A key reason i do not think the RBA will ease their policy rate at their May meeting is that the housing market is turning up. Just the day before the Q1 CPI report was released, Luci Ellis (Head of the RBA’s Financial Stability Department) was at Citi giving a speech entitled Housing and Mortgage markets.

This speech included a section on the monetary transmission mechanism (of which housing is a key part). Luci noted that it is common to hear scepticism about policy’s efficacy at this point in the cycle, but that they were seeing signs that they had traction.

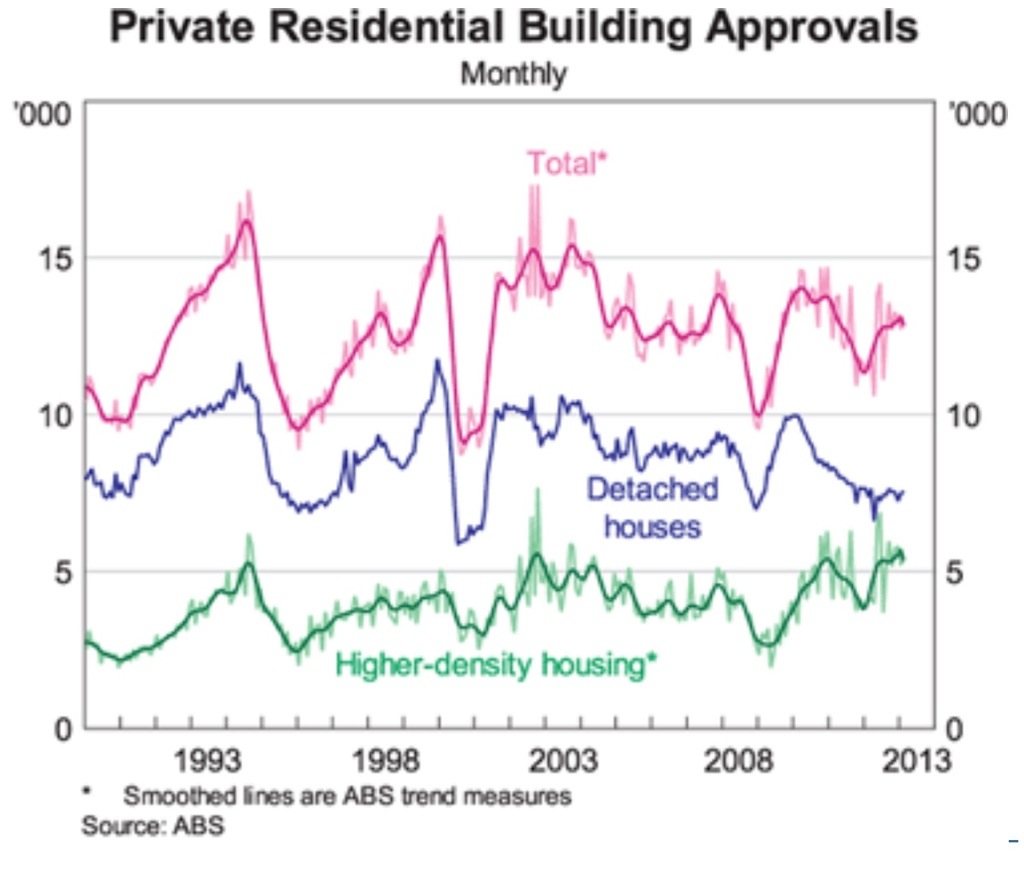

Interest rates have been lowered quite a bit over the past year and a half or so. As so often seems to happen, soon after a period of easing we start to hear concerns that monetary policy might not have any effect this time, because of some special factor interfering with normal relationships. After a period, though, the signs start to emerge. Typically, financial variables like credit and asset prices respond first. Output and inflation adjust later, the well-known ‘long and variable lags’. Recent data have followed precisely this pattern: monetary policy still works. Equity markets are up, and so are dwelling prices (Graph 10). Credit growth has remained quite slow, but loan approvals to investors and existing home owners have been picking up for a while.

My read on this is that the RBA judged that they had gained decent policy traction, and could expect their prior policy easing to further add to demand in the future. The change in house price dynamics (they were falling a year back, and are now rising) seems to be a key part of this judgement.

This is stage one of monetary easing – the easing of broad financial conditions. The RBA’s finger prints are on the house price part of this; the world’s major central banks (ECB, Fed and BoJ) own the equity market re-rating — i think the RBA would have already cut further if not for the equity market re-rating that began in mid 2012.

By the way, the change in domestic house prices over 2012 suggests that the RBA was still tight mid year when policy was 4.25%. Looking back, neutral seems to have been ~3.5%

So now on to stage two – real activity. Again, it is common to hear that this time it is only going to be asset prices – like future consumption can rise indefinitely without any impact on current consumption. I don’t buy that, and we are seeing some signs of a pickup in housing activity.

Is it enough? Will it be sustained?

That depends on how quickly we lose demand from the mining investment boom.

This is why i think the RBA will hold policy steady in May – they are awaiting more information about the likely evolution of mining investment demand. They don’t want the housing market to be too strong too early – as that might create other troubles (either inflation or financial stability) down the track.

That the RBA will not cut in May I 100% agree with. They will cut in June or Jule.

That housing is recovering a bit from the lows, after the recent cutting cycle I agree too.

But that housing will provide the economic traction that it used to, that monetary policy is having the same impact that it used to, that I do not agree with it at all.

The saving rate is much higher this time around, credit growth not even close to what it used to be and I see no signs of that changing soon.

Regarding the housing market, has Luci Ellis (who famously said that higher house prices in the US were not a concern pre-2008, higher house prices were actually desirable), saw any of these charts:

http://www.macrobusiness.com.au/2013/04/more-evidence-of-fhb-retreat/

and

http://www.smh.com.au/business/new-home-sales-hit-16year-low-in-february-20130403-2h640.html

Yes, prices may be higher in the last quarter, supported by higher share prices and investors activity, but that is a seasonal spring/summer bounce.

With local inflation still running a 4%, and having done so for a decade now, building has become a luxury. We probably need another 100 bps of cuts to make the AU fall.

Cash rates will keep going lower until the AUD moves structurally (for a year or so) below parity with the USD. When the AUD will do that, imported inflation will stabilize and the RBA won’t be able to cut anymore. If AUD stays above parity rates are going lower.

One more graph. Check out the owner occupied finance commitments ex refi.

http://www.macrobusiness.com.au/2013/04/housing-finance-beats-expectations/

Now adjust that for population and GDP growth.

Prices may be going up, with record low transaction volumes.

The transmission mechanism is obviously much weaker.

Sorry, last comment, I do not want to spam the blog! :)

Do we want to ignore the March PCI?

Click to access pci_march_13%2520report.pdf

If the RBA sticks to its forecast of growing unemployment and low inflation, I really do not see housing as being a constraints to lower rates, right now.

It is only one month of data – the trend for the housing component remains up.

Non-tradable deflation has still a long way to go:

http://www.adelaidenow.com.au/business/low-prices-and-stronger-dollar-but-still-aussies-pay-more-for-new-cars/story-e6frede3-1226630649830

Cars are just an example of imported products that have not adapted (yet) to the stronger AUD. It takes time, but there’s a lot more scope for imported prices to fall, if the AUD stays high. So if the AUD stays high, overall inflation will stay low and rates will go lower.

http://www.smh.com.au/digital-life/digital-life-news/evasive-microsoft-adobe-fail-to-justify-prices-20130322-2gjkr.html

Great post and I basically agree with the conclusions. The issue for me is not whether monetary policy can work, or whether it is currently expansionary, but whether it is expansionary enough. I think the balance of risks favours a more expansionary policy than has been implemented since mid-late 2011. All this hand-wringing that’s been in the papers (especially the Oz) about life after the mining boom and how the Budget is shot forever all derives from the consequences of the recent excessively tight policy. This, in turn, increases the risk of bad fiscal and micro polices being implemented. Combined with the slow employment growth we have seen, I think there is good reason to have looser policy.

Speaking of the Oz and Paul Kelly’s article yesterday, I thought it was interesting how he quoted Garnaut as suggesting we cannot do 2008-style stimulus again due to our external position (the CAD) not being ‘strong enough’. That’s the least important reason in my mind not to repeat that exercise. It sounds like Garnaut is reliving 1986. And that turned out fine so I’m not sure what all the angst is about.

It is certainly the top concern of S+P (for what that’s worth). My guess is that it is a political constraint — they do not want to get put on -ve outlook, especially so close to the election. It would cost them seats.

I missed Saul Eslake saying a similar thing a few says ago – that we could face a recession in a couple of years when the CSG projects finish up. Call me a market monetarist, but this type of comment reflects the poverty of Keynesianism. First, recessions are largely monetary phenomenon rather than caused by real factors. Second, anticipated recessions seldom become actual recessions, mainly because the first reason means the monetary authority can prevent them.

Sorry, I should have said the cause of recessions is largely a monetary phenomenon. Recessions are themselves obviously real phenomenon. Getting carried away with channeling Friedman.

I agree. I think the RBA’s key concern is a goldilocks housing market – a bit of inflation but not too much. They know that Australians love their mortgage debt, so rates too low too soon will just encourage house prices to go on a mini-boom. But there’s probably little else to keep households feeling confident and spending as the mining investment boom winds down.