The RBA just released their semi-annual Financial Stability Review (FSR). Predictability, the FSR plays down the risks from the maturity of Interest Only (IO) loans — however I think they are over-confident.

Let me explain.

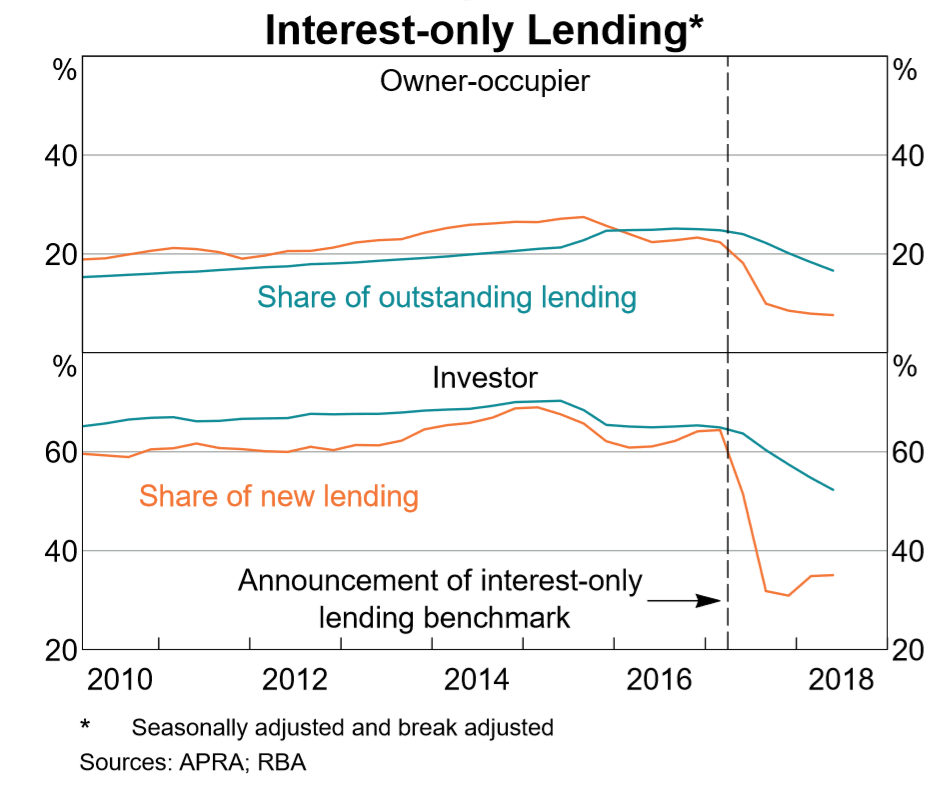

In the five years prior to the introduction of policy measures to slow IO lending, IO loans rose to be ~40% of the flow of new loans — and therefore ~40% of the stock.

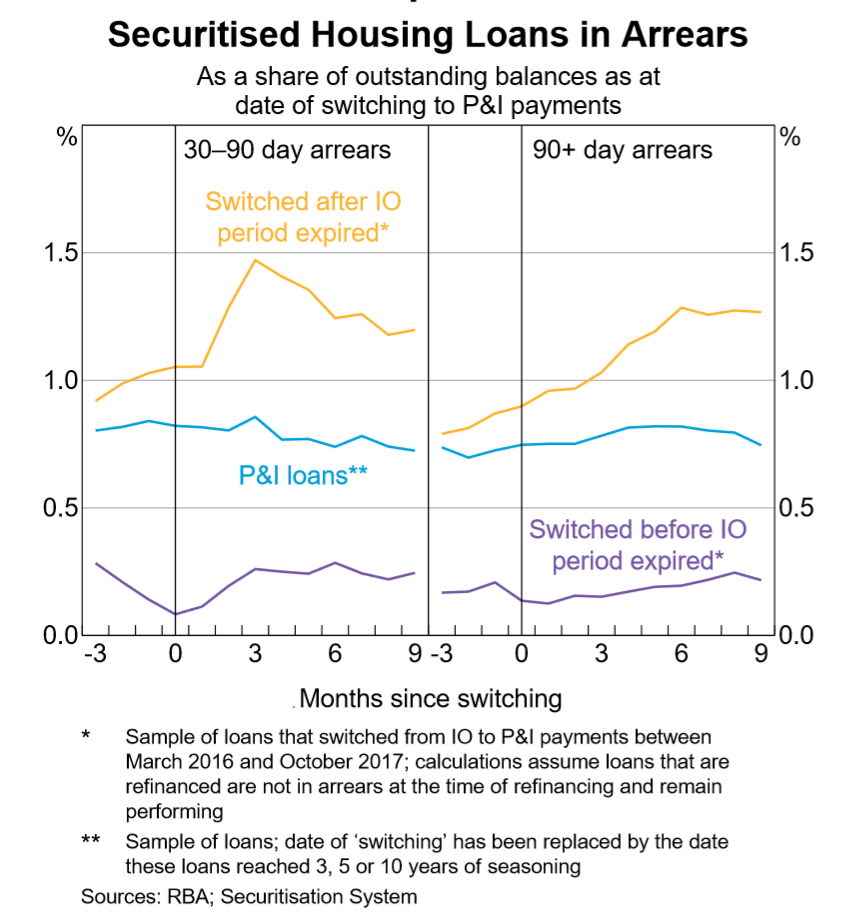

While the largest part of these loans were made to people who could afford a traditional mortgage — and elected to make IO repayments for other reasons — my hunch is that a meaningful proportion of these loans were made to people who could not afford to repay the principal. You can get a sense for this from the spike in arrears that we see when an IO period expires.

The thing to note about the above chart is that the observation period used to calculate mortgage performance is Mar’16 to Oct’17 — before the tightening of credit conditions that happened in 2018. IO borrowers tend to experience stress when their IO period ends — which suggests that some proportion of IO borrowers are unable to afford a P&I repayment schedule.

The two main exits from this situation are refinancing back into a new IO loan, and selling the house. My guess is that the exit is much tighter now: you have to pass one of the new, tighter, credit checks; or sell your house in a bear market.

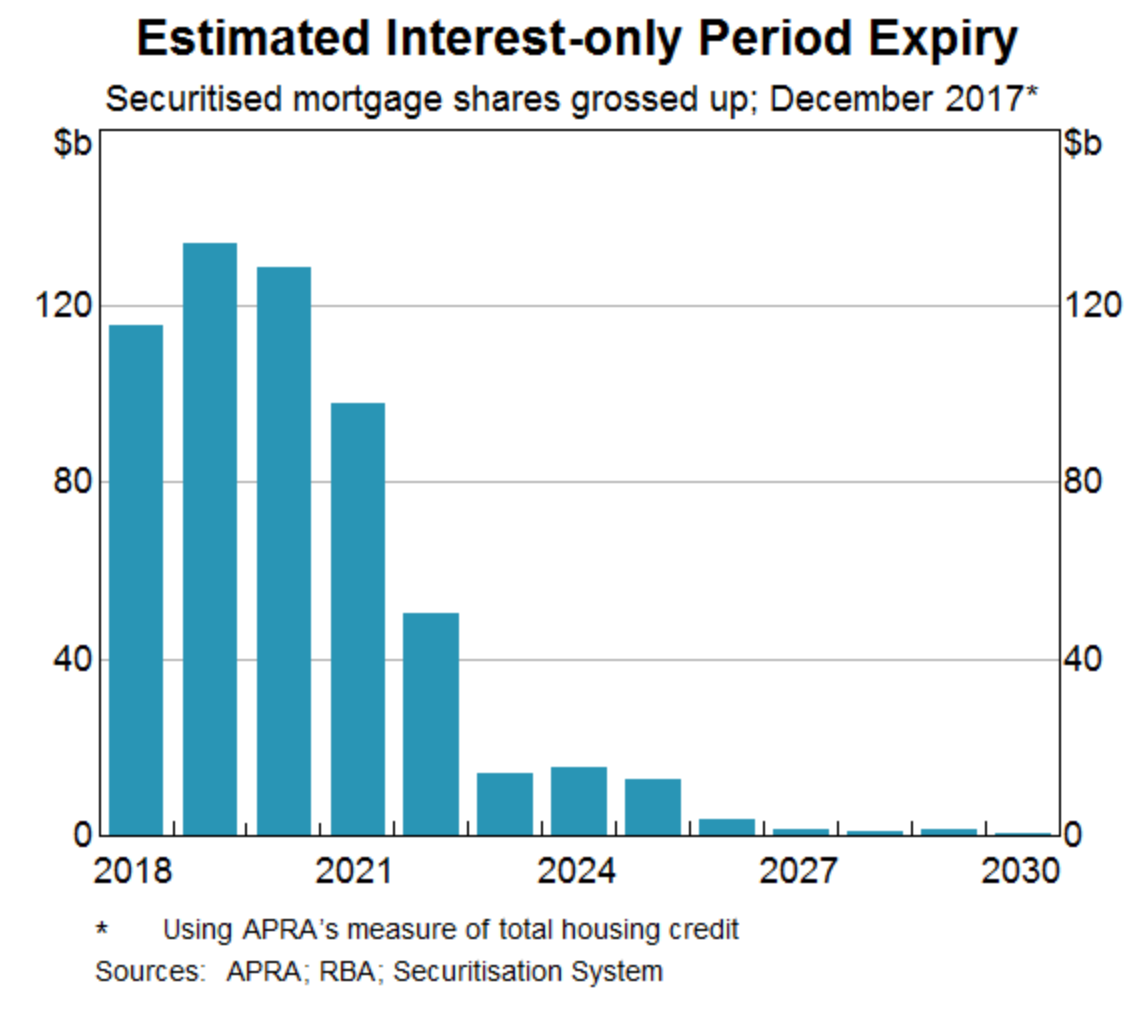

Over the five years 2018-2022 ~600bn of these mortgages mature. Given the timing of the IO mortgage boom, and the fact that most IO periods are 5yrs, I would think that most of these buyers got into expensive Sydney and Melbourne properties in the 2013-2018 boom.

Those who got in early have plenty of equity, so the house may be sold to repay the loan — but given falling house prices the 2016/17 vintages (maturing in 2021/22) won’t have that padding. If the house is sold to repay the loan, there may be a gap.

The RBA says ‘no problem’, most people can afford higher repayments, and most are ahead. That’s true, but beside the point. These events are about the minority of people who can’t afford to repay. So rather than focus on the right hand side of this chart (the 50% who are ahead), I think we should focus on the left-hand-side.

Over 30% of households have no mortgage buffer at all, and over 50% have less than six month’s buffer.

Unfortunately I don’t have the detailed data required to link how far ahead households are to the loan type — but a bit of common sense tell you that new mortgages are much less likely to have a buffer.

So the main challenge facing the Australian housing market (and economy) is the 600bn of relatively young interest only mortgages that mature over the next few years. These borrowers are more likely to struggle with the 40% increase repayments, are unlikely to have meaningful buffers, and (given the tightening in credit standards) may find it difficult to refinance into a new loan.

Their only option will be to sell into an already depressed housing market.

Let’s say 10% of these loans unfold in this way — that’s equivalent to ~1yr of supply for the housing market (as ~4% of houses turn over each year). An increase in the supply of housing of that size is likely to weigh on prices in any case — and particularly so given that the new rules reduce average borrowing power.

well done.

Let us add a few things.

If people have problems when interest rates are sol ow what occurs if they rise although that maybe problematic given that wages are going nowhere.

What if a number are not investors but speculators and have assumed rising prices.

The second case is a big problem. Speculation that assumes capital gains will not survive the 40% repayment spike and falling prices

I am betting the RBA are sweating over it.

Thanks for the post, very interesting. I don’t know the data or the housing market well enough to come up with any unique points of disagreement, but here is my attempt at coming being devil’s advocate drawing on this Kent speech: https://www.rba.gov.au/speeches/2018/sp-ag-2018-04-24.html

1. The remaining stock of IO loans now appears to be closer to $500bn, due to people voluntarily shifting to P&I. Of course, this means (as he recognised) that the remaining stock of borrowers could be more cash-flow constrained than they were on average before.

2. It’s hard to estimate the affordability of shifts to P&I or infer it from prepaying data because at least investors have an incentive to not reduce their loan balances, as Kent notes.

3. As Kent says, refinancing (perhaps into longer-term P&I loans to minimise cashflow impacts) or reduced expenditure are options, and with reasonable ongoing jobs and income growth, one would think mortgagees would do all they can to avoid selling into a bear market.

4. But your point is that even if 10% can’t afford it, the effect on the property market could be large. Maybe, but is it correct that only about 4% of houses turnover each year? That suggests a typical period of ownership of 25 years. I thought it might be more like 10 years, and likely shorter for the types of properties likely to be the subject of these loans (Sydney and Melbourne apartments). So will it be a big increase to the volume of sales? Having said that, one would expect that voluntary sales would fall a lot in the bear market, so perhaps the increase over the ‘natural’ volume would be more significant than in a bull market.

5. Finally, as I suggested, we’re likely talking mainly about flats. It’s possible that as apartment construction slows down, rental growth could pick up (again, assuming decent ongoing income growth) and help to cushion the rise in repayments – see here: http://petewargent.blogspot.com/2018/02/a-coming-rental-crisis.html

Anyway, thanks again and whatever happens, it still certainly a worrying time for property-owners.