I must admit to being a bit stunned by the RBA’s May SOMP. There were a number of elements that strained credibility — but in particular i felt that the labour market sections were a stretch. But, as ever, the game is to predict what they will do, so here we are …

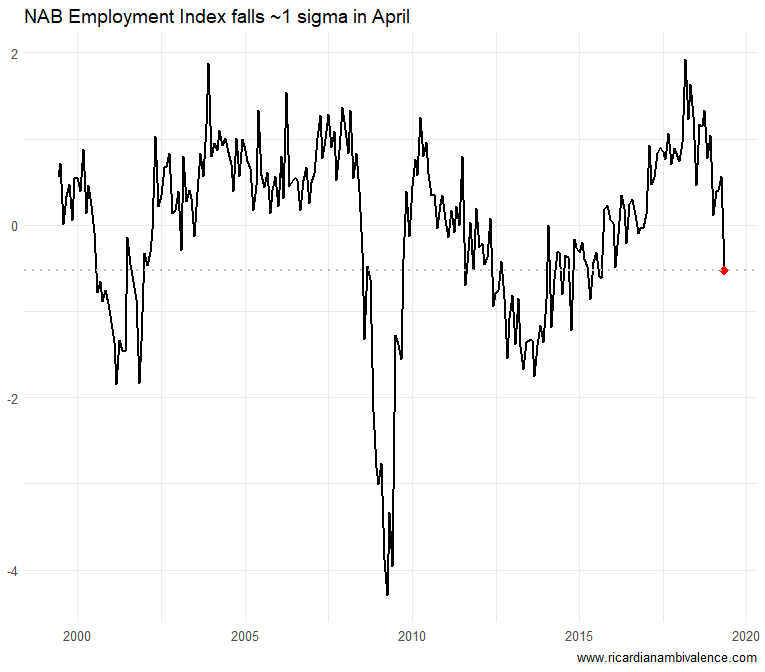

Their bull case appeared to fall apart today, with the NAB Employment index falling sharply to a below average level (-1 sigma to -0.5 sigma).

In the SOMP the RBA wrote that “business employment intentions remain above average according to the NAB quarterly survey and the Bank’s liaison program”. That evaporated today. , with the April NAB business surveys falling 7.4pts to -1.2.

This means that there is no longer an interesting divergence between job advertisements and the NAB survey. The RBA leaned on this divergence heavily in the SOMP, when they noted that “there continues to be some divergence in these indicators; the decline in job advertisements points to a much weaker outcome for employment in the near term than the leading indicators from business surveys”.

Presumably this also means that they will also strike out the upside risk that the labour market is stronger than they anticipated.

So regardless of the outcome of the April employment report on Thursday, we just got some important, and certainly challenging, information about the labour market.

I think we can only say Lowe is no Glen Stevens and the only reason they di not cut is the election.

On a related topic just how low can they go until the banks lose money on taking deposits?

In the SOMP the rba has a chart showing the distribution of deposit rates. Most are around or above 1%, so the NIM reduction should be mild down to a 50bps cash rate.