The RBA today published their Q2 2013 SOMP. The bottom line is that every meeting is live, but i think they are more likely to await the Q2 CPI data before easing further. If there’s some bad demand side data, they could cut at any meeting, however if it’s just a case of (more) plodding growth, they’ll likely await the CPI reports and cut if inflation remains low.

The Q2 SOMP does not fully clear up the confusion i felt following Tuesday’s rate cut, but it helps. In part because it reveals a little of the RBA’s confusion.

To me, the SOMP feels a bit ‘between horses’ — my sense is that the RBA will cut if their forecasts prove correct. So why wait? I sense a degree of ‘wait and see’ about the new low inflation view that’s embodied in these forecasts.

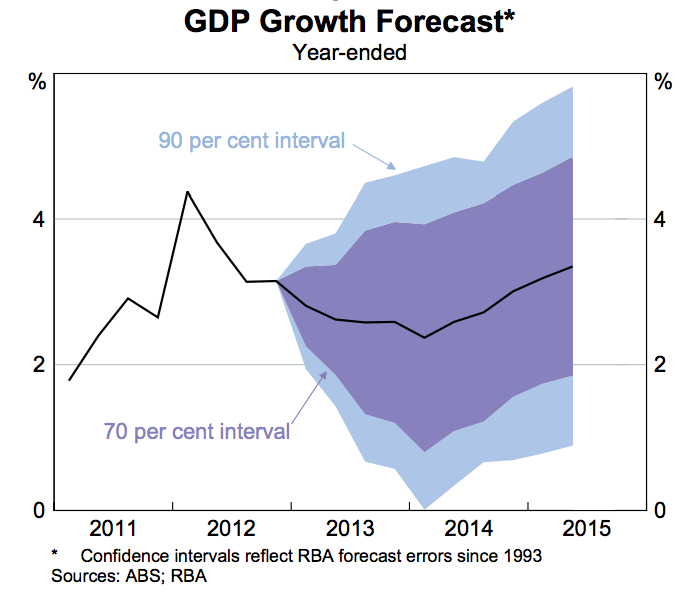

First of all, I think it’s great that the RBA has continued to publish their GDP and CPI fan charts. I think its healthy to be open about how hard this forecasting gig is, and the amount of judgement that is required to do a good job (and I think that they have done a very good job).

Anyhow, onto the SOMP.

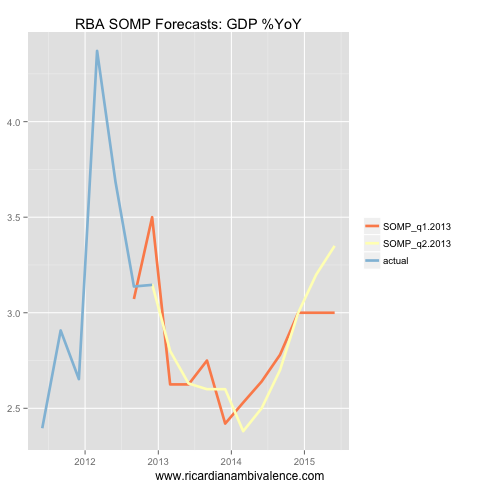

As I suspected prior to the May RBA meeting, the RBA’s demand forecasts have not been downgraded. Q4 was weaker than they expected (we already knew that) but Q1’13 appears to have been upgraded ever so slightly (+20bps to 2.8%).

Meanwhile, the growth low has been pushed back a quarter to Q1’14, and marked fractionally lower. The tail of the recovery looks better, but that may be due to how I made the charts. There was no fan-chart forecast for 2015 in the Q1’13 SOMP, so I used the middle of the range given in the table, and this may have depressed the Q1’13 SOMP’s 2015 estimates.

All told, there’s no upgrade (which I had thought possible prior to the May meeting) but neither is there a downgrade. My bottom line — they didn’t cut because of a demand downgrade.

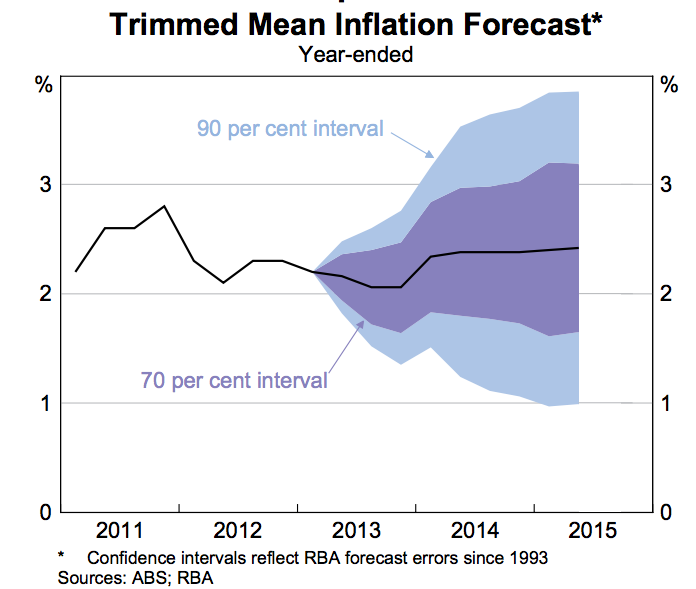

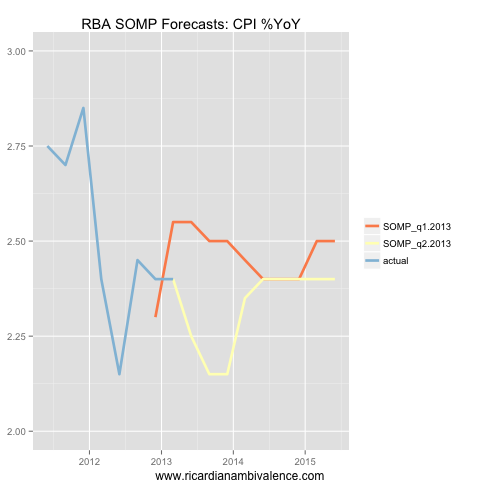

On the inflation side we can clearly see the reason for the rate cut — inflation is too low even assuming a 2.75% cash rate. It would have been a nit lower if they had not cut, as then they would have assumed a 3% rate. In these forecasts, core inflation never gets back to 2.5%y/y. That’s unacceptable for a central bank that targets 2.5%

Long term forecasts are not very reliable, so the RBA won’t put too much weight on this, however it is a good reason to cut again. More weight will be placed on the nearer term forecasts, which are even more concerning.

Core CPI inflation is forecast to fall to ~2.15%y/y later this year which is way too low (note: this chart shows average core CPI, unlike the above RBA core CPI fan-chart, which shows trimmed mean inflation; trimmed mean inflation is below average core, and touches ~2% in 2013 as trimmed mean CPI was ~20bps lower than weighted median CPI in Q1 2013).

All told, I feel a little more comfortable that something has happened to the RBA’s judgement of the supply side. They have published very similar growth numbers, and meaningfully lower inflation, despite a lower cash rate. This suggests that the RBA either thinks the output gap is wider, or that potential growth is higher – probably a bit of both.

So what does this mean for monetary policy? The bits of the forecasts that are reliable are the short term forecasts, and these show that inflation will be around the bottom of the band and that growth will be well below average for the next six quarters.

With this combination of forecasts, I expect that the RBA will cut at least twice more this year.

Why not right away? I think that’s because forecasting is hard, and judgements about potential supply are even harder; so they would like to wait and confirm their theory.

If demand (GDP) and inflation (CPI) come in around RBA forecasts, I expect the RBA will cut following each of the CPI reports this year, taking the cash rate to 2.25% by the November meeting.

If demand is around forecast and CPI is higher than expected, it’ll show that supply hasn’t moved out, and the RBA will hold. If demand looks like it’s flagging, expect earlier cuts. What about hikes? Not likely until we have navigated the end of the mining boom …

_____

Finally: It would be great if the RBA published all the data in their charts in a machine readable format (as the RBNZ does). If you have time and interest you can get the data from the charts with freely available tools (I used this one). There’s no public interest in hundreds of people each wasting an hour doing this, so I hope they consider this further step toward open policy making.

2.25% cash rate, who would have thought!

That would send the ASX 200 another 10% up and AUD down further.

What if house prices too keep going like they have since May 2012 but inflation numbers or GDP do not reflect that in 2013, do they care?

House price rises since may 2012 have been modest. If that is all they get they could cut even further.

confused. before last meeting you wrote that housing was one the reasons why the rba would not cut. that concern now completely gone from their minds ? there must be a level of price growth that would concern them. maybe 7% y/y or more? NZ is experiencing this with their low rates and LVR limits will be put in place.

I had thought they would not cut because the upturn in housing meant that their demand forecasts were probably OK. the new information is that the demand they forecast is not enough to make inflation hit 2.5%, even though their demand forecasts are little changed.

I never meant to give the impression that house price appreciation was a threat to financial stability — which is what the rbnz is saying.

got it. i still think housing maybe a precursor of future medium-term inflation, which they recognize they can’t forecast properly anyway. i see the RBA in pure reaction mode to data, i think a significant turn in housing would make them rivise their inflation forecast higher especially if combined with a lower dollar. In that case they’ll stop cutting. I mean if we really get down that low with unemployment stable at these levels, it would be quite risky for inflation especially non tradable.

What’s your latest view on AUD in light of these latest RBA developments?

cheers

Well soros and co have made more money than me trading fx, but i still see it as a buy. I was a bit too early, it seems. Might have to revise that if the fed really tapers.

According to a note I read from Macquarie, the SMP made a point of saying that house prices rising too fast could be a threat to financial stability if it were accompanied by increasing household leverage. Being Sumnerian, I think the real risk is from house prices falling too much due to falling NGDP growth. And any silly house price increases would probably be associated with NGDP rising too fast (a la 2007), which should also be avoided for its own sake. Using monetary policy to target asset prices directly would be a big mistake.

Sumner has an odd view here — in that he is a level target fan, so bygones are never bygones, but asset markets are (weakly?) efficient so financial market prices are always basically right?

I think housing is a momentum market, so it can overshoot actual income growth and create trouble when / if the income growth required to make the purchase come good is not achieved.

Anyhow, the current state of the australian housing market seems to be ‘modestly inflating’. Perhaps this is a reason to cut only slowly – that momentum character means a quick burst of 100bps would probably make housing re-rate to a greater extent than a year of 25bps per qtr – but it is not a reason to accept sub target cpi for the entire forecast.

I don’t think there is anything inconsistent in advocating level targeting but believing in the EMH. Sumner has said something like he doesn’t believe in bubbles, but if they exist, it is because markets are naively assuming perfect stability in NGDP growth. Invariably, something happens to disturb that complacency and the market falls. So there are no bubbles, only valleys, or something like that.

I agree with your second para, and see that as a reason both for stable NGDP growth and for level targeting. The 2005-7 period was a worry because NGDP growth got to 8-9%, which was not sustainable on any measure. But I would see any house price ‘overshoot’ resulting from moving back from 3% NGDP growth to 5-6% or so as being fairly benign, even if that ends up being a 15-20% appreciation over the next year or so.

The RBA (and other central banks) may not see an inflation problem until it actually happens all of the sudden and it gets out of hand, I think that is the risk. The whole world is easing money supply, they may be already creating the next bubble without even knowing it. Prudence and stability (in both directions) is the name of the game, IMO, I think it would be worth sacrificing a bit of GDP growth and inflation right now in the name of future stability. Look at what govt will be doing this week: budget will not be balanced for the foreseeable future “to protect today’s jobs”, who cares about the fact future generations will have to pay for it and that today’s entitlements are not sustainable.

Publish the data to quandl