The April employment report revealed a slackening of the labour market — and is probably enough to get a 25bps rate cut in June.

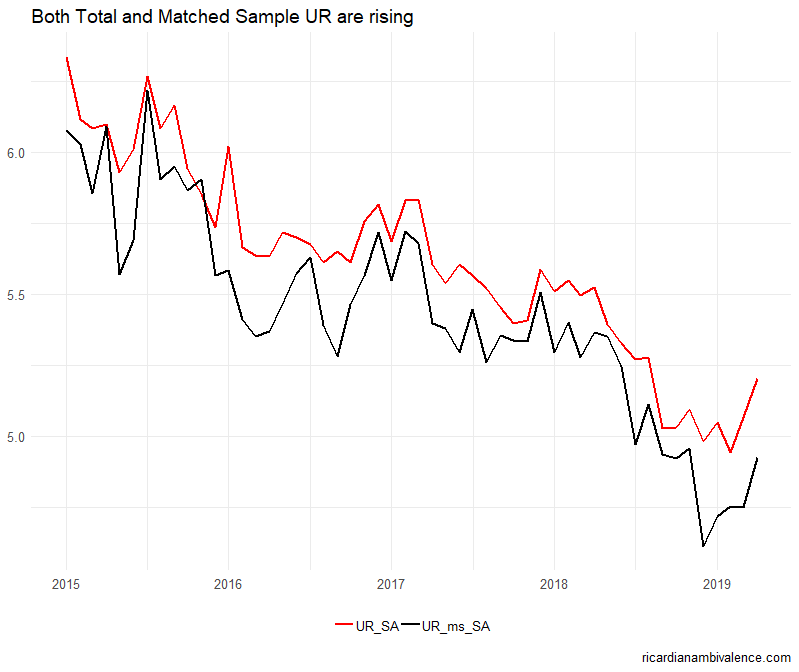

The headline unemployment rate rose ~14bps to 5.20%, with March revised up ~2bps to 5.065%. Don’t get distracted by the strong growth of headline employment (+28.4k) — the household survey is designed to measure the rate of unemployment, and that’s what it does best.

It’s tempting to blame sample rotation — as the incoming sample’s unemployment rate was 160bps higher than the sample it replaced — but i don’t think that’s right. The increase in the unemployment rate is actually larger if we exclude that new rotation group: the matched sample unemployment rate rose 18bps to 4.93%, which is a larger move than the 14bps increase in the total unemployment rate.

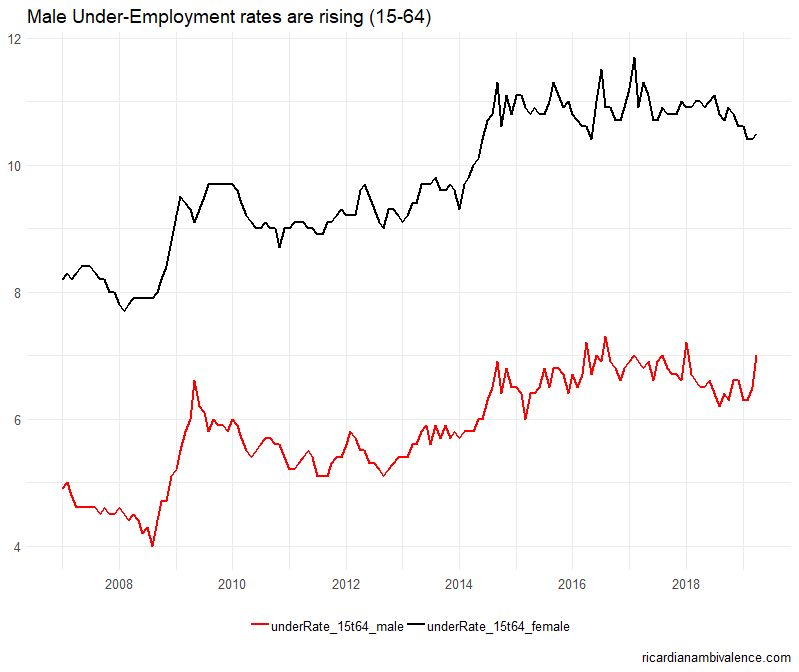

The underemployment rate data confirms the softening. This measure increased 30bps to 8.5% on the month (prime age was +30bps to 8.7%).

The details are consistent with what you’d expect in a cyclical downturn. Men tend to work in more cyclical industries, so in downturns you tend to see the male underemployment rates rise faster than female underemployment rates. That’s exactly what we are seeing: in April the prime male underemployment rate (15 to 64) rose 50bps to 7% and the female +10bps to 10.5%. The spread between the two has tightened ~100bps in the past six months (from ~450bps to ~350bps).

Combined with the weakness in the employment component of the April NAB business survey and the disappointing sideways profile of WPI, any fair minded person would conclude that the probability of inflation meeting the profile set out in the May SOMP last week has declined somewhat. The leading indicators are softer, and the transmission of labour market pressure to wage growth is less certain — so the downside risks to the inflation forecast are rising.

The inflation forecast was already too weak (and it was made assuming a rate cut in August and another in Feb’20), so I would expect the board to bring forward the rate cut to either June or July. Most likely June.

and the labour market is a lagging indicator

I’ll take the opposing position again for the following reasons.

If they move in June it:

– Immediately confirms they made a mistake in May

– Potentially confirms the (likely false) narrative that they politicised their May decision

– Opens them up to huge market criticism of the May error.

They’ll sight it as a single data point driven primarily by an increased participation rate and will want to see some more data points to confirm an adverse move in the UE rate.

Even money chance “carefully monitor” is used, which further confirms to market that if UE rate above 5 is maintained in June and July that they’ll pull the trigger in August.

August is a lock (assuming data maintains trend) as it gives them enough time to continue the place setting and narrative building that external influences (trade war escalation etc) are the causes of the move, rather then their own gross mismanagement, and it distances themselves from the May error so they can frame this as them prudently coming to the rescue. August gives them the ability to frame the narrative that the data has “turned” for long enough that *now* action is warranted and that they are acting accordingly.

Again, zero disagreement with your objective, data-based analysis. But I still think human instincts continue to over-ride objective policy action.

I hope you are wrong. Lowe has been a total dud as gov.

100%

all confirmed.