[note this is the third in a series looking at the indicators for Q1’13 Australian CPI: we have also looked at the business surveys, and NZ CPI]

Forecasting CPI is a tough gig … however, due to the fact that Australian CPI comes out very late, it’s possible to get some edge from the data that’s already been released for other areas.

The RBA published a sophisticated RDP looking at this last year. I find that the majority of the benefit (in terms of forecasting Australian trimmed mean CPI) comes from using the US trimmed mean CPI number.

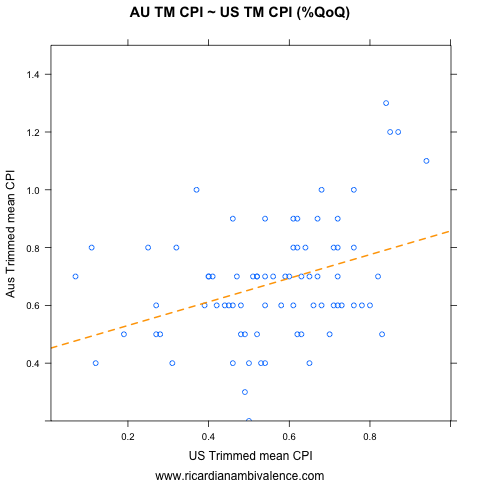

On a quarterly basis, there is an okay relationship between US and Australian Trimmed Mean CPI. We get the US data early, and you can do an okay job with just two months of data, so that allows us to make a fairly informed guess once we know Feb US trimmed mean CPI.

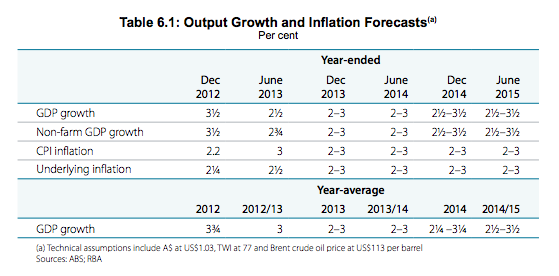

Using US trimmed mean CPI, and lagged values of Australian trimmed mean CPI, a forecast of ~0.6%qoq for Q1’13 drops out. This is exactly what the RBA’s Q1 SOMP implies (their forecasts are half year ended YoY rates, so the precise read is that the RBA expects CPI to average ~0.6%q/q for the next two quarters).

The QoQ model is likely to be biased up. Recent QoQ CPI results have been inflated by the carbon tax and other policy changes — so the model thinks there is more inflation momentum than is actually the case.

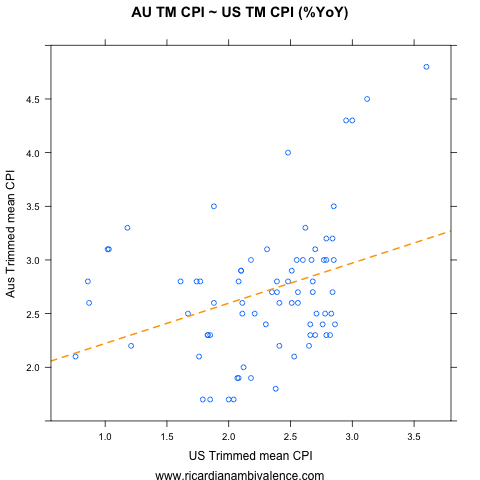

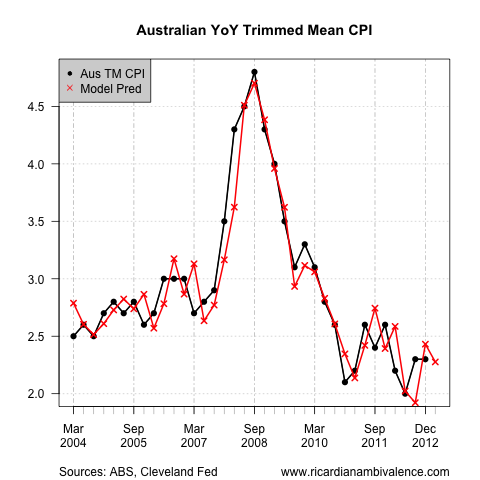

The relationship looks better with between the YoY trimmed mean CPIs (this is the case, as shocks arrive and are passed on in an uneven fashion, and YoY allows these to average out over time).

Using lags of Australian trimmed mean CPI, and the current quarter and lags of US CPI, we can do a pretty good job of forecasting Australian CPI. This model’s forecast is 2.3%y/y (which requires a 0.4%q/q result for Q1).

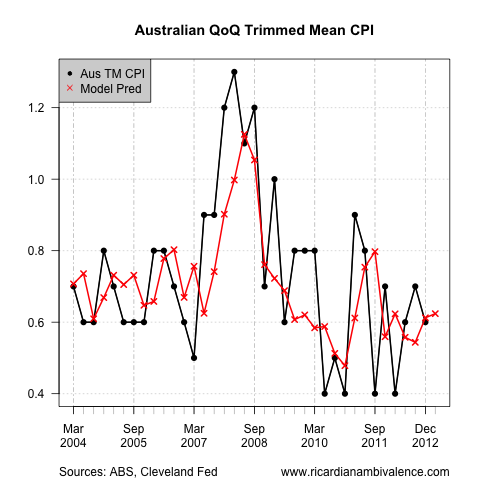

Taking the average of the two models — always a sensible thing — suggests that something like 0.5%q/q is likely for Australian trimmed mean CPI today. That’s low, and eyeballing the above chart, is very likely a little lower than the RBA expected in their Q1 SOMP — but i do not think it is low enough to get the RBA to cut their policy rate (the test is does demand need support?).

After all, Q2 CPI could well be a little higher, and that would push them back onto their 2.5%y/y core CPI projection for H1’13.

Interesting that US CPI is such a good predicter. For mon pol purposes, our CPI should be adjusted down by 1.4% this fin year, half for the carbon tax and half for network price increases, both of which have nothing to do with aggregate demand.

Agree. The difference between cost of living and inflation is not understood by a few – all these little price hikes are just like taxes.

I expect a low number too, on the lower end of the RBA target range.

On the demand side, non-tradable inflation is going to be interesting: if demand is weak it should be falling and the gap with tradable closing.

According to my quick calculations, non-tradable inflation is still running very hot at 1.3% q/q in original terms, while tradable is in full deflation now at -1.2% in original terms. the two combines give a benign overall number. So more of the same… still staring at the same issue with the high dollar making imports cheaper and local products uncompetitive. Obviously, money that is freed up because imports are cheaper get spent to locally for the time being and some pricing power is still there.The truth is that local inflation is still not contained at all. Should the dollar fall, overall inflation will pick up very fast. So I do not know if dropping rates further is the solution here really.

Yep, and about 1%qq SA (my SA) for non-tradable … They have cut when it is this high before, but then asset prices were not working so hard for them.

at the better end of it.

Well done

Hmm, i don’t feel so good. I think i needed to weight the survey data more. Back to the drawing board.

Clearly the inflation genie is out of the bottle thanks to 125 bp of excessive easing last year due to an industry-captured RBA Board…

Subtracting carbon and we are at <2%. Now let's see if the RBA is more interested in targeting inflation or asset prices.

Non-tradable inflation is still running very hot at 1.3% q/q in original terms, no signs of more rate cuts needed there. It’s imported deflation that keeps the overall number so low. We have a two-speed inflation too, RBA should pay attention to this.

Q1 is seasonally high – things like health and education costs go up. All groups SA is at 0.1% q/q.

Non-tradable y/y is at 4%+ , the highest since post GFC.

Has been like that, around 4%, for a looooooong time.

And that’s why building new residential is super expensive and sales are at record low.

Haha, yep all those inflation hawks need a lot of inflation and very soon to be right about the RBA having made a mistake last year.

SSEC that is like saying if my aunty had balls she would be my uncle!

It has been thus for a long long time.

Six month annualised underlying rate which the RBA likes to look at is at 2%.

There’s a cut coming folks.

“It has been thus for a long long time.”

Yep, that’s why businesses look at local costs and say see you later.

Yep, there sure is scope. But in May? Is demand really that weak?

Inflation low, UnN rising, if the cash rate wasn’t already at 3%, they would cut. Hence, they should cut. My concern is that they pay too much heed to absolute levels of interest rates (which are misleading as an indicator of monetary policy stance) and modest rises in dwelling prices.

the CPI is confirming the reasonable real GDP figures but weak nominal GDP figures.

SSEC ever since financial deregulation, the cutting of tariffs and actual competition policy working tradable inflation has always been appreciably lower the non-tradable inflation.

Sure has, but if fx is the problem we need to change that to rebalance — or we need a lower fx rate.

Looking at the non-tradable inflation (and even considering the carbon tax effect) and also asset prices in Q1, I do not think demand is that weak right now. I am starting to believe the unemployment rate won’t go much higher than 5.6%. I expected a weaker non-tradable inflation. Next labour data is on 09/05/2013, the RBA will meet before that. I do not think RBA will cut in May before having the unemployment data. They will maintain easy bias and probably produce more dovish minutes. The AUD keeps stubbornly high, even after CPI data.

WPI is okay.Remember non-tradables is exacerbated by ETS and electricity prices both of which are getting weaker now.

how do you get the $A down?

When we had a real demand crisis in Australia (i.e. after the share market crash of 2008-09) non-tradable dropped down to just above 2% y/y ; that was a real sign demand was very weak. Not so today obviously.

Another 50 bps of cuts won’t do much for $A, I am afraid: more cuts are already priced in by markets. It does not look like $A is in our hands. Today $A is keeping high despite CPI because copper, gold and silver rebounded. RBA can’t cut rates just to target $A IMO.

Interesting that the Kouk has folded on his ‘bottom of the cycle’ call of a couple of months ago. I suspect the entrenched hopelessness of Labor’s position in the polls has liberated his conscience to tell it how it is.

Lol … Next up, will Mr Joye call for a cut?

That would have to hurt. Maybe time for another Downfall parody..??

I watch it again and couldn’t stop laughing! It’s very well done!

Good analysis by CBA. They are always bullish, so they balance the general view of this blog :)

Click to access 240413-CPI.pdf