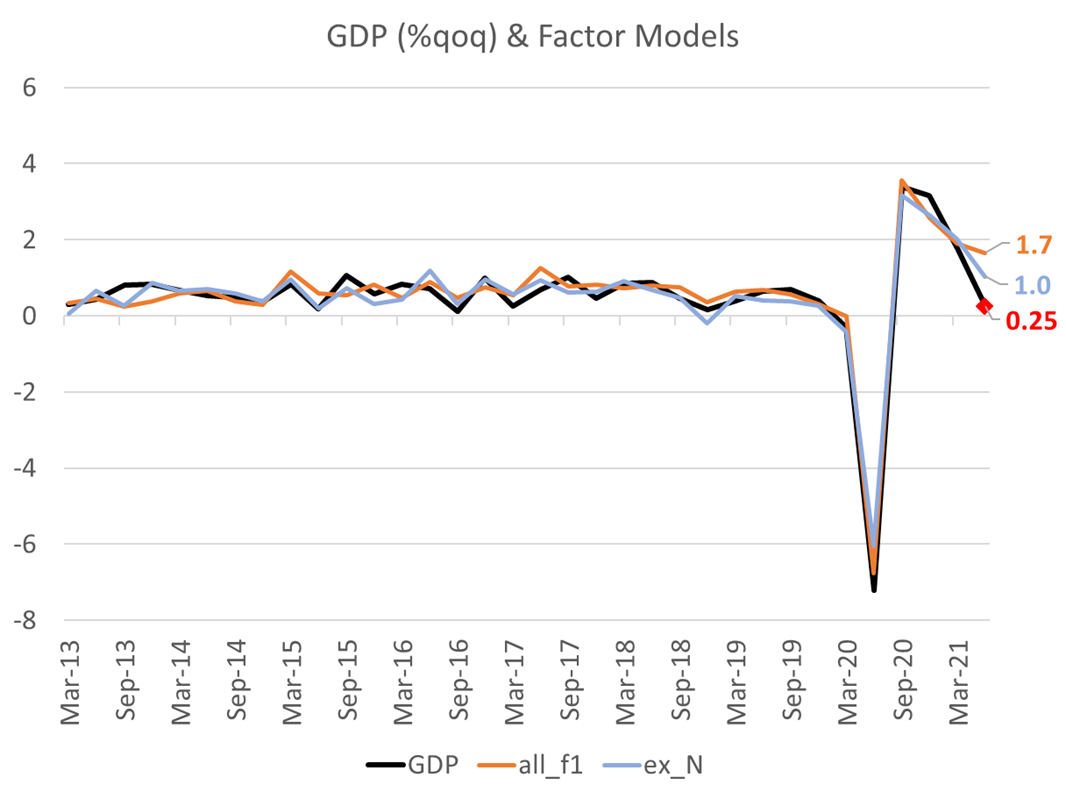

Q2’21 GDP is going to be weak: say +0.25%qoq. More likely 0%qoq than 0.5%qoq.

My tracking estimate of the GDP-expenditure has fallen to -0.2%qoq. The headline GDP number is likely to be a bit better than this as it’s an average of three measures, and the (limited) partial indicators for GDP-income and GDP-production are better than than the expenditure numbers. It’d have to be pretty much the largest error on record for it to reach the RBA’s +0.75%qoq August SOMP forecast.

There will be a bit of new information in the GDP release, but based on the information we have, the underlying economy seems likely to have been much better than the an ‘adding-up’ approach to GDP will suggest. This is probably intuitive, if you know about the large subtractions from GDP due to net exports and business inventories. Domestic demand looks to be tracking around 1.25%qoq.

There are alternatives to this ‘adding-up’ approach to GDP (see this RBA RDP). These take a weighted average of the information in the various inputs, plus other inputs, and the weighted average than maps into GDP (the two models below enjoy correlation to QoQ GDP in the high 90s over the last decade).

These approaches are consistent with a far healthier economy in Q2. That seems consistent with the strong growth of employment and the decline of the unemployment rate. The main problem with these sorts of judgements is that employment lags GDP. In the case that GDP has genuinely changed direction, the labour market data tends to lag behind for one or two quarters.

The lagging labour market does seem to have been part of the story in Q2’21. A model that excludes employment data (the blue line) is consistent with GDP growth of ~1.0%qoq; this is ~70bps slower than one that includes employment data (the orange line). However the main point is that both are much larger than what we’re likely see in the Q2’21 National Accounts.

The main take-away is that the RBA is unlikely moved by a weak headline Q2’21 print. They will try look through the number and stick with their plan to taper to 4bn starting in September. The main argument for doing something is to get ahead of the retail-confidence reaction.

The most likely monetary policy response is still to pre-commit to buying at 4bn per week until at least February (50%); pushing back the taper to November (30%) is still more likely than no reaction at all (20%). There’s just not much difference between the former two.

One comment

Comments are closed.